Key Takeaways

- Airbnb stock trades at near 29x NTM earnings versus Booking Holdings stock at ~16x, but TIKR’s model assigns ABNB a 16% IRR against BKNG’s 15%, reframing the premium as earned rather than excessive.

- Consensus expects Airbnb stock revenue to grow 12% in 2026, 3 points faster than Booking Holdings stock at 9%, with ABNB’s Q1 2026 beat of 18% growth suggesting further upside to estimates.

- TIKR’s mid-case targets $313 for Airbnb stock (+121% total return) and $342 for Booking Holdings stock (+102%), with the IRR gap widening to 16% versus 15% on a long-horizon basis.

KEY STATS

Airbnb (ABNB)

- Market Cap: $84.2B

- Enterprise Value: $75.5B

- 52-Week Range: $111 – $147

- LTM Revenue: $12.24B

- LTM Operating Margin: 21%

- LTM FCF Margin: 36%

- NTM P/E: 28x

- NTM FCF Multiple: 16.6x

- Net Debt / EBITDA: (3.3x) net cash

- TIKR Mid Target: $313 (+121%)

Booking Holdings (BKNG)

- Market Cap: $131.4B

- Enterprise Value: $134.3B

- 52-Week Range: $151– $234

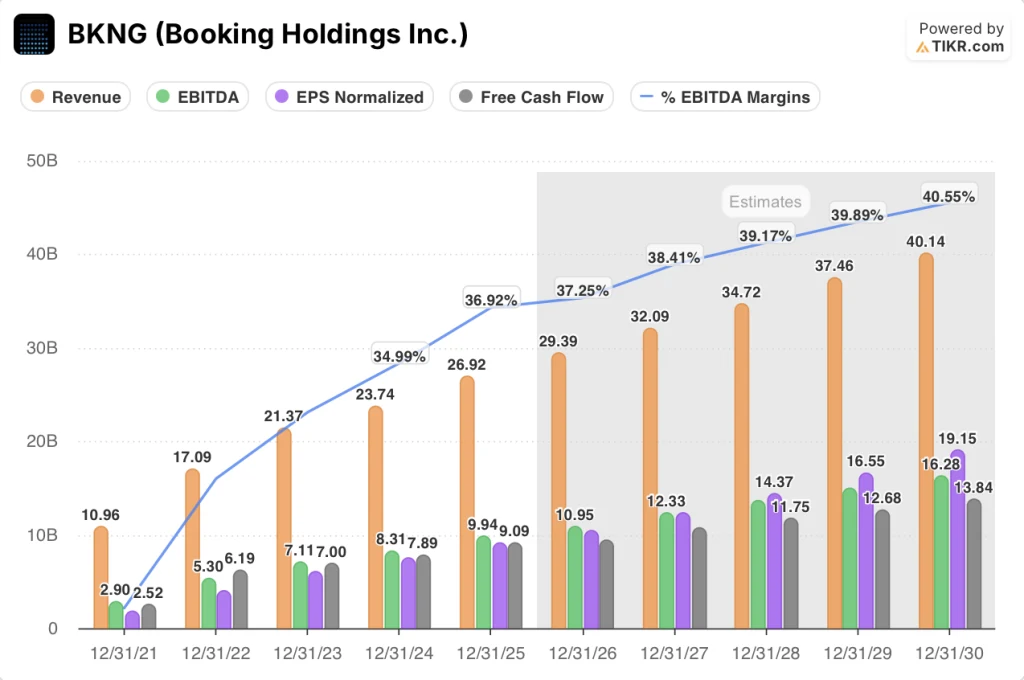

- LTM Revenue: $27.69B

- LTM Operating Margin: 35.3%

- LTM FCF Margin: 33.8%

- NTM P/E: 16x

- NTM FCF Multiple: 12.4x

- Net Debt / EBITDA: 0.27x

- TIKR Mid Target: $342 (+102%)

Two Models, One Question: Which Travel Platform Earns the Premium?

Airbnb (ABNB) and Booking Holdings (BKNG) represent two distinct bets on the future of travel.

Airbnb is a marketplace, not an intermediary. It earns a take rate on gross booking value flowing between guests and hosts, keeping its cost structure lean and its FCF conversion unusually high.

Booking Holdings is a portfolio. Booking.com, Priceline, Agoda, KAYAK, and OpenTable serve different segments across accommodation, flights, car rentals, and dining, with scale as the defining asset.

The tension is not between a good business and a bad one. It is between a mature compounder trading cheaply and a faster-growing disruptor trading at a premium.

Airbnb’s Q1 2026 earnings confirmed the growth story is intact. Revenue grew 18% year-over-year to $2.7B, beating the high end of guidance by 2 points, with Nights and Seats Booked growing 9% despite an estimated 100 basis point Middle East headwind.

App-based bookings grew 22% and now represent 63% of total nights, up from 58% a year ago. First-time booker growth hit its highest rate since 2022, with Brazil, Japan, and India leading acceleration.

Reserve Now, Pay Later is emerging as a structural monetization lever. Roughly 20% of global GBV in Q1 came from RNPL bookings, driving longer lead times and a mix shift toward higher-priced homes.

Management raised its full-year take rate outlook and guided revenue growth to accelerate to low-to-mid teens for 2026. Combined with a simplified fee structure for API hosts, the monetization narrative is gaining concrete traction.

Booking Holdings delivered its own solid quarter, though the Middle East conflict cast a shadow. Q1 revenue grew 16% to $5.5B and adjusted EBITDA grew 19%, but management guided Q2 room night growth at just 2% to 4%, absorbing an estimated 3-point headwind from the conflict.

The full-year outlook calls for gross bookings up high single to low double digits, with EBITDA margins expanding 0 to 25 basis points. The U.S. market is becoming a meaningful growth driver, with room night growth accelerating for the fourth consecutive quarter to low-teens in Q1.

Wall Street’s Take: Growth at a Discount or Discount for a Reason?

Market expects Airbnb stock to grow revenue 12% in 2026 to $13.71B, accelerating from 10.3% in 2025. EBITDA is seen expanding to $4.82B at a 35.2% margin, with EPS normalized growing 23.3% to $4.97.

FCF is estimated at $5.08B for 2026, representing a 37% margin, the highest in the company’s history on a forward basis.

For Booking Holdings stock, consensus models 9.2% revenue growth to $29.40B in 2026, with EBITDA of $10.98B at a 37.3% margin. EPS normalized is also seen growing 14.5% to $10.44, with FCF of $9.4B at a 32% margin.

The mispricing debate centers on multiples.

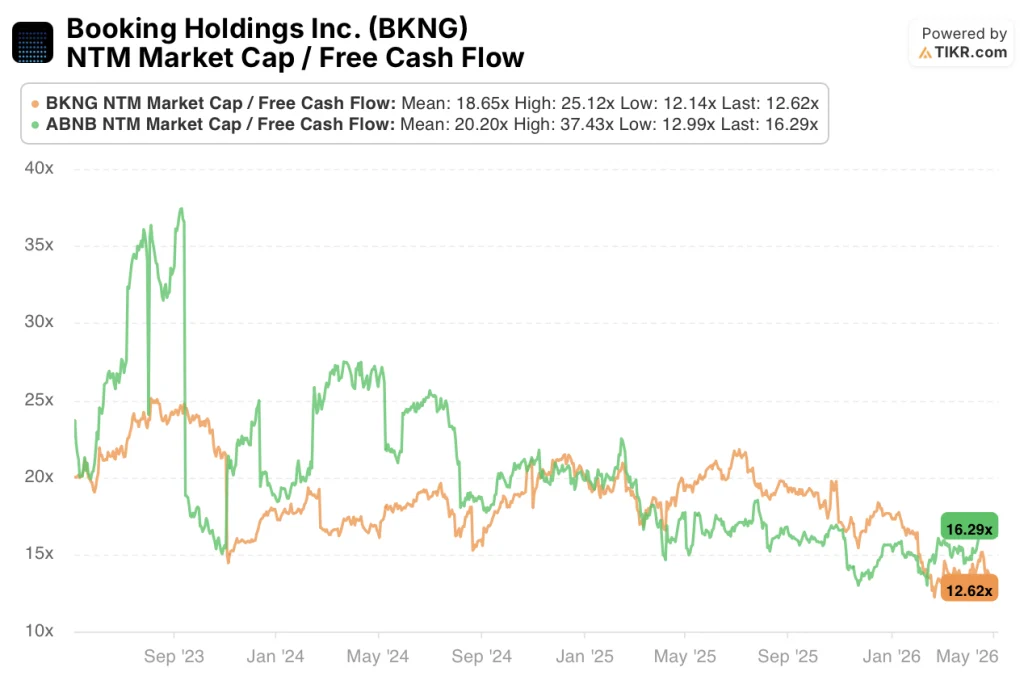

BKNG’s NTM P/E of 16x sits near the low end of its 5-year range, which has averaged closer to 20x.

Meanwhile, ABNB’s 28.3x NTM P/E is elevated in absolute terms, but the 5-year mean has hovered around 30x, suggesting the stock is not stretched relative to its own history.

On FCF multiples, BKNG trades at 12.6x NTM FCF versus ABNB at 16.3x. Both sit well below their 3-year means of 18.7x and 20.2x respectively, with BKNG’s discount to its own historical average the more striking of the two for a business generating nearly $10B in annual free cash flow.

The key risk for Airbnb stock is execution on new verticals. Hotels, experiences, and services are scaling, but each carries integration risk before reaching profitability at scale.

The key risk for Booking Holdings stock is geopolitical concentration. With approximately 7% of 2025 global room nights tied to Middle East travel, sustained conflict represents a structural rather than temporary drag on near-term results.

Financials: The Profitability Race

The margin comparison between these two companies looks like a paradox on the surface.

Booking Holdings grew operating margins from 24% in 2021 to 35.2% in 2025, a 1,120 basis point expansion over four years. Airbnb’s operating margin over the same period moved from 9% to 20.8%, nearly doubling but still trailing Booking’s by more than 14 points.

Yet Airbnb’s FCF margin tells a different story. At 37.2% in 2025, ABNB’s FCF conversion exceeds Booking Holdings’ 33.8% LTM FCF margin, reflecting Airbnb’s near-zero capital expenditure model where hosts bear the property costs.

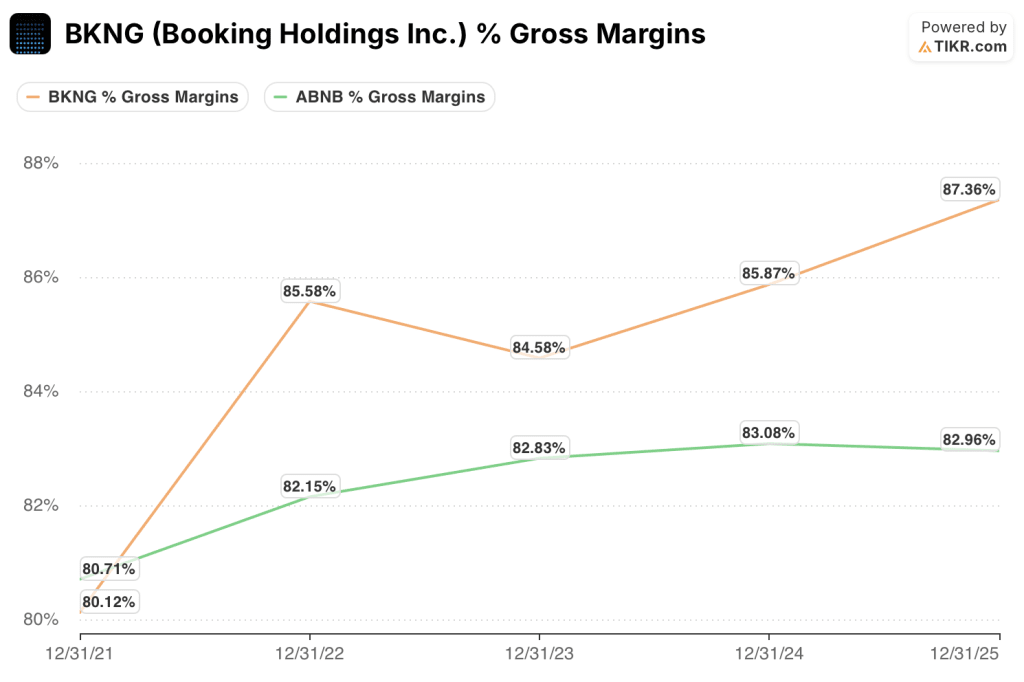

Gross margins are effectively tied. Airbnb runs at 83% gross margin versus Booking at 87%, both reflecting asset-light platforms collecting take rates on transaction volume.

The gap in operating margins is driven by Airbnb’s higher R&D spend as a percentage of revenue, at $2.35B in 2025, nearly 20% of revenue, as the company invests in AI, new verticals, and international expansion.

Consensus expects the margin gap to persist and widen. ABNB EBITDA margins are forecast to expand from 35.1% in 2025 to 35.9% by 2027, while Booking moves from 36.9% to 38.4% over the same period, a gap that widens from roughly 180 basis points today to approximately 250 basis points by 2027. If Airbnb sustains 3 points faster revenue growth at near-equivalent margins, however, the growth-adjusted case for the premium multiple holds.

What Does TIKR’s Valuation Model Say?

Both stocks are trading below their historical multiples, and TIKR’s model finds compelling return potential in each. The question is not whether either business is worth owning, but which one the data favors more at current prices.

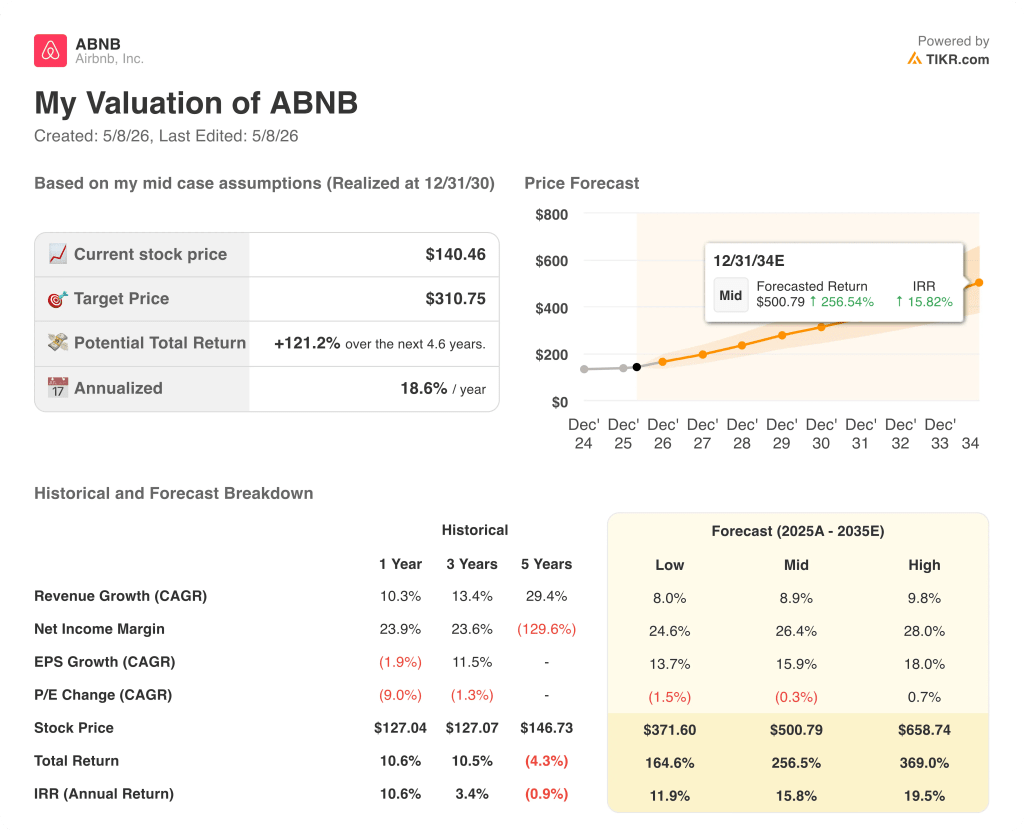

Airbnb stock appears undervalued at current levels, with TIKR’s mid-case model targeting $3111, implying a 120% total return over ~5 years at an annualized near 20% per year. The model assumes 9% revenue CAGR and a ~27% net income margin, both conservative relative to the current growth trajectory.

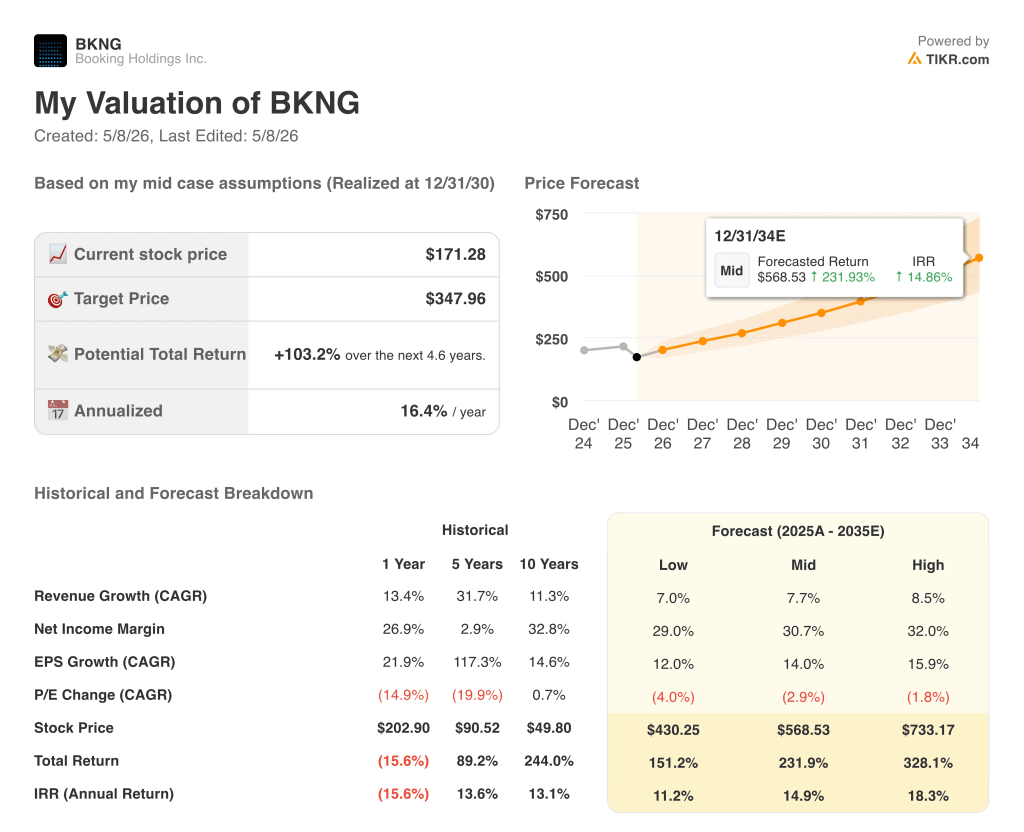

Booking Holdings stock appears undervalued at current levels, with TIKR’s mid-case targeting $348, implying an approximate 103% total return at an annualized ~16% per year. The model assumes around 8% revenue CAGR and a ~31% net income margin, consistent with consensus.

On a like-for-like horizon through 12/31/34, TIKR’s mid-case targets $505 for Airbnb stock at a 16% IRR versus $556 for Booking Holdings stock at a ~15% IRR, a 113 basis point annualized gap that favors ABNB for investors prioritizing compound return over absolute dollar gain.

The Growth Premium vs. The Scale Discount

The central argument for Airbnb stock is that its 28.3x NTM P/E is not a stretched multiple but a fair price for a business compounding faster, converting more of its revenue to free cash, and entering new verticals from a position of zero net debt.

- Revenue grew 18% in Q1 2026, beating guidance by 200 basis points, with the full-year outlook raised to low-to-mid teens.

- FCF margin of 37% in 2026E leads Booking’s 32%, and $8.74B in net cash gives Airbnb capital flexibility that Booking, with $2.83B in net debt, does not carry.

- Reserve Now, Pay Later drove approximately 3 points of nights booked growth in Q1 and remains in early global rollout, with desktop expansion and upfunnel merchandising still ahead.

- Hotels are growing at more than double the rate of the total business, the World Cup is expected to be the largest event in Airbnb history, and the May 20 product launch carries genuine upside optionality.

- TIKR’s IRR of 15.79% exceeds Booking’s 14.66% while ABNB trades at $141.66 versus BKNG’s $169.63, making the entry point asymmetrically attractive relative to the return profile.

The central argument for Booking Holdings stock is that its 16x NTM P/E near a 5-year low prices in too much pessimism for a business with $9.4B in forward FCF and accelerating U.S. momentum.

- NTM P/E of 16x sits well below the 5-year average of approximately 20x, implying meaningful re-rating potential as Middle East headwinds normalize in H2 2026.

- FCF generation of $9.4B in 2026E enabled $3.6B in share repurchases in a single quarter, with share count down 40% since 2014.

- U.S. room night growth accelerated for the fourth consecutive quarter to low-teens, with Booking.com’s direct channel growing double digits domestically.

- Operating margin of 35.2% already leads Airbnb’s 20.8%, and the $500M to $550M transformation program savings for 2026 are on track, providing a visible path to further expansion.

- Connected Trip transactions grew high-teens in Q1, roughly 3x total Booking.com transaction growth, and Genius tier Level 2 and 3 members now account for a high-50s percentage share of room nights.

Should You Invest in Airbnb or Booking Holdings?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Airbnb stock and Booking Holdings stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down for both companies.

You can build a free watchlist to track Airbnb and Booking Holdings alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ABNB and BKNG stock on TIKR for Free →