Key Stats

- Current Price: ~$25 (May 5, 2026)

- Q1 2026 Revenue (HDMC): $1.1B, down 2% YoY

- Q1 2026 EPS: $0.22, down from $1.07 in Q1 2025

- Q1 2026 Global Retail Sales Growth: +8% YoY

- Full-Year 2026 HDMC Retail Units Guidance: 130,000 to 135,000

- Full-Year 2026 HDMC Operating Income Guidance: $10M to (40M) loss

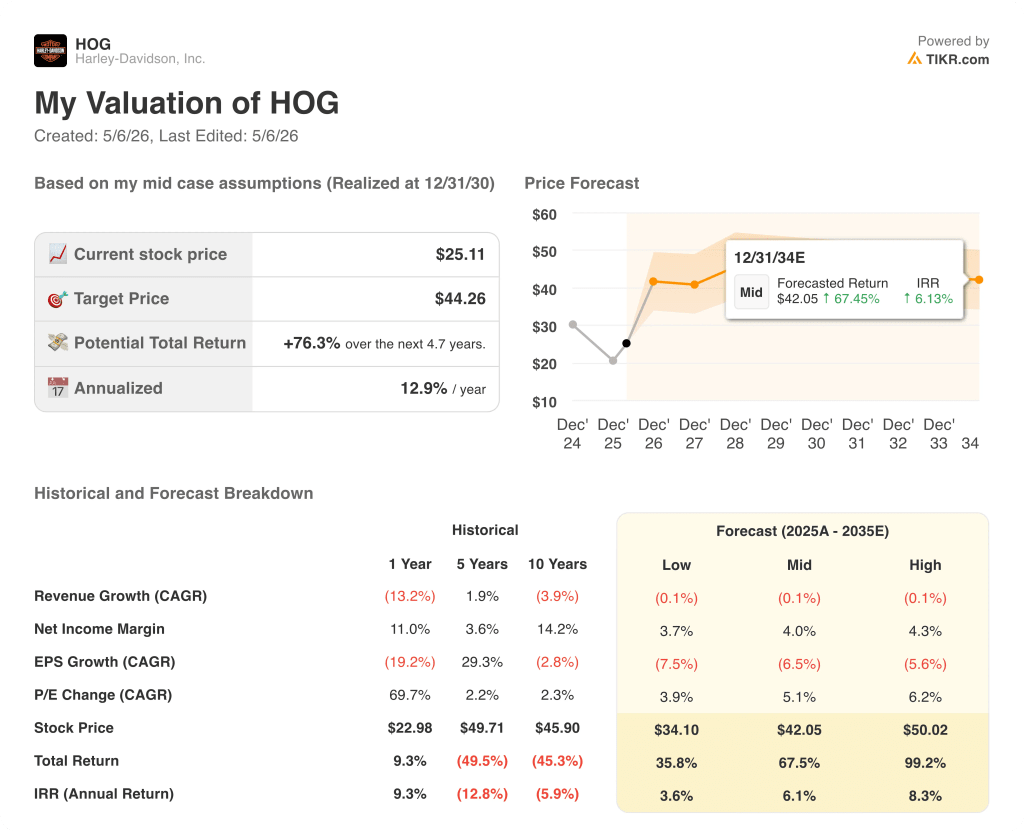

- TIKR Model Price Target: $44

- Implied Upside: ~76%

Harley-Davidson Stock Posts $0.22 EPS as Tariffs Crush Operating Income

Harley-Davidson stock (HOG) dropped to a reported EPS of $0.22 in Q1 2026, down sharply from $1.07 in Q1 2025, as tariff costs and restructuring charges overwhelmed a genuine improvement in retail demand.

Consolidated revenue fell 12% YoY, driven almost entirely by the HDFS segment’s 54% revenue decline after the company moved to a capital-light financial services model by selling a significant portion of its retail loan book.

HDMC segment revenue, the motorcycle manufacturing core, came in at $1.1B, down only 2% YoY, with motorcycles contributing $836M, Parts & Accessories and Apparel at $200M, and Licensing and Other at $20M.

The retail picture was the bright spot: North American retail sales of new motorcycles rose 14% YoY to approximately 24,000 units, with U.S. retail up 16%, driving global retail sales up 8% to approximately 34,000 units.

Harley-Davidson reached 38% of the U.S. 601cc+ market in Q1, up 2 percentage points YoY, according to CFO Jonathan Root on the Q1 2026 earnings call.

Tariffs were the primary earnings drag: HDMC absorbed $45M in new or increased tariff costs in Q1 2026 alone, against a full-year 2026 tariff cost forecast of $75M to $90M, an improvement from the prior range of $75M to $105M.

Operating expenses at HDMC totaled $248M in Q1, $49M higher YoY, split between $15M in restructuring charges tied to role eliminations and $34M in incremental costs covering higher warranty spend from product recalls, executive team transition costs, and expanded marketing.

HDMC operating income collapsed to $19M from $116M in Q1 2025, with consolidated operating income coming in at $23M versus $160M a year ago.

Management held full-year guidance unchanged: HDMC retail and wholesale units of 130,000 to 135,000 each, HDMC operating income of $10M to a $40M loss, and HDFS operating income of $45M to $60M.

CEO Artie Starrs used the Q1 call to formally unveil “Back to the Bricks,” a multiphase strategic plan targeting at least $150M in annualized cost savings by 2027, the return of the Harley-Davidson Sportster in 2027, and the launch of the Sprint lightweight motorcycle in the back half of 2026.

Share repurchases remained active: HOG bought back 6.6M shares worth $128M in Q1 2026 on a discretionary basis, bringing total repurchases to 26.8M shares valued at $726M since the program was announced in Q2 2024.

Harley-Davidson Stock Financials: Margin Compression Deepens Under Tariff Load

The Q1 2026 income statement shows an operation under significant structural pressure, with tariff costs and higher operating expenses compressing margins at every line while the retail recovery plays out at a pace that the income statement cannot yet reflect.

HDMC gross margin came in at 25.3%, down from 29.1% in Q1 2025, with tariff costs of $45M, net pricing and incentive spend to clear prior model year dealer inventory, unfavorable product mix, and higher supply management costs all working against the business simultaneously, according to Jonathan Root on the Q1 2026 earnings call.

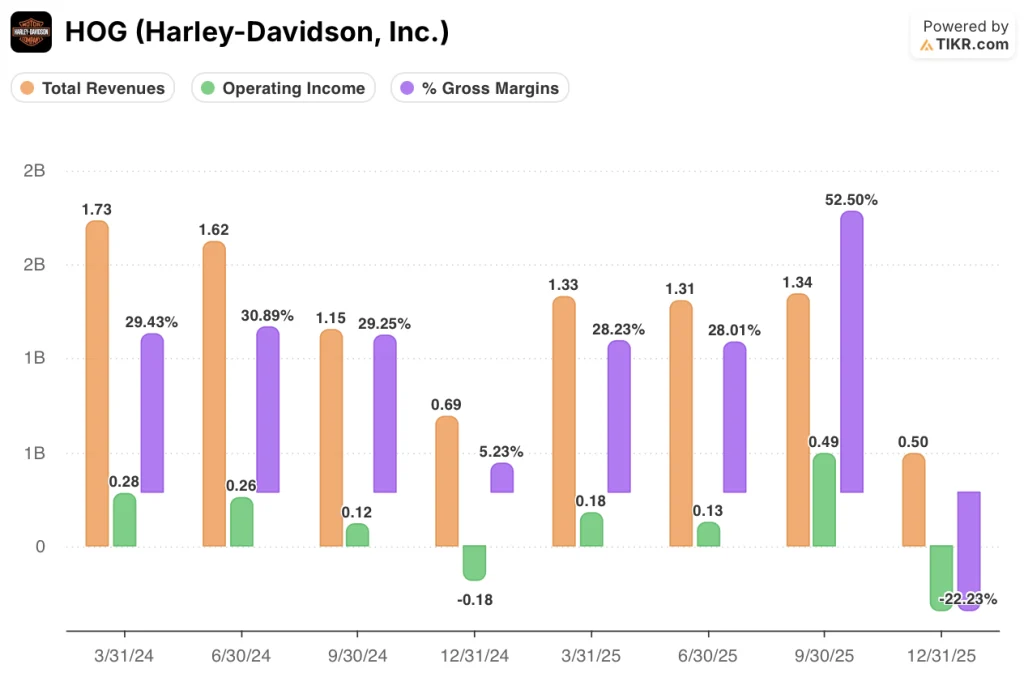

The multi-quarter revenue trend shows consistent seasonal compression: total revenues ran $1.7B in Q1 2024, declined to $1.6B in Q2, fell further to $1.1B in Q3, bottomed at $688M in Q4, then partially recovered to $1.3B in Q1 2025 before dropping to $496M in Q4 2025.

Gross margin on the consolidated basis compressed from 29.4% in Q1 2024 to 28.2% in Q1 2025, continuing a contraction arc that the HDMC-level figure of 25.3% in Q1 2026 confirms is still in progress.

Consolidated operating income was $279M in Q1 2024 and $176M in Q1 2025, establishing the scale of the deterioration that brought Q1 2026 consolidated operating income to $23M.

Management guided to HDMC operating income of between positive $10M and a negative $40M for full-year 2026, a range that reflects continued production deleverage as the company keeps production units below wholesale shipments to work down company inventory.

What Does the Valuation Model Say?

The TIKR model sets a price target of $44 for HOG stock, implying approximately 76% upside from the current price of ~$25, with the mid-case scenario projecting a total return of 68% over roughly 5 years at an annualized IRR of 6.1%.

The model’s mid-case assumptions are conservative: flat revenue CAGR of nearly none (0%), a net income margin recovery to 4%, and EPS CAGR of -6.5%, with the valuation re-rating driven primarily by P/E multiple expansion at a 5% annual CAGR rather than earnings growth.

Q1 2026 confirms the business is still in the reset phase: tariff drag, restructuring charges, and margin compression are all present simultaneously, which means the path to $44 is heavily dependent on the 2027 cost savings program, the Sportster relaunch, and the tariff environment stabilizing.

HOG stock at $25 prices in very little execution on Back to the Bricks, which means the risk/reward skews constructive for investors with a 3 to 5 year horizon and tolerance for near-term noise.

Harley-Davidson stock is not a near-term earnings compounder. It is a reset story where the valuation gap only closes if cost actions and new product launches translate into operating leverage, starting in 2027.

Harley-Davidson stock’s path to fair value requires the 2027 cost savings and Sportster relaunch to deliver operating leverage at a time when tariff costs and production deleverage are still compressing margins.

Thesis Intact

- North America retail sales rose 14% in Q1 2026 and U.S. market share reached 38% of the 601cc+ segment, up 2 percentage points YoY, before the Sportster or Sprint are in market

- Full-year tariff cost forecast improved to $75M to $90M from $75M to $105M, and management expects the quarterly tariff burden to decrease consecutively through the rest of 2026

- At least $150M in annualized cost savings are targeted for 2027 and beyond, with headcount reductions and COGS actions already underway in Q1

- Dealer inventory fell 22% YoY globally, with North America at approximately two-thirds current model year 2026 units, setting up a cleaner selling environment entering the main riding season

Thesis at Risk

- HDMC operating income guidance of $10M to a $40M loss for full-year 2026 leaves no margin for error if tariff policy shifts again or promotional costs accelerate

- Sprint production is being finalized outside the U.S. and carries tariff exposure that management has not fully quantified as of the Q1 call

- The entire $350M-plus 2027 EBITDA target assumes Sportster delivers at historical volumes of 35,000 to 40,000+ global units, a figure not yet tested against current consumer demand and pricing dynamics

- LiveWire is forecasting an operating loss of $70M to $80M for full-year 2026, a cash drain that persists with no committed Harley-Davidson funding beyond the 2025 loan

Should You Invest in Harley-Davidson, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Harley-Davidson stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Harley-Davidson, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HOG stock on TIKR for Free →