Key Takeaways:

- NVIDIA is the world’s dominant AI chip company with $216B in annual revenue and operating margins above 60%, while Navitas Semiconductor designs gallium nitride (GaN) power circuits for fast chargers, AI data centers, and electric vehicles. These two semiconductor companies sit at very different stages of scale, profitability, and development.

- Analysts expect both companies to grow revenue, but at very different rates. NVIDIA is expected to grow revenue at around 50% annually while sustaining operating margins near 60% and generating over $97B in free cash flow. Navitas is expected to grow revenue at around 20% annually, but still runs deeply negative operating margins, near negative 182%.

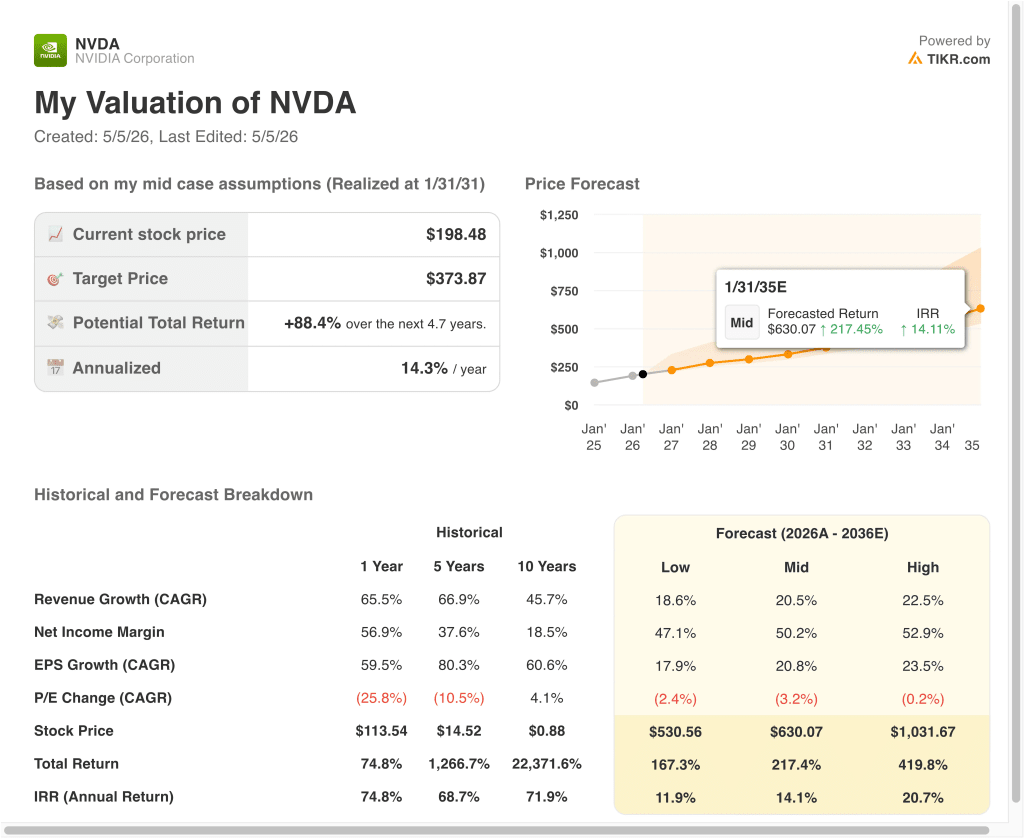

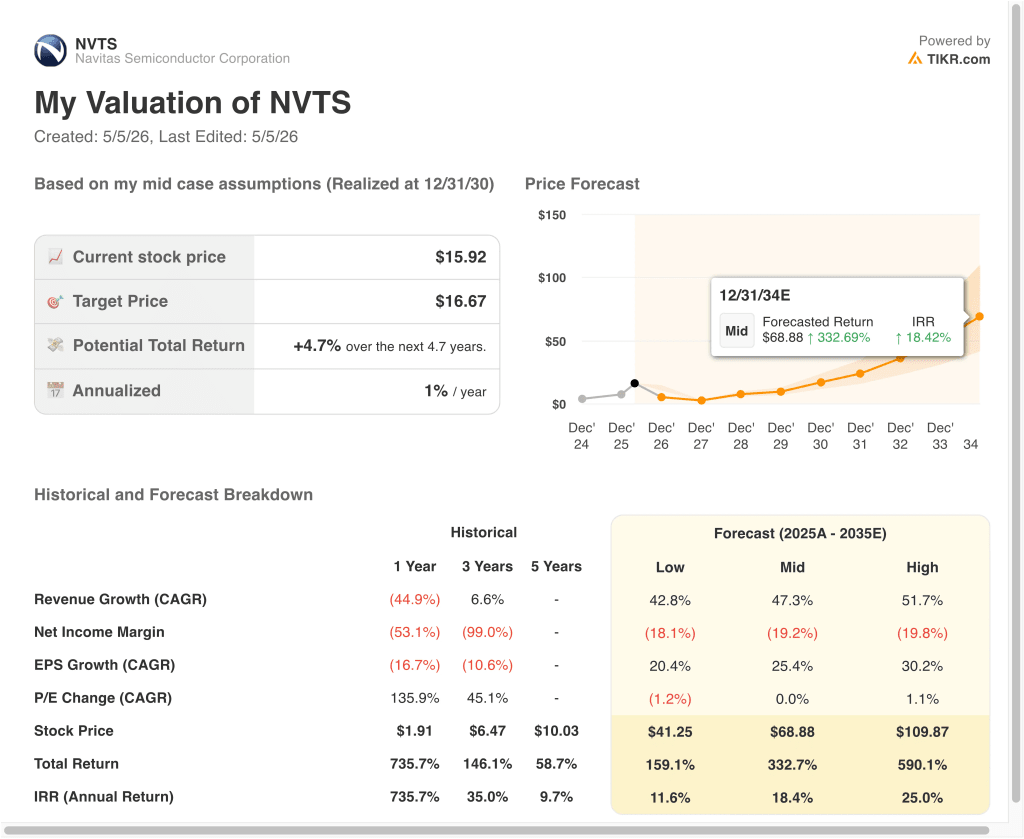

- Based on our valuation assumptions, NVIDIA stock could rise from $198 to around $374 per share over the next 4.7 years, delivering about 88% total return or around 14% annually. Navitas stock, by contrast, projects around 1% annualized return over the same near-term period, rising from $16 to roughly $17.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

What’s Happening?

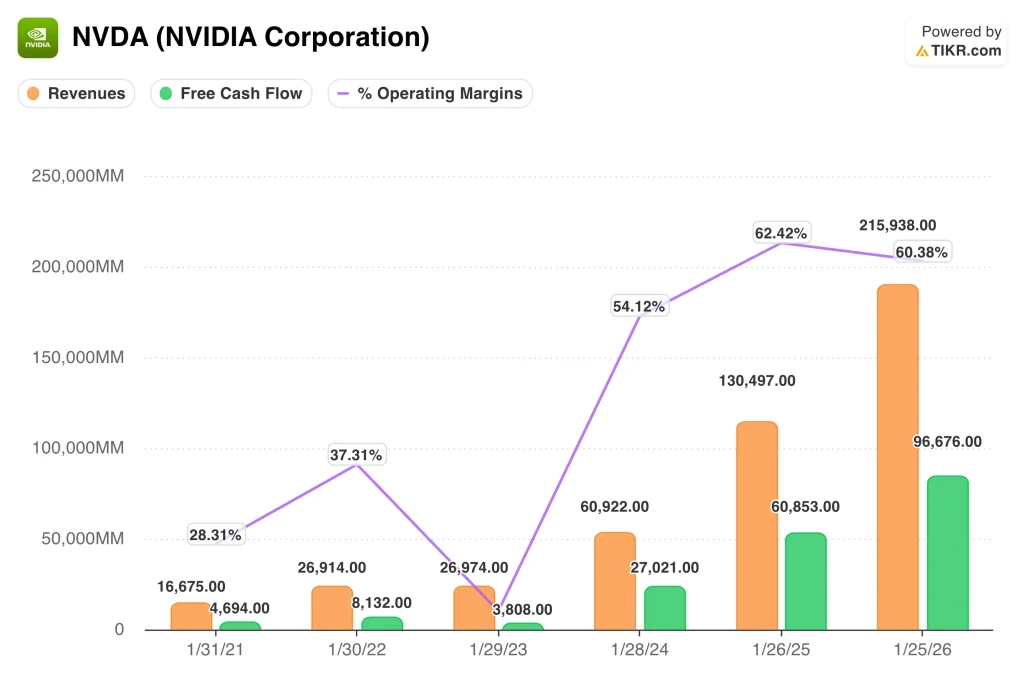

NVIDIA (NVDA) Corporation designs graphics processing units, or GPUs, the specialized chips that power artificial intelligence workloads. Its Data Center segment alone generated $62B in revenue during its most recent quarter. And the company posted $216B in total annual revenue for fiscal year 2026. NVIDIA also achieved operating margins above 60% while generating nearly $97B in free cash flow last year.

Navitas Semiconductor (NVTS) designs a very different type of chip. It focuses on gallium nitride, or GaN, power integrated circuits that convert electricity more efficiently than standard silicon. GaN produces less wasted heat, so it matters enormously as AI data centers consume growing amounts of electricity. And Navitas debuted a new 800V power board at NVIDIA’s GTC 2026 conference, targeting AI data center power systems directly.

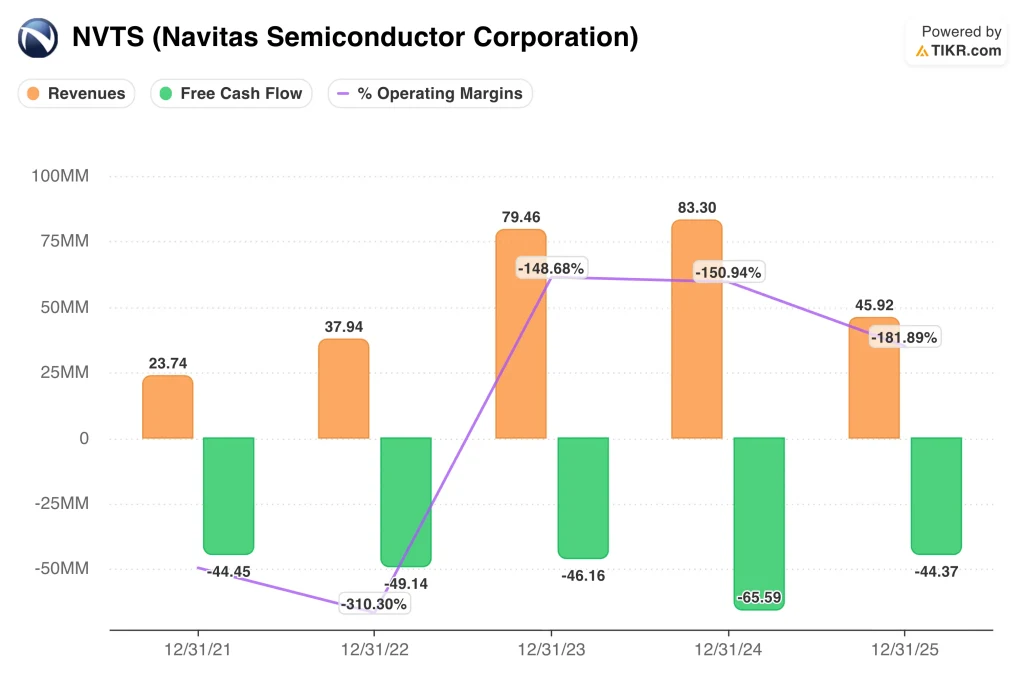

The scale difference between these two companies is stark. NVIDIA commands a market cap near $4.8 trillion and delivered 74% total return over the past year. But Navitas reported only $46M in revenue in 2025, down from $83M in 2024, and still has no profits.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Where These Two Businesses Start to Diverge

NVIDIA’s financial results are remarkable by any measure. Revenue surged from $16.7B in fiscal 2021 to $216B by fiscal 2026. And operating margins expanded from 28% to above 60% over the same period. Free cash flow also grew from $4.7B to nearly $97B, reflecting the extraordinary leverage in NVIDIA’s business model.

Navitas tells a very different story. Revenue grew from $24M in 2021 to $83M in 2024, but then dropped sharply to $46M in 2025. Operating losses deepened over that period, reaching around negative 182% of revenue last year. Free cash flow also stayed deeply negative at around negative $44M, so the company still relies on outside capital to fund its operations.

Revenue declined at Navitas for a specific reason. The company has heavy exposure to China, and export controls hit its chip sales hard in 2025. But demand for GaN power technology should recover as AI data centers need more efficient power conversion. So Navitas must scale revenue significantly before its operating margins can turn positive.

NVIDIA’s margin profile stands in sharp contrast. Its gross margin reached 71%, and its operating margin exceeded 60% last year. That level of profitability is exceptionally rare for a company growing at this speed. And it reflects NVIDIA’s pricing power in AI chips, where customers have very few alternatives.

See what analysts think about NVDA and NVTS stock right now (Free with TIKR) >>>

One Stock Trades on Earnings. The Other Trades on Potential.

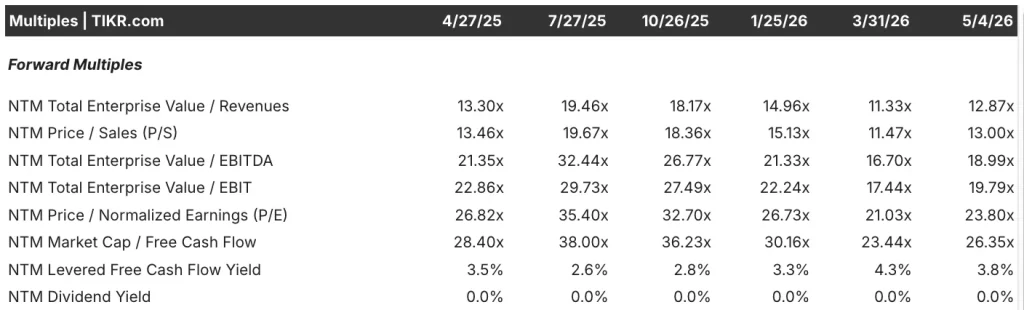

NVIDIA currently trades at around 24x forward earnings. Its forward EV/EBITDA multiple, which compares enterprise value to core operating earnings, sits at around 19x. Those multiples look elevated at first glance, but they reflect extraordinary and growing profits. And analysts maintain a consensus buy rating with a street target around $269.

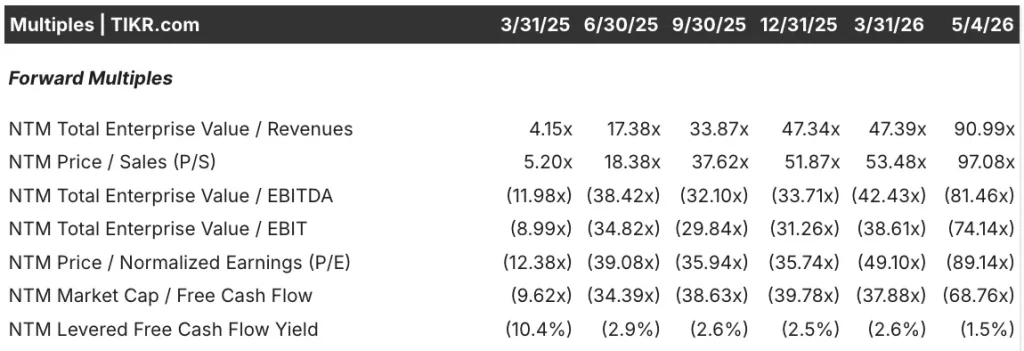

Navitas cannot be valued on traditional earnings multiples because it generates no positive earnings. Its forward enterprise value to revenue multiple sits at around 91x, very high given its current revenue scale. The forward EV/EBITDA and forward P/E multiples are both deeply negative, since the company still burns cash each quarter. So investors in Navitas are pricing in a massive revenue ramp that has yet to fully arrive.

The right multiple to use for each stock reveals a great deal. NVIDIA suits traditional earnings valuation because it generates enormous and growing profits. But Navitas fits a revenue multiple framework because earnings are still deeply negative. That distinction reflects the core difference between a proven business and a speculative growth story.

NVIDIA’s market cap to free cash flow ratio sits at around 26x, reasonable for a company generating nearly $97B annually. Navitas has a deeply negative free cash flow ratio because it still burns cash each quarter. Yet institutional interest in Navitas is growing, and BlackRock and Vanguard both added to their positions recently. And that growing fund interest reflects speculation that the GaN market will accelerate meaningfully in the years ahead.

See analysts’ full growth forecasts and estimates for NVDA and NVTS stock (It’s free) >>>

The Valuation Models Tell Very Different Stories

We analyzed the upside potential for NVIDIA stock based on its continued dominance in AI data center chips and infrastructure.

Based on estimates of around 21% annual revenue growth, around 50% net income margins, and a normalized EPS Growth (CAGR) of around 20x, the model projects NVIDIA stock could rise from $198 to around $374 per share.

That would be an 88% total return, or around 14% annualized return over the next 4.7 years.

We analyzed the upside potential for Navitas stock based on its GaN technology ramp in AI data centers, fast chargers, and electric vehicles.

Based on estimates of around 47% annual revenue growth, still negative net income margins improving toward around negative 19%, and a normalized EPS Growth (CAGR) once profitability eventually arrives, the model projects Navitas’ stock could rise from $16 to around $17 per share over the same period.

That would be roughly a 5% total return, or around 1% annualized return over the next 4.7 years.

Based on analysts’ consensus estimates, we note that the two models produce very different near-term outcomes. NVIDIA’s projections show meaningful upside, reflecting real earnings and enormous free cash flows.

But Navitas’s projections show minimal price appreciation in the near term, because the current valuation already embeds most near-term expectations. So the risk and return gap between these two stocks is very wide.

Build your own Valuation Model to value any stock (It’s free!) >>>

Which One Do You Actually Buy?

NVIDIA is not cheap, but it keeps earning its premium. Revenue nearly doubled year over year, and free cash flow reached nearly $97B annually. Few companies in history have grown at this speed while expanding margins so dramatically. So NVIDIA offers investors a rare combination of scale, profitability, and growth momentum.

Navitas is a very different kind of bet. Revenue actually fell sharply in 2025, and the company still burns cash each quarter. But GaN technology serves a real and growing need, and AI data center demand for efficient power conversion is accelerating. So Navitas could reward long-term investors willing to wait for meaningful revenue growth to arrive.

The choice between these two stocks depends on risk tolerance and investment horizon. NVIDIA suits investors who want proven profits and a leading position in the AI megatrend. But Navitas at $16 already trades well above the analyst street target of around $10, so near-term downside risk is real.

Going forward, NVIDIA offers proven earnings power, while Navitas suits investors comfortable with the speculative GaN revenue ramp and the volatility it brings.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Should You Invest in NVIDIA or Navitas?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NVDA or NVTS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NVDA or NVTS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze NVIDIA and Navitas stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!