Key Stats

- Current Price: $159 May 1, 2026)

- Q1 2026 Revenue: $1,242M (+53% YoY)

- Q1 2026 Adjusted EPS: $1.09 (+63% YoY)

- Full-Year 2026 Revenue Guidance (Updated): +26% to +28% reported growth; +21% to +23% organic

- Full-Year 2026 Adjusted EPS Guidance (Updated): $4.45 to $4.55 (prior: $4 to $4.15)

- TIKR Model Price Target: $226 (mid case)

- Implied Upside: ~42%

nVent Electric Q1 2026 Earnings Breakdown

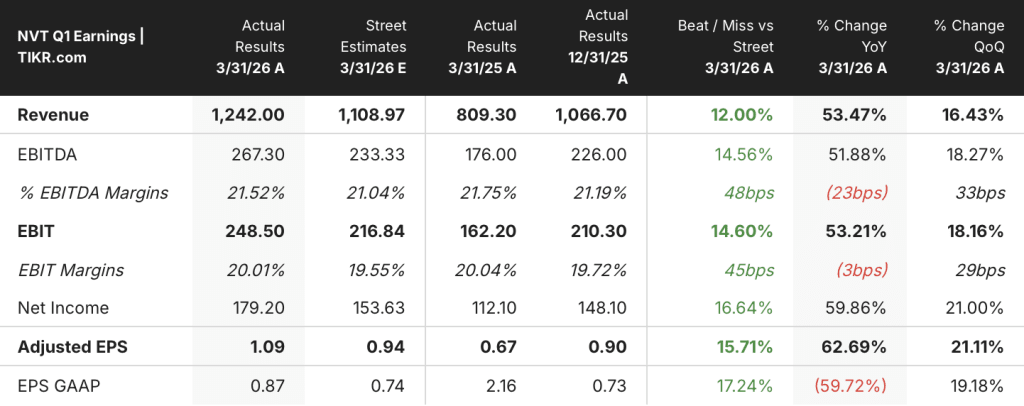

nVent Electric stock (NVT) delivered Q1 2026 revenue of $1,242M, up 53% year-over-year, with adjusted EPS of $1.09 growing 63% and landing well above the high end of guidance.

The Systems Protection segment was the engine of the quarter, with sales of $895M rising 76% total and 50% organically, according to CFO Gary Corona on the Q1 2026 earnings call.

Infrastructure within that segment grew more than 100% organically, driven by AI data center demand across both gray space and white space products.

New products contributed over 20 points to total company sales growth, against an Investor Day forecast of roughly 3 points, according to CEO Beth Wozniak on the Q1 2026 earnings call.

The Electrical Connections segment grew more sales of $347M, up 15% total and 8% organically, but segment income was flat at $85M, with return on sales falling 390 basis points year-over-year due to higher-than-expected copper inflation.

Corona noted that pricing and productivity actions taken during Q1 produced improving margins month-over-month within the segment, with further recovery expected in Q2 and the balance of the year.

nVent raised full-year 2026 adjusted EPS guidance to $4.45 to $4.55, up from an original range of $4.00 to $4.15, with organic sales growth guidance lifted to 21% to 23% from a prior range of 10% to 13%.

The company absorbed approximately $40M of tariff impact in Q1 and continues to model roughly $80M of incremental tariff headwind for the full year, with pricing and supply chain actions expected to fully offset inflation including tariffs.

Capital returns in Q1 included $50M in share repurchases and a 5% dividend increase, with the company exiting the quarter at 1.5x net leverage, well below its 2.0x to 2.5x target range.

Organic orders for nVent Electric stock rose approximately 40% in Q1, with most of that growth driven by AI data center demand, and backlog growing low double digits sequentially to $2.6B, extending visibility into 2027, according to Wozniak on the Q1 2026 earnings call.

nVent Electric Stock: Financials

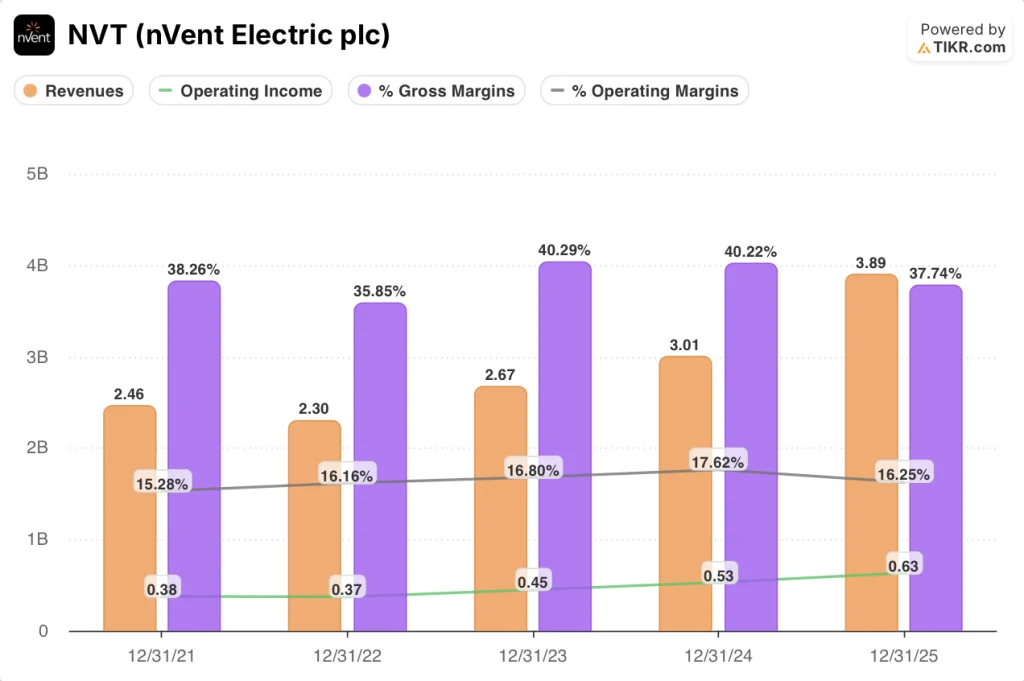

The Q1 2026 income statement reflects a company scaling aggressively into infrastructure demand, with revenue growth accelerating each quarter while operating margins held steady despite significant tariff and commodity pressure.

Revenue climbed from $730M in Q1 2024 to $810M in Q1 2025, then to $1,242M in Q1 2026, with YoY growth rates accelerating from a contraction in early 2024 to 11% by Q1 2025 and 53% in the most recent quarter.

Gross margin compressed from 39% in Q1 2024 to 39% in Q1 2025, a level broadly maintained through the intervening quarters despite volume surges.

Operating margin held at 20% in Q1 2026 on a reported basis, essentially flat year-over-year at 20%, as strong volume leverage in Systems Protection offset the margin drag in Electrical Connections.

Operating income reached $249M in Q1 2026, up 53% from $162M in Q1 2025, according to Corona on the Q1 2026 earnings call, reflecting roughly $60M of inflation including $40M in tariff impact absorbed in the quarter.

The Electrical Connections return-on-sales decline of 390 basis points was the primary margin headwind, driven by copper inflation, with Corona confirming on the call that remediation actions are producing visible improvement and that margins are expected to return toward historical levels by mid-year.

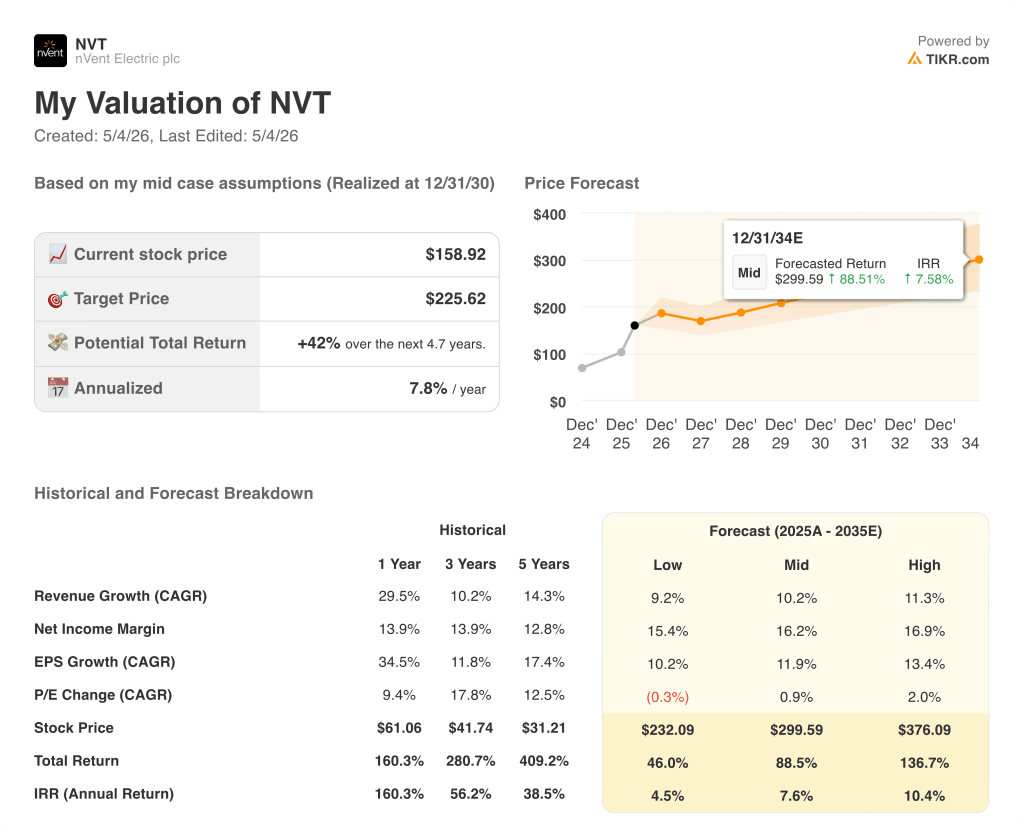

What Does the Valuation Model Say?

The TIKR mid-case model prices nVent Electric stock at $226, implying approximately 42% upside from the current price of $159 over a roughly 5-year horizon, with an annualized return of around 8%.

The mid-case assumes a revenue CAGR of 10% and a net income margin expanding to 16%, both of which look conservative given that Q1 2026 organic growth alone ran at 34% and the company just raised its full-year organic guidance to 21% to 23%.

The Q1 beat strengthens the investment case by demonstrating that nVent can sustain 20% operating margins while absorbing $40M of tariff headwind in a single quarter, removing a key execution risk from the model.

The base scenario holds: nVent Electric stock is priced below what the mid-case fundamentals support, and the Q1 print does more to pull forward the upside case than to introduce new risks.

nVent’s investment thesis hinges on whether the AI data center build-out sustains order velocity long enough to validate the capacity investments being made now.

What Has to Go Right

- Organic orders grew approximately 40% in Q1, with backlog reaching $2.6B and extending visibility into 2027, supporting the raised full-year organic growth guide of 21% to 23%

- New products contributed over 20 points to Q1 sales growth, with additional product launches planned for Q2 and Q3 in the Blaine, Minnesota facility that opened in Q1

- Infrastructure vertical is now 55% of Q1 sales, up from 12% at spin-off, providing structural exposure to AI data center CapEx that is accelerating rather than plateauing

- Systems Protection return on sales expanded 220 basis points year-over-year to 22.7%, validating that scale is translating to margin improvement in the highest-growth segment

What Could Still Go Wrong

- Electrical Connections return on sales fell 390 basis points to 24.4%, with copper inflation the primary driver; recovery is forecasted but not yet visible in the reported figures

- Tariff exposure stands at $170M all-in ($90M in 2025, $80M incremental in 2026), with the macro environment described by management as “highly fluid” as of the Q1 call

- Orders are concentrated in AI data center demand, which management acknowledged can be lumpy quarter-to-quarter; a deceleration in hyperscaler CapEx spend would disproportionately impact nVent Electric stock

- Net leverage at 1.5x sits well below target, and management signaled confidence in larger M&A; a poorly timed or mispriced acquisition during a high-execution period introduces integration risk

Should You Invest in nVent Electric plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up nVent Electric plc stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track nVent Electric plc alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NVT stock on TIKR for Free →