Key Stats

- Current Price: ~$137 (May 5, 2026)

- Q1 2026 Revenue: $4.4B, up 4% YoY

- Q1 2026 Non-GAAP Diluted EPS: $3.13, up 5% YoY

- 2026 Revenue Guidance (raised): $18.0B to $18.4B

- 2026 Non-GAAP Diluted EPS Guidance (raised): $12.10 to $12.50

- TIKR Model Price Target: $204 (mid case)

- Implied Upside: ~49%

Leidos Holdings Stock Delivers a Strong Q1 Earnings Breakdown

Leidos Holdings stock (LDOS) opened Q1 2026 with $4.4B in revenue, up 4% year-over-year, and non-GAAP diluted EPS of $3.13, up 5% from the prior-year quarter.

The Intelligence and Digital segment was the standout driver, with revenue up 7% year-over-year, including 6% organic growth, fueled by expanded intelligence community mission support and $22M from the Kudu Dynamics acquisition.

Non-GAAP operating margin in that segment improved from 9.7% to 10.2% year-over-year, according to CFO Chris Cage on the Q1 2026 earnings call.

Homeland revenues rose 6% year-over-year on surging demand for energy infrastructure engineering and air traffic control systems, though non-GAAP operating margin slipped from 9.4% to 8.5% due to changing requirements on a fixed-price program.

Defense revenues of $883M were roughly flat year-over-year, with integrated air defense growth offset by the wind-down of airborne surveillance programs; segment margin compressed from 9.8% to 8.3% due to a scheduled delay on a fixed-price development program.

Adjusted EBITDA came in at $614M for Q1, up 2% year-over-year, for an adjusted EBITDA margin of 14%.

Leidos raised full-year 2026 revenue guidance by $500M to a new range of $18.0B to $18.4B, raised non-GAAP diluted EPS guidance by $0.05 to a range of $12.10 to $12.50, and increased operating cash flow guidance by $50M to approximately $1.8B, according to Cage, driven primarily by the Entrust acquisition closing in March.

Leidos repurchased $200M of stock in Q1 as part of its capital deployment strategy, closing the quarter with $6.3B in debt and a gross leverage ratio of 2.6x.

Management flagged Q2 as the likely low point for both revenue growth and margins this year, attributing some Q1 outperformance to pull-forward from Q2, with the expectation that procurement activity accelerates meaningfully in the second half.

Leidos Holdings Stock: What the Income Statement Shows

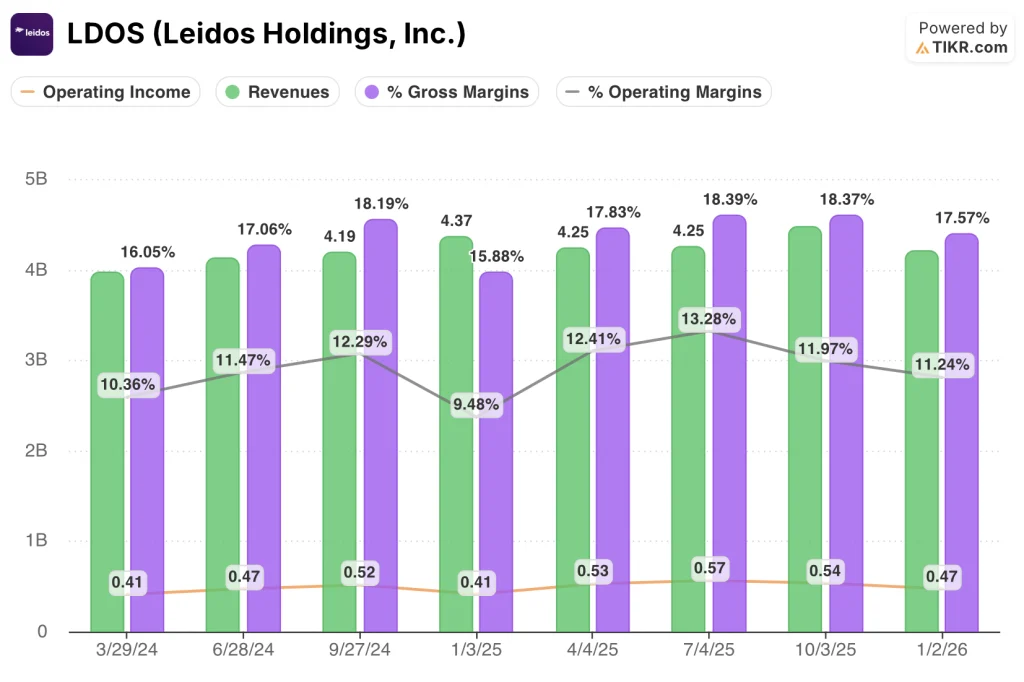

Leidos Holdings stock (LDOS) is operating in a period of margin normalization after a string of strong YoY operating income gains: the income statement picture is one of controlled compression rather than structural deterioration.

Gross margin came in at 17.6% in Q1 2026, down from 18.4% in each of the two preceding quarters, representing a step back from recent peaks.

Operating income was $470M in Q1 2026, down sequentially from $540M and $570M in the prior two quarters.

Operating margin settled at 11.2% in Q1 2026, compared to 12.0% and 13.3% in the preceding two quarters, and against 12.4% in the year-ago period.

Revenue came in at $4.21B in the quarter ended January 2, 2026 (Q4 2025), and $4.4B in Q1 2026, which represents a revenue step-up quarter-over-quarter that partly reverses a softer Q4 print.

The multi-quarter trend across eight quarters shows revenue oscillating in a $3.98B to $4.47B band, with operating margin peaking at 12.3% in September 2024 and receding since.

Cage attributed the Q1 margin softness to the absence of an insurance reimbursement in Q2 and near-term growth investment spending tied to framework agreements, Military OneSource, and Defense product-line programs, all of which Leidos expects to deliver higher-margin revenue as they scale.

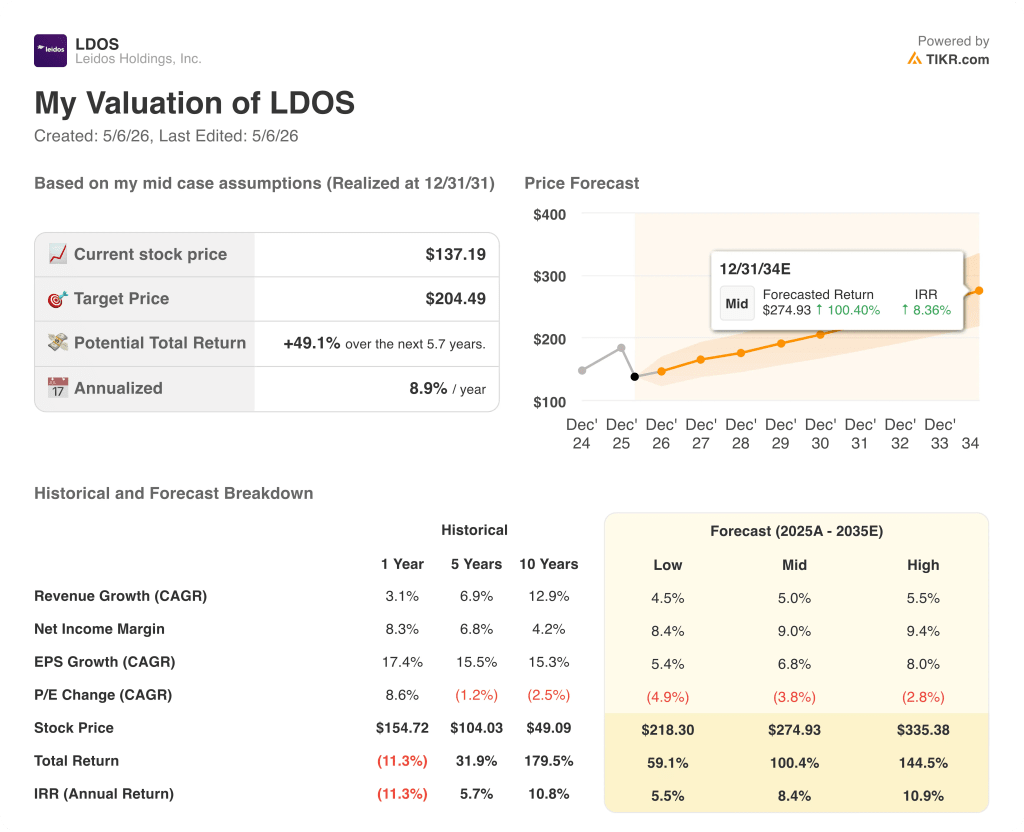

What Does the Valuation Model Say?

The TIKR model prices Leidos Holdings stock at $204 in its mid-case scenario, implying approximately 49% upside from the May 5 close of ~$137.

The mid-case assumes a revenue CAGR of 5% and a net income margin of 9% through 2035, with EPS growing at around 7% CAGR and P/E contracting at a 3.8% annual rate.

Q1’s raised guidance is consistent with the model’s growth assumptions: management’s $18B to $18.4B full-year revenue range tracks directionally with a 5% forward growth rate.

The investment case is modestly strengthened by this quarter: the Entrust acquisition is closing ahead of schedule, integration is described as ahead of plan, and the raised guidance is not contingent on an assumed market reacceleration that has yet to materialize.

Leidos Holdings stock is trading at a discount to TIKR’s mid-case fair value, with the near-term margin pressure representing a timing dynamic rather than a structural thesis change.

Leidos Holdings stock: does the raised guidance justify the discount?

The debate after Q1 is not whether the quarter was good. It’s whether the path from today’s 11% operating margin back to the 13%-plus range management is implying for the back half is achievable on the stated timeline.

What Has to Go Right

- Revenue reacceleration in Q3 and Q4 must materialize as management described, with Defense program ramps (IFPC, PAMS, ABADS-MD) transitioning from development cost drag to award fee performance

- Entrust integration synergies must begin flowing in 2027 as guided, with the refreshed $10B order pipeline converting at a rate that supports the 5% revenue CAGR in the model

- The Health segment’s volume staying elevated through the VA disability exam cycle must hold, protecting the 20%-plus margin profile Cage committed to on the call

- ALPS recognition under the $2.2B ABADS-MD contract and framework discussions on the AGM-190A small cruise missile must advance to serial production by year-end

What Could Still Go Wrong

- Q2 guidance explicitly signals the low point: margin compression plus elevated growth investment spending could disappoint if the H2 ramp is again described as “pull-forward” at the next call

- The SES joint venture closing in H2 removes segment revenue and shifts the contribution to equity method income, creating a period of visible top-line drag before synergies surface

- Defense operating margin at 8.3% for Q1 2026 is 150 basis points below Q1 2025, and the fixed-price development program drag is not expected to clear until late this year

- A book-to-bill ratio of 0.8 in Q1 (trailing 12 months at 1.1x) means near-term award conversion must pick up sharply in Q2 and Q3 to validate the H2 revenue step-up thesis

Should You Invest in Leidos Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Leidos Holdings stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Leidos Holdings stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LDOS stock on TIKR for Free →