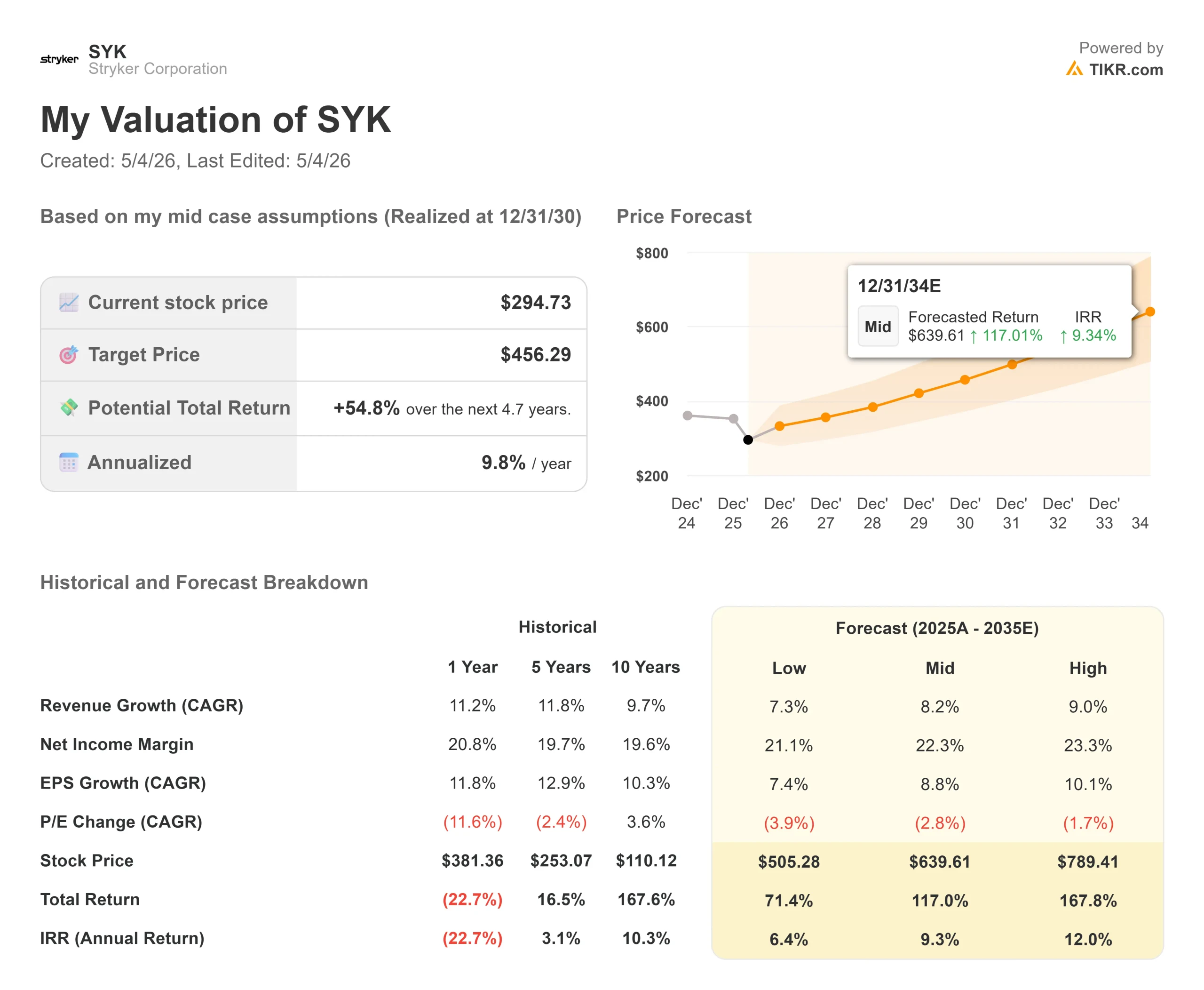

Key Stats for Stryker Stock

- Current Price: $294.73

- Target Price (Mid): ~$456

- Street Target: ~$419

- Potential Total Return: ~55%

- Annualized IRR: ~10% / year

- Earnings Reaction: -6.47% (May 1, 2026)

- Max Drawdown: -26.96% (May 1, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

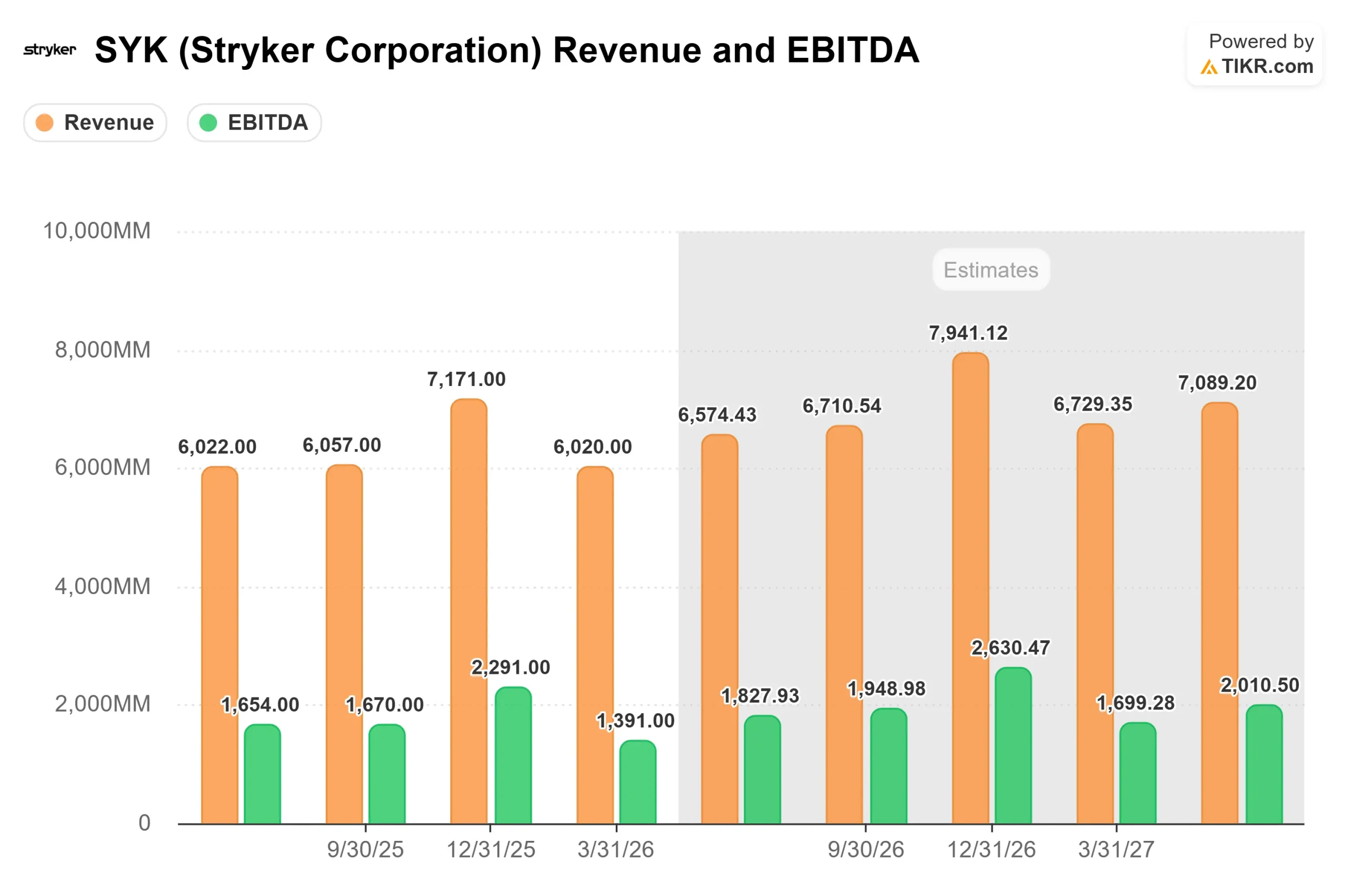

Medical device stocks rarely make headlines for geopolitical reasons. On May 1, shares of Stryker Corporation (SYK) fell 6.47% to close at $294.73, touching a 52-week low of $294.55, after the company reported a revenue miss of nearly 5% and an adjusted earnings miss of nearly 13%. The cause was not weak demand or a competitive setback. It was a cyberattack, allegedly carried out by an Iran-linked hacking group called Handala, that hit Stryker’s systems in late March and shut down global manufacturing for nearly three weeks.

Bulls say the damage is temporary. The order book remains elevated, procedure volumes held steady through the disruption, and management kept its full-year organic growth guidance of 8% to 9.5% intact. Bears ask a harder question: if three weeks of downtime can produce a $310 million revenue shortfall in one quarter, how confident can investors be that it all comes back? At a 52-week low and a valuation multiple not seen in years, the debate is now about recovery timing, not business quality.

What the Cyberattack Did to the Numbers

The timing of the attack was particularly damaging. It struck late in Q1, meaning Stryker absorbed a full quarter of optics from a partial quarter of disruption. The breach created two problems simultaneously: physical disruption to manufacturing and shipments, and a billing system failure that prevented some completed sales from being recorded as revenue during the quarter.

Actual Q1 revenue came in at $6.02 billion against an average estimate of $6.33 billion, a shortfall of around $310 million and a miss of 4.89%. Adjusted EPS of $2.60 missed the $2.98 consensus by 12.86%. Adjusted gross margin contracted 190 basis points to 63.6%, and adjusted operating margin fell 180 basis points to 21.1%, both driven by lost manufacturing absorption rather than any structural cost problem. Those figures come directly from CFO Preston Wells on the April 30 earnings call.

Wells was direct about the full-year outlook: “From a full year perspective, nothing has changed… we don’t expect much of a change overall in terms of what our margin performance will be for the year.”

The demand picture behind the headline numbers was healthy. Stryker delivered its best-ever Q1 for Mako robotic surgery installations, both in the U.S. and internationally, per VP of Finance Jason Beach on the call. The capital order book remained elevated entering Q2. Orders were not cancelled. Shipments were delayed.

CEO Kevin Lobo described the recovery in three phases: revenue recognition catch-up in Orthopaedics happening in Q2, deferred elective procedures rescheduled across Q2 through Q4, and make-to-order capital equipment in MedSurg recovering in the back half. “Endo and Medical are more capital-intensive.”

Lobo said on the call. “You would expect more of their recovery to occur in Q3 and Q4.” Stryker was fully operational by the week of April 1, and Lobo said customer relationships held: “There isn’t really any business I could think of that we’ve lost.”

See historical and forward estimates for Stryker stock (It’s free!) >>>

A Product Cycle the Market Is Ignoring

The Q1 noise is obscuring a product launch cycle that is genuinely strong. Pangea, Stryker’s trauma plating system, received European regulatory approval just before the call, adding to existing traction in the U.S. and Japan. Lobo called it “a tailwind that will last well into ’27 and even ’28.”

LIFEPAK 35, the company’s defibrillator platform, holds clearance across most global markets and carries a long replacement cycle. Mako Shoulder, extending the Mako 4 robot to shoulder replacement procedures, is expected to fully launch midyear. Mako RPS (Robotic Positioning System), a handheld robotic device for ambulatory surgery centers, is generating strong early feedback from surgeons. The Incompass Total Ankle is in the market, awaiting FDA clearance on its PROPHECY cut guides before adoption can accelerate, supported by a recently improved reimbursement rate for total ankle procedures.

On M&A, Stryker announced the pending acquisition of Amplitude Vascular Systems, a company developing intravascular lithotripsy (IVL) technology, meaning ultrasonic pressure waves used to break up arterial calcium deposits. The deal is expected to close in Q2 and will run through the existing Inari Medical sales force.

On competitive dynamics in orthopedics, Lobo was unambiguous: “Regardless of what competitive actions are occurring, we’re really not seeing that take away from customer interest in Stryker… our full year guidance assumes we will continue to outgrow the Orthopaedic marketplace by 200 to 300 basis points.”

See how Stryker performs against its peers in TIKR (It’s free!) >>>

How the Street Is Responding

Post-earnings analyst moves followed a clear pattern: targets cut, ratings mostly held. Raymond James lowered its target from $418 to $383 (Outperform), and TD Cowen cut from $387 to $355 (Hold). Stifel moved to $360 (Buy), Wolfe Research to $350 (Outperform), and BTIG to $379 (Buy). Bernstein SocGen reiterated Outperform with a $410 target, citing revenue visibility. Per TIKR’s Street Targets data, the mean analyst price target as of May 1, 2026, is $419.11, with 14 Buys, 8 Outperforms, 7 Holds, 1 No Opinion, and 1 Underperform across 30 analysts. At $294.73, the Street mean implies around 42% upside.

TIKR’s valuation multiples data adds context. NTM EV/EBITDA compressed from 22.00x in March 2025 to 15.31x as of May 1, 2026. NTM P/E moved from 27.63x to 18.84x over the same period. Both are meaningful discounts to Stryker’s own recent history. For a business with the consistency of a compounder stock, that kind of multiple compression either signals a real entry point or a prolonged recovery overhang.

TIKR Advanced Model Analysis

- Current Price: $294.73

- Target Price (Mid): ~$456

- Potential Total Return: ~55%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Stryker stock (It’s free!) >>>

The mid-case model uses a revenue CAGR of around 8% through 2030, driven by continued Mako platform expansion across new procedure types and international revenue acceleration as key products ramp outside the U.S. The mid-case net income margin assumption of around 22% is supported by management’s stated target of at least 150 basis points of additional operating margin improvement through 2028, building on the 20.8% margin Stryker printed in fiscal 2025 per TIKR’s actuals data.

The primary risk is the recovery timeline. A slower-than-expected back half compresses 2026 EPS and pressures forward estimates. On the downside, TIKR’s low case still implies around 71% total return by 12/31/30. The high case implies around 168%. The mid case at around 55% is a solid outcome for a business generating LTM free cash flow of around $5.1 billion per TIKR’s trailing data, with an NTM dividend yield of 1.2% at current prices.

Conclusion

Watch Q2 2026 organic revenue growth, reported in late July. If it comes in at or above 9%, the recovery is tracking on schedule, and the primary bear case weakens. Below 7%, back-half reliance becomes harder to defend, and full-year guidance faces pressure.

Stryker was hit by a one-time external shock, not a business deterioration. At a 52-week low and an NTM P/E of 18.84x, a level not seen in years, it offers a more compelling entry than any point in recent history for investors willing to hold through the Q2 and Q3 recovery confirmation.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Stryker?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Stryker, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Stryker alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Stryker on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!