Key Stats for Accenture Stock

- 52-Week Range: $174 to $326

- Current Price: $175

- Street Mean Target: $250

- Street High Target: $320

- Analyst Consensus: 14 Buys / 4 Outperforms / 10 Holds / 1 Underperform / 1 Sell

- TIKR Model Target (Dec. 2030): $

What Happened?

Accenture plc (ACN) is a global professional services company that helps large enterprises transform their operations through technology, AI integration, and managed services.

Accenture stock has been cut nearly in half from its 52-week high of $325.71, yet the underlying business just posted its strongest bookings quarter in company history.

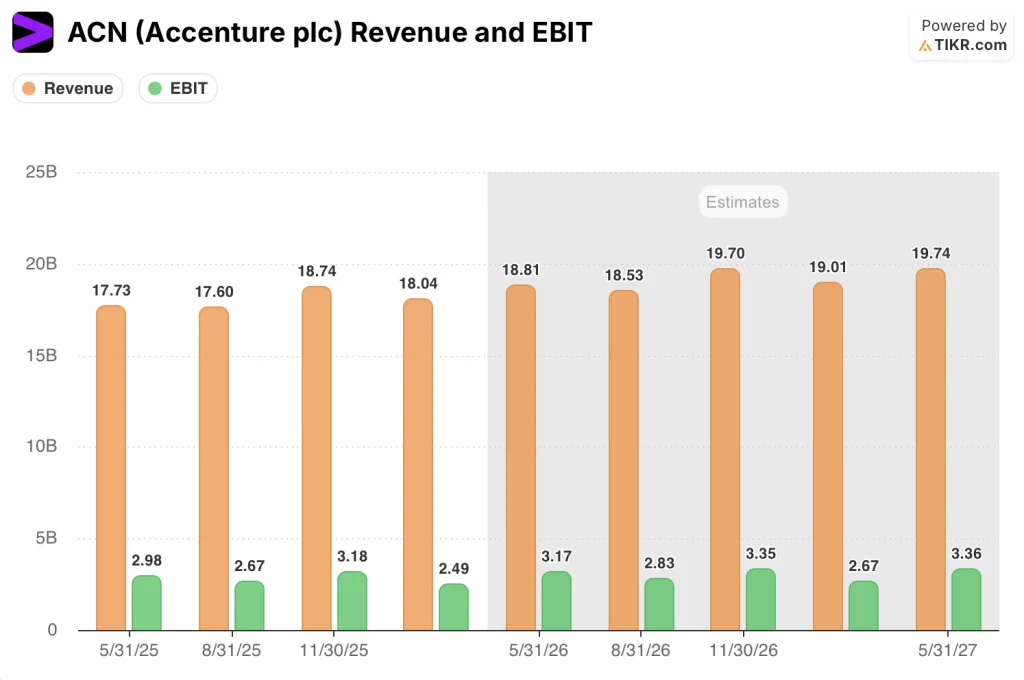

Q2 fiscal 2026 revenue came in at $18.04 billion, up 8.3% year-over-year, landing at the top end of the company’s guided range.

New bookings hit a record $22.1 billion for the quarter, pushing first-half bookings to $43 billion and giving the company its third consecutive quarter above the $20 billion mark.

A record 41 clients booked more than $100 million in a single quarter, up from the low-30s range just a year ago, a figure CEO Julie Sweet described as direct evidence of “the continued demand for reinvention at scale.”

Sweet went further on the AI demand picture, telling investors: “AI, as it stands right now, may turn out to be the most powerful technology breakthrough since electricity.”

The company raised its full-year acquisition budget to $5 billion, deploying $1.6 billion in Q2 alone across targets including Faculty (a U.K.-based AI-native services firm), cybersecurity leader CyberCX, and Ookla, a network intelligence data business generating $231 million in annual revenue through a non-FTE subscription model.

Free cash flow of $3.67 billion in Q2 beat Street estimates by nearly 196%, driven by DSO improvement and operational efficiency gains, and the company raised full-year free cash flow guidance by $1 billion to a range of $10.8 billion to $11.5 billion.

Wall Street’s Take on ACN Stock

Accenture stock is pricing in fear, but the forward revenue and earnings trajectory the bookings data implies tells a different story.

Revenue consensus estimates project around 6% growth in the next reported quarter, building on the 8.3% year-over-year print from Q2, and EBIT is forecast to reach around $3.17 billion in the next quarter against $2.49 billion in Q2, reflecting continued operating leverage as the company converts its record bookings backlog.

Of 29 analysts covering ACN stock, 14 carry Buy ratings and 4 Outperforms, with a mean price target of $249, implying around 43% upside from current levels; the Street is waiting for Accenture to demonstrate that its $5 billion acquisition budget accelerates non-FTE revenue conversion rather than diluting near-term margins.

The target range spans $210 on the low end to $320 on the high end, a spread that reflects a genuine bifurcation: bears believe macro uncertainty and U.S. Federal headwinds suppress growth into fiscal 2027, while bulls point to the record bookings trajectory and anniversary of the Federal drag in Q4 as the inflection that closes the gap toward the $300-plus range.

At 8.95x NTM EV/EBIT, less than half its historical mean of 18.82x and the lowest multiple the stock has ever traded at in the five-year dataset, Accenture stock appears undervalued against a backdrop of record bookings and EBIT forecast to grow around 6% next quarter as AI-driven managed services scale.

Sweet’s disclosure that over 85,000 AI and data professionals are already deployed, exceeding the company’s own 80,000 target ahead of schedule, reframes Accenture not as a company chasing AI demand but one already operating at scale inside it.

A deterioration in managed services bookings, which grew 10% in U.S. dollars this quarter, would undercut the recurring revenue conversion thesis and compress the multiple further.

The Q3 fiscal 2026 earnings call is the moment to watch: anniversary of the U.S. Federal drag hits that quarter, and the company has guided for Federal to return to growth, the specific data point that will tell investors whether the bookings backlog is converting at the rate the current mean target implies.

What Does the Valuation Model Say?

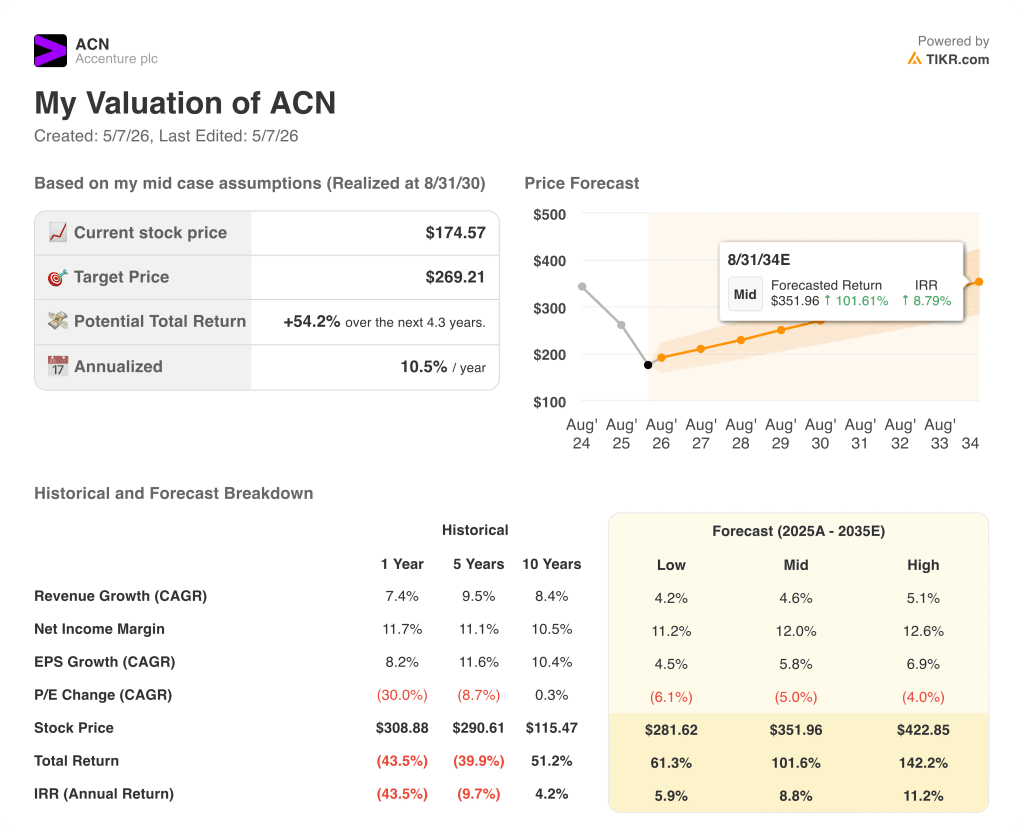

The TIKR model prices ACN at around $352 in the mid case (realized at August 2030), built on a revenue CAGR of roughly 5% and a net income margin expanding from 11.7% today toward 12%, assumptions conservative enough that even the low case (around $282, around 6% IRR) still implies material upside from current levels.

At $175, Accenture stock is trading at a price the TIKR model only assigns to its most pessimistic scenario, yet that low case still assumes positive returns, making the current price appear undervalued relative to any reasonable earnings and margin path the company’s own bookings data supports.

The argument hinges on whether the bookings-to-revenue conversion rate holds, and the gap between the low case and the current price is wide enough that investors are essentially being offered downside protection with asymmetric upside.

What Has to Go Right

- Q4 fiscal 2026 Federal business returns to growth as guided, removing a roughly 1% drag that has suppressed Americas revenue growth from a 6% underlying rate to a reported 3%

- Non-FTE revenue from the Faculty, Ookla, and DLB Associates acquisitions begins to show up in bookings and revenue mix within two to three quarters, justifying the $5 billion deployment at higher margins

- Managed services bookings, at $10.8 billion this quarter with a 1.2 book-to-bill, continue converting at current rates, driving the revenue CAGR toward the 5% to 6% mid case assumption

- AI-driven engagements move from proof-of-concept to production at scale across the 100-plus clients Accenture added to advanced AI programs this quarter alone, expanding average deal size and duration

What Could Go Wrong

- Escalation of the Middle East conflict disrupts the roughly $1 billion in annual revenue Accenture generates from the region, a risk CFO Angie Park explicitly cited in Q2 guidance commentary

- Macro uncertainty causes large enterprises to delay or cut the multiyear transformation programs that underpin the 41 clients booking over $100 million per quarter, compressing bookings below the $20 billion threshold in fiscal 2027

- Higher acquisition multiples for AI-native targets (Park confirmed the company is paying above historical averages for Faculty and similar assets) compress near-term EPS relative to the consensus estimates that drive the current mean price target of $249

- Revenue growth decelerates toward the 4% low case CAGR, leaving the stock fairly valued at $282 rather than the $352 mid case, a meaningful difference for investors buying at current levels

Should You Invest in Accenture Plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ACN stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Accenture Plc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ACN stock on TIKR for Free →