Key Stats

- Current Price: ~$146 (May 5, 2026)

- Q1 2026 Revenue: $1.633B (+85% YoY, +16% QoQ)

- Q1 2026 Adjusted EPS: $0.33

- Q1 2026 GAAP EPS: $0.34

- Q1 2026 Adjusted Operating Margin: 60%

- Q1 2026 Adjusted Free Cash Flow: $925M (57% margin)

- Full-Year 2026 Revenue Guidance: $7.650B to $7.662B (~71% YoY growth)

- Full-Year 2026 Adjusted Operating Income Guidance: $4.440B to $4.452B

- Full-Year 2026 Adjusted Free Cash Flow Guidance: $4.2B to $4.4B

- TIKR Model Price Target: ~$496 (mid case, 12/31/30)

- Implied Upside: ~240% over ~4.7 years (~30% annualized)

Palantir Stock Posts 85% Revenue Growth in Q1 2026 — Its Fastest Rate as a Public Company

Palantir stock (PLTR) surged into its Q1 2026 earnings report on the back of its highest ever year-over-year revenue growth rate, with first-quarter revenue coming in at $1.633 billion, up 85% from the same quarter a year ago and 16% sequentially.

U.S. revenue crossed the triple-digit threshold for the first time since Palantir’s direct public offering, growing 104% year-over-year and 19% sequentially to $1.282 billion.

U.S. commercial revenue was the single loudest number in the report, reaching $595 million after growing 133% year-over-year and 18% sequentially.

According to Chief Revenue Officer Ryan Taylor on the Q1 2026 earnings call, absent a successful commercial customer program transitioning to a government customer, U.S. commercial growth would have been 143% year-over-year and 22% sequentially.

U.S. government revenue reached $687 million, up 84% year-over-year and 21% sequentially, driven by continued execution in existing programs and new awards including a USDA contract of up to $300 million awarded in April.

Total commercial TCV bookings reached $1.3 billion in Q1, up 42% year-over-year, with U.S. commercial TCV bookings hitting $1.2 billion for the third consecutive quarter above $1 billion.

According to CFO Dave Glazer on the Q1 2026 earnings call, trailing 12-month U.S. commercial TCV bookings reached $4.7 billion, a 115% increase from the prior 12 months.

Adjusted operating income came in at $984 million, representing a 60% adjusted operating margin.

GAAP net income was $871 million, a 53% GAAP net margin, with GAAP EPS of $0.34 and adjusted EPS of $0.33.

Adjusted free cash flow reached $925 million, a 57% margin, with the company ending the quarter holding $8 billion in cash and short-term U.S. treasury securities.

On the back of Q1 results, Palantir raised full-year 2026 revenue guidance to $7.650B to $7.662B, representing 71% growth year-over-year and a 10-point increase over the prior guidance midpoint.

The company also raised U.S. commercial revenue guidance to in excess of $3.224 billion, a growth rate of at least 120%, and lifted full-year adjusted free cash flow guidance to $4.2B to $4.4B.

Palantir Stock Financials: Margin Expansion at Full Acceleration

Palantir stock’s income statement tells a clean margin expansion story with no interruption across the past eight quarters.

Gross margin stood at around 82% in Q1 2024 and compressed slightly to 79% by Q4 2024, but recovered through 2025, reaching ~85% in Q4 2025.

Operating margin followed a similar but more dramatic arc: 12.8% in Q1 2024, dipping to 1.3% in Q4 2024, then accelerating sharply through 2025 to 19.9% in Q1 2025, 26.8% in Q2, 33.3% in Q3, and 40.9% in Q4 2025.

Operating income moved in lockstep: $80M in Q1 2024, a trough of $10M in Q4 2024, then compounding to $180M, $270M, $390M, and $580M across the four quarters of 2025.

According to CFO Dave Glazer on the Q1earnings call, Q1 2026 adjusted operating margin reached 60%, with adjusted operating income of $984 million.

Glazer also noted that Q1 adjusted expenses were $649 million, up 7% sequentially and 32% year-over-year, driven by continued investment in the AI platform and technical hiring, with further expense ramp expected across 2026.

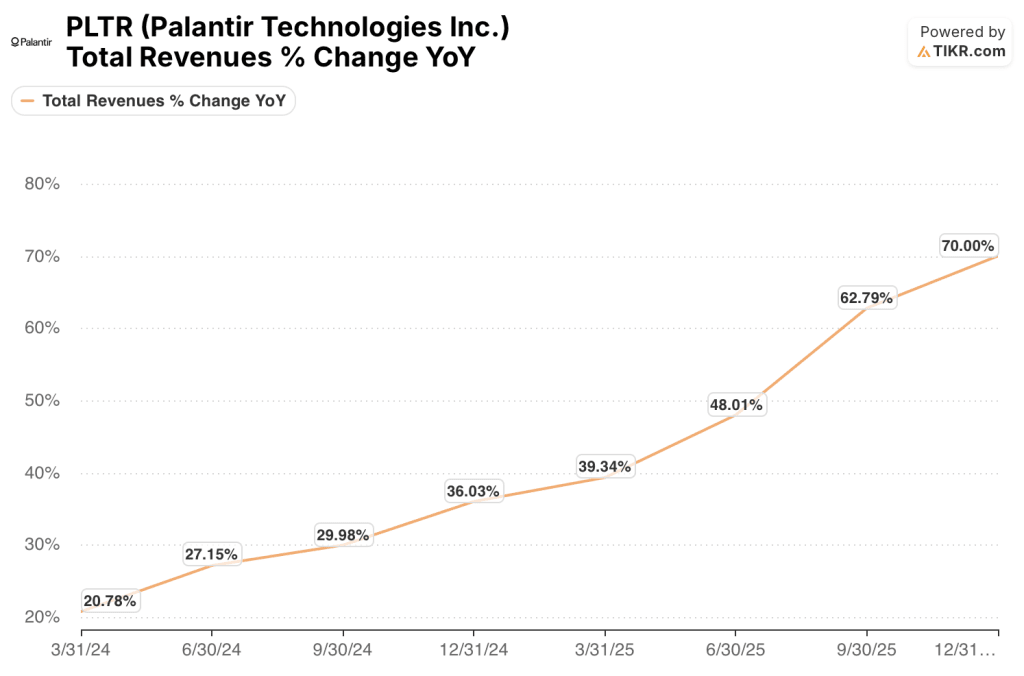

Revenue growth acceleration has been equally consistent: from 20.8% YoY in Q1 2024, the year-over-year rate climbed every quarter through Q4 2025 at 70%, and Q1 2026 pushed that rate to 85%.

What Does the Valuation Model Say?

The TIKR mid-case model prices Palantir stock at ~$496, implying approximately 240% upside from the current price of ~$146 over 5 years, or about 30% annualized through December 2030.

The mid-case assumes a revenue CAGR of ~25% and a net income margin of ~48%, with EPS growing at roughly 24% annually.

Q1 2026’s 85% revenue growth and 71% full-year guidance raise stress-test the model favorably: the bear risk in this framework is no longer about near-term execution but about whether the multi-year growth rate can sustain anything close to current velocity as the law of large numbers kicks in.

With $8 billion in cash, $925 million in Q1 free cash flow, and Rule of 40 now sitting at 145%, the investment case for Palantir stock is materially stronger coming out of this report than going in.

The investment argument for Palantir stock hinges on whether U.S. commercial and government demand can compound at scale long enough to justify a valuation that already prices in a decade of dominance.

What Has to Go Right

- U.S. commercial revenue must sustain the trajectory implied by full-year guidance of at least $3.224 billion, requiring continued 120%-plus growth; Q1’s $595 million and $1.2 billion in TCV bookings establish the foundation but execution must hold

- U.S. government revenue growth of 84% in Q1 and 21% sequentially must translate into a durable multi-year program spend cycle, supported by Maven usage doubling in 4 months and programs like ShipOS and Warp Speed scaling materially

- Adjusted operating margin at 60% in Q1 must either hold or improve as Palantir continues ramping expenses; the full-year adjusted operating income guidance of $4.440B to $4.452B requires sustained margin discipline through heavy technical hiring

- Net dollar retention of 150%, up 1,100 basis points sequentially, must reflect durable expansion at existing customers rather than a one-quarter spike

What Could Still Go Wrong

- International commercial revenue grew only 26% YoY and 5% sequentially to $179 million in Q1, a fraction of the U.S. trajectory, creating a structural single-market concentration risk if U.S. growth moderates

- Total remaining deal value of $11.8 billion and RPO of $4.5 billion are strong in absolute terms, but government contracts with termination for convenience clauses limit RPO’s predictive value and add program-level volatility

- Expenses growing 32% YoY in Q1 with further ramp guided for 2026 could compress margins faster than revenue growth offsets if commercial velocity shows any deceleration in Q2 or Q3

- PLTR stock currently trades at a premium that embeds the high scenario: the TIKR model’s high-case target of ~$1,008 requires ~25% annual EPS growth through 2035; any guidance revision downward would have an outsized valuation impact

Should You Invest in Palantir Technologies Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Palantir Technologies Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Palantir Technologies Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PLTR stock on TIKR for Free →