Key Stats for DoorDash Stock

- Current Price: $166.14

- Target Price (Mid): ~$909

- Street Target: ~$248

- Potential Total Return: ~447%

- Annualized IRR: ~44% / year

- Earnings Reaction (Q4 2025, reported 2/18/26): +1.62%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

DoorDash (DASH) has lost 42% from its 52-week high of $285.50, and the debate is loud. Bears see a company voluntarily compressing its own margins through heavy 2026 investment spending. Bulls see a logistics and software platform being built at a scale no competitor is currently matching. The unresolved question heading into today’s Q1 2026 earnings is whether DoorDash is spending recklessly or setting up a free cash flow inflection that the stock price does not yet reflect.

This article uses the Q4 2025 earnings transcript, TIKR data, and recent company announcements to work through that question.

Why the Market Sold Off and What It May Be Missing

The sell-off started in November 2025. Management announced plans to spend “several hundred million dollars more” in 2026 on a single global tech stack, autonomous delivery, and merchant software. DASH fell 17.45% the day after that Q3 announcement. By March 27, 2026, the peak-to-trough drawdown reached 47.97%.

The market read it as a profitability story going backward. The Q4 transcript tells a more specific story.

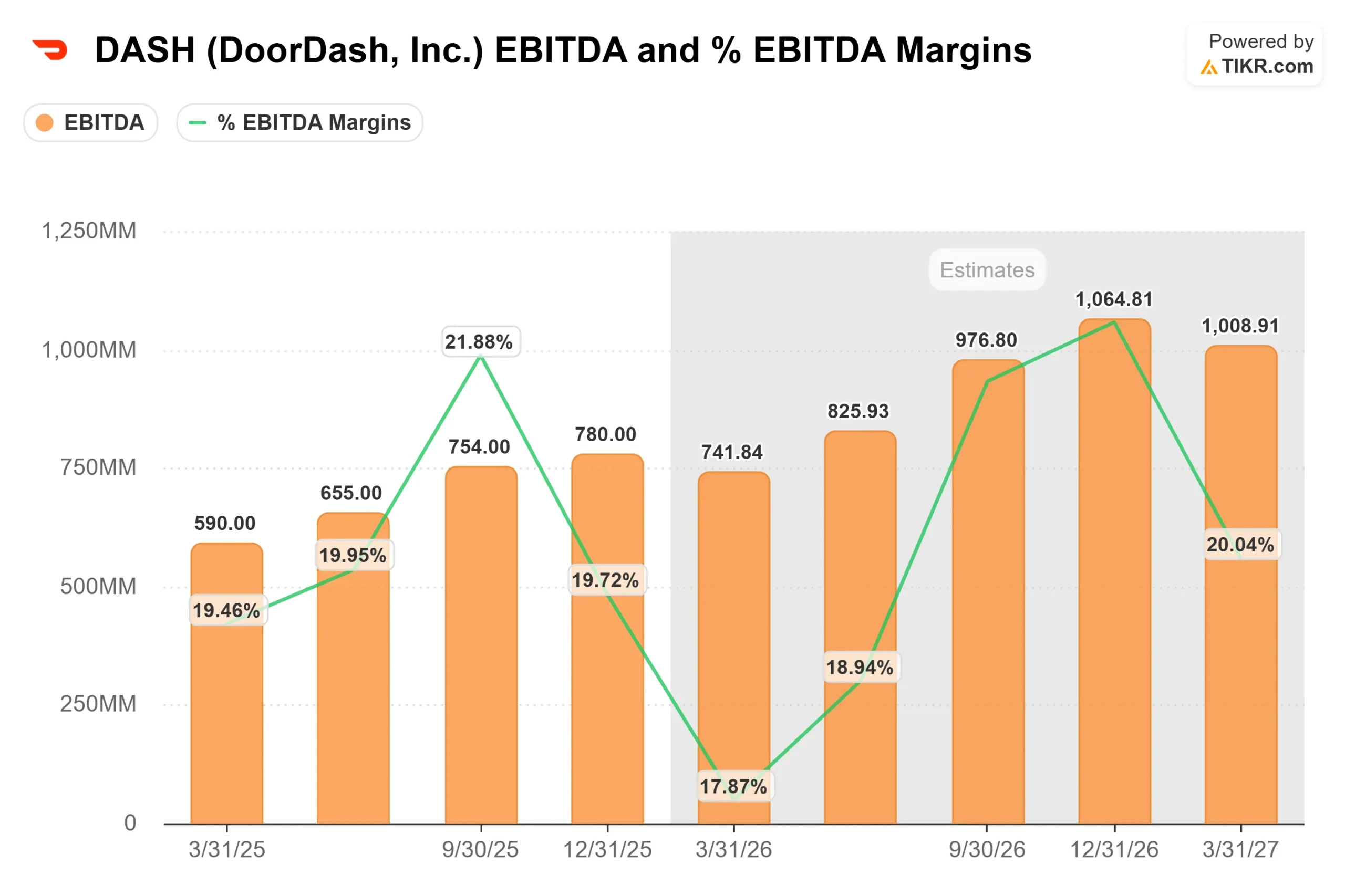

CFO Ravi Inukonda stated on the Q4 2025 earnings call: “My expectation for the full year EBITDA for ’26 has not changed since the last call. 2026 EBITDA margin is going to be up slightly compared to 2025, excluding ROO.” He also noted that the redundant costs from running parallel tech stacks would be concentrated mostly in 2026, with a smaller portion carrying into 2027 before rolling off entirely.

That framing matters. The investment cycle has a defined endpoint, a defined cost structure, and a defined payoff: faster global feature velocity, lower operational overhead, and a unified platform serving 40-plus countries through one engineering team.

The underlying financials confirm this spending is funded by genuine earnings power, not capital raises. LTM revenue reached $13,717 million as of December 31, 2025. Trailing free cash flow (the most recent twelve-month period) was $2,375.63 million, per TIKR.

See historical and forward estimates for DoorDash stock (It’s free!) >>>

Three Bets Behind the Spending

1. Collapsing three tech stacks into one. DoorDash currently operates separate platforms for DoorDash, Wolt, and Deliveroo. CEO Tony Xu explained the problem plainly on the Q4 2025 earnings call: “In order to ship one feature, you have to ship that three times in slightly different processes that make no sense.” Merging them means every product improvement built for the U.S. can be deployed instantly across Europe. Xu added that early results are already visible, with features proven in one market showing “immediate impact to the customer audience” when shipped to another.

2. Expanding grocery and retail beyond 30%. Thirty percent of DoorDash’s U.S. monthly active users (MAUs, meaning customers who place at least one order per month) now order from categories outside restaurants. CFO Inukonda confirmed on the Q4 call that the grocery and retail segment is expected to reach unit economic profitability in the second half of 2026, driven by larger basket sizes and improving logistics efficiency. The stated long-term goal is to get that 30% figure “closer to 100%.”

3. Building an autonomous delivery platform. DoorDash expanded its drone delivery partnership with Wing (an Alphabet subsidiary) to metro Atlanta in April 2026, offering deliveries in under 20 minutes. In late March 2026, DoorDash joined the $200 million Series C funding round for Also, a startup spun out of Rivian, to co-develop autonomous delivery vehicles. DoorDash’s proprietary “Dot” ground robot is already completing live deliveries in select markets. Xu described the autonomous delivery platform as “probably the most valuable part of what we’re building,” because it orchestrates handoffs across Dashers, drones, and ground robots, and any meaningful reduction in per-order delivery cost flows directly to margin.

See how DoorDash performs against its peers in TIKR (It’s free!) >>>

Deliveroo: Running Ahead of Plan

Deliveroo was the single largest driver of 2026 investment costs. Based on the Q4 transcript, the integration is outperforming early expectations.

Xu stated on the Q4 2025 earnings call: “We are growing much faster at the same profit contribution that we expected before the acquisition. We’re gaining share in its largest markets.” He credited daily product improvements and lessons applied from the earlier Wolt integration.

In February 2026, DoorDash exited Qatar, Singapore, Japan, and Uzbekistan under the Deliveroo and Wolt brands after a multi-month country review, concentrating resources on markets with the clearest path to sustainable scale. Management confirmed the exit left its full-year guidance unchanged. Pruning underperforming markets while doubling down on stronger ones is a sign of capital discipline, not global retreat.

International revenue reached $2,257 million in 2025, up from $1,319 million in 2024, per TIKR segment data.

What the Street Says and Where the TIKR Model Diverges

Wall Street is not bearish on DASH despite the drawdown. As of May 5, 2026, the TIKR Street Targets page shows 27 Buys, 8 Outperforms, 10 Holds, 0 Underperforms, and 0 Sells. The mean analyst price target is $248.48, roughly 49% above the current $166.14 price.

That consensus is constructive but conservative relative to what the TIKR Valuation Model implies at the 2030 horizon.

NTM EV/EBITDA (the ratio of enterprise value to expected EBITDA over the next twelve months) currently sits at 19.41x, down sharply from 34.35x in September 2025. The multiple has already been compressed significantly. Whether the business grows into it is the central question for long-term investors.

TIKR Advanced Model Analysis

- Current Price: $166.14

- Target Price (Mid): ~$909

- Potential Total Return: ~447%

- Annualized IRR: ~44% / year

See analysts’ growth forecasts and price targets for DoorDash stock (It’s free!) >>>

The TIKR mid-case model uses a revenue CAGR (compound annual growth rate) of approximately 18% through December 31, 2030. The two primary growth drivers are international platform scale (Deliveroo and Wolt reaching contribution profit positive on a single unified tech stack) and new verticals monetization (grocery, retail, and advertising as more MAUs adopt non-restaurant categories). The margin driver is operating leverage on fixed costs, with free cash flow margins projected toward approximately 27% by 2030, per consensus estimates on TIKR.

The upside case requires DoorDash to complete tech unification on schedule, deliver on the Deliveroo full-year EBITDA target, and show grocery and retail unit economics turning positive in H2 2026 as guided. The downside risk is a prolonged investment cycle. If tech replatforming stretches significantly into 2027 or autonomous delivery capital needs exceed current estimates, the free cash flow inflection bulls are counting on gets delayed.

Conclusion

The single number to watch in today’s Q1 2026 results (due after the close on May 6, 2026) is Marketplace GOV, meaning the total dollar value of all orders placed through DoorDash’s platform. Management guided $31.0 to $31.8 billion for Q1. A result within or above that range confirms core demand is intact even as investment spending weighs on near-term margins. DoorDash is absorbing deliberate short-term pain to build infrastructure designed to compound for years. The TIKR model suggests the market may be underpricing what comes out the other side by 2030.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in DoorDash?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DoorDash, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DoorDash alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze DoorDash on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!