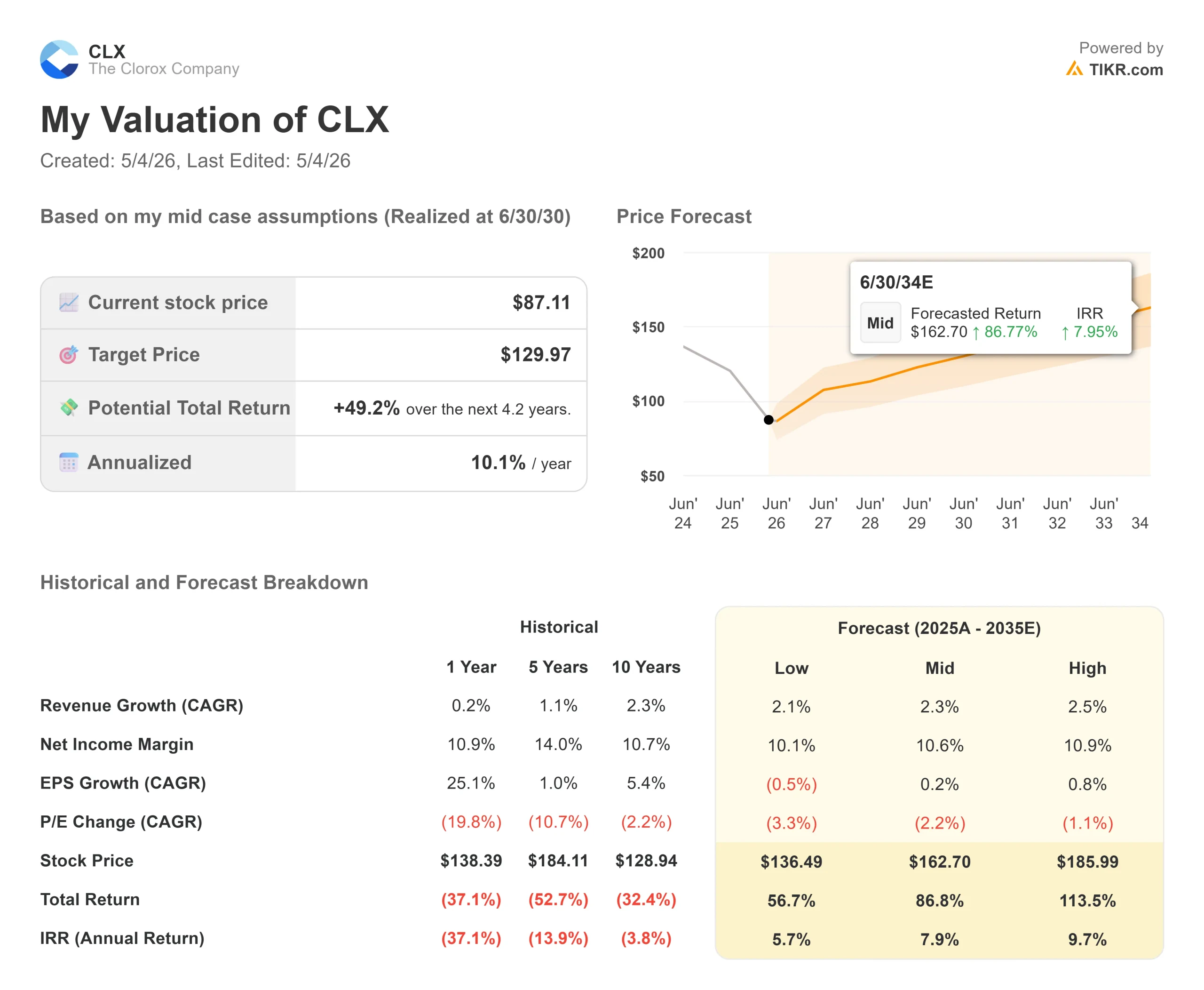

Key Stats for Clorox Stock

- Current Price: $87.11

- Target Price (Mid): ~$130

- Street Target: ~$115

- Potential Total Return: ~49%

- Annualized IRR: ~10% / year

- Earnings Reaction: -9.67% (April 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The Market Is Treating This Like a Broken Company

Consumer staples stocks are supposed to be boring. Clorox (CLX) has not been boring lately. Shares dropped 9.67% on May 1 after a guidance cut overshadowed a genuine earnings beat, pushing the stock to a 52-week low and 37.37% below its May 2025 peak. Bulls say the market is confusing temporary execution noise for permanent structural damage. Bears say the guidance trajectory keeps moving the wrong way, with almost no visibility into fiscal 2027. The question right now: is Clorox fixable, or is the damage deeper than management admits?

Clorox owns Clorox, Pine-Sol, Glad, Hidden Valley, Fresh Step, Brita, and Burt’s Bees. This is not a broken business model. It is a timing and cost problem, and those tend to resolve.

What Happened on April 30

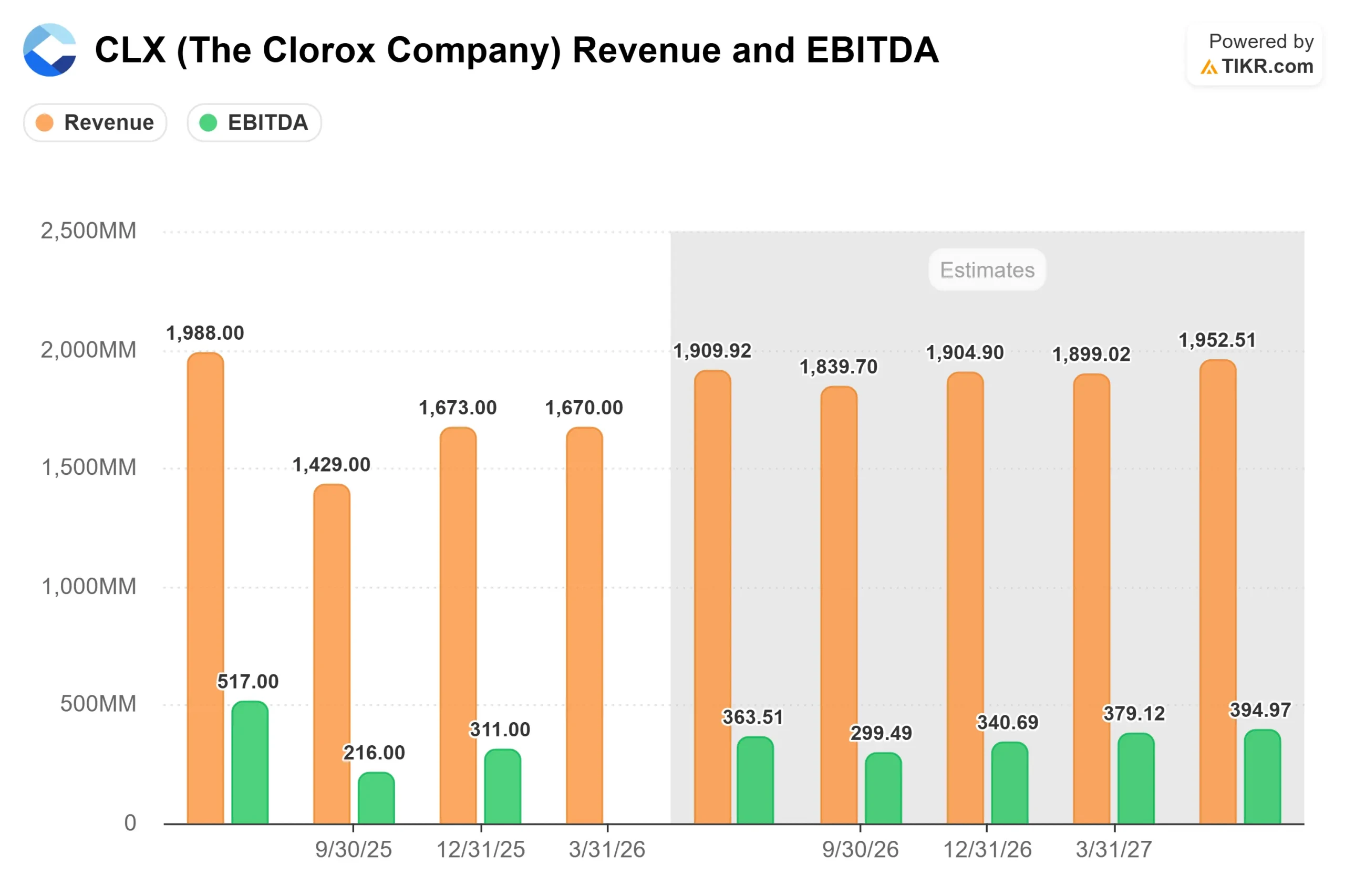

The Q3 numbers were actually solid. Net sales came in at $1,670 million, essentially flat year over year. Adjusted EPS hit $1.64, up 13% from $1.45 a year earlier and above the TIKR consensus estimate of $1.54. EBIT of $296 million beat the $273.20 million consensus by 8.35%.

What broke the stock was the updated full-year outlook. Clorox now expects fiscal 2026 net sales to fall ~6%, organic sales to drop ~9%, and gross margin to contract 250 to 300 basis points versus the prior guidance of down 50 to 100 basis points. Adjusted EPS guidance moved to $5.45–$5.65 from $5.95–$6.30. Three things hit simultaneously: a 7.5-point organic sales drag from ERP inventory normalization reversing, GOJO integration costs, and a fresh $20–$25 million Q4 oil-price headwind from the Middle East conflict. Analyst price targets were cut sharply following the release, with the Street’s low target now at $83 and the mean at around $115, per TIKR.

See historical and forward estimates for Clorox stock (It’s free!) >>>

What the Market May Be Underweighting

On the earnings call, CEO Linda Rendle identified two problem areas with notable specificity.

Fresh Step cat litter is undergoing a full brand reset, with new UPCs, new claims, new pack sizes, and renamed items. Changing UPCs forces a hard retailer conversion that creates temporary out-of-stocks. Rendle acknowledged that shelf placement was imperfect in some locations, but was clear that this was a transitional problem. Critically, the litter category itself is growing mid-single digits. Clorox is losing share in a growing category, which is recoverable.

Hidden Valley faced a different challenge: the food category declined mid-single digits in Q3 versus an expected low-single-digit decline, pressured by heavy competitor discounting and early consumer trends around GLP-1 medications. Clorox reversed a prior packaging misstep and launched protein-forward and Avocado Oil products that appear to have driven a share inflection late in the quarter.

The most important message came from CFO Luc Bellet. The ERP (enterprise resource planning) implementation is complete. The extra logistics and fulfillment costs that dragged margins for a year were near zero by the end of Q3. Bellet was direct: “Towards the end of the quarter and this month, we incurred very minimal costs.” If ERP costs are truly done, the gross margin floor may already be in.

The GOJO Wildcard

Clorox closed its acquisition of GOJO Industries, the maker of Purell hand sanitizer, on April 1, 2026. GOJO generates approximately $800 million in annual revenue, growing at a mid-single-digit pace, with more than 80% of sales through B2B (business-to-business) channels serving hospitals, schools, and offices.

The year-one math is dilutive on the surface. GOJO carries slightly lower gross margins than Clorox’s average, adding about 50 basis points of dilution in year one. Q4 carries an additional one-time 150 basis-point headwind from inventory step-up accounting that does not repeat. Interest expense rises roughly $30 million in Q4 and approximately $110 million above the prior $100 million annual run rate in fiscal 2027.

But GOJO adds $200 million of revenue to Q4 alone. Management expects at least $50 million in run-rate cost synergies beginning in years two and three, with GOJO accretive to EBITDA over time. Rendle was unequivocal: “My confidence remains incredibly high on this acquisition, both from a strategic perspective and the fact that it gives us additional growth exposure in health and hygiene.”

See how Clorox performs against its peers in TIKR (It’s free!) >>>

Is the Valuation Attractive?

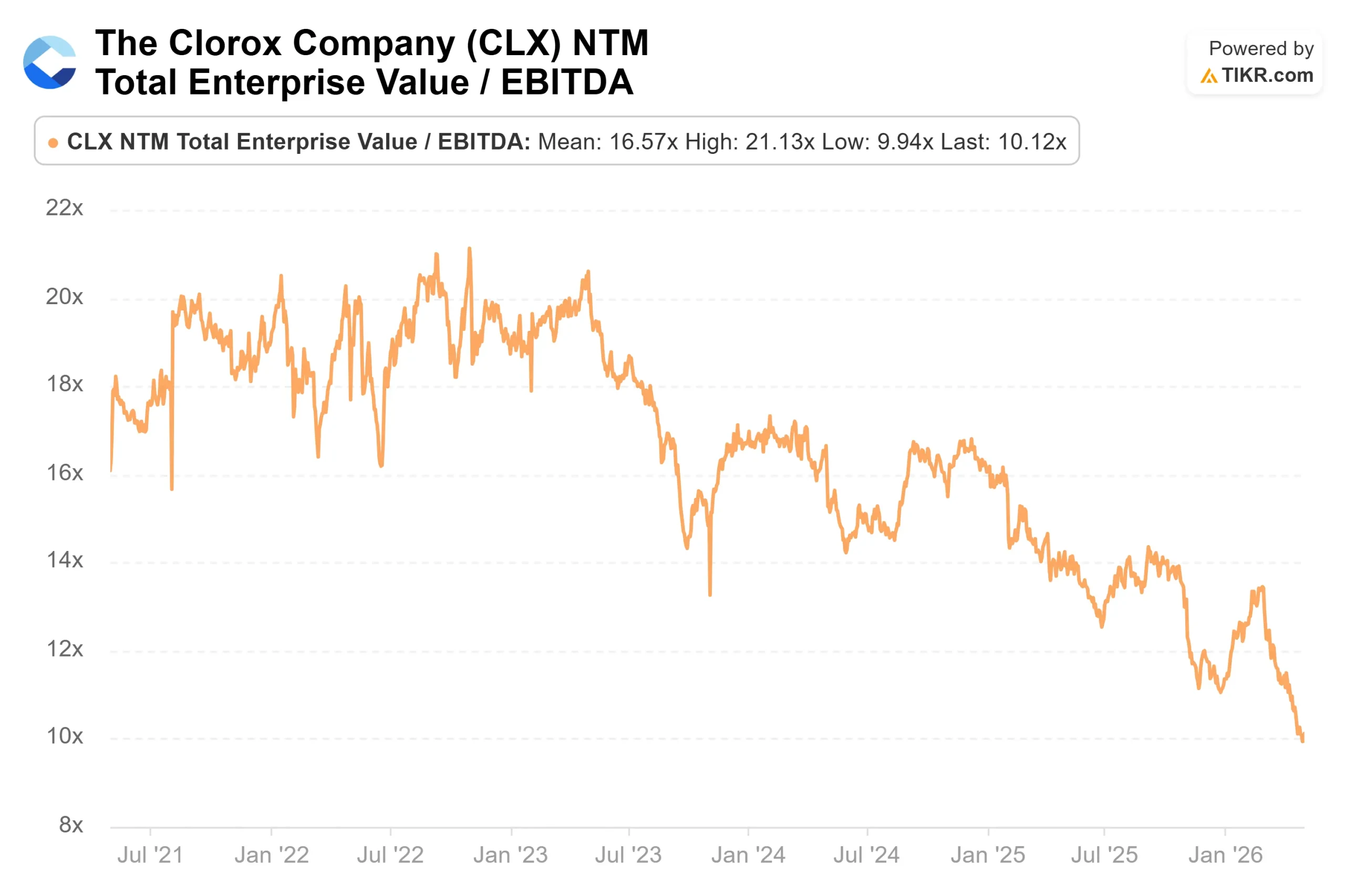

CLX now trades at 10.12x NTM EV/EBITDA, down from 14.48x a year ago, with an NTM P/E of 14.41x and a dividend yield of 5.8%. On TIKR’s Competitors page, Kimberly-Clark (KMB) trades at 10.29x NTM EV/EBITDA, and Reynolds Consumer Products (REYN), which competes in the trash bag category with its Hefty brand, trades at 8.90x. CLX at 10.12x sits slightly above REYN and in line with KMB. Given GOJO’s long-term growth optionality, that positioning is defensible.

The bear case is real. The Street’s lowest analyst target sits at $83, below today’s price. Organic sales are falling 9% this year, fiscal 2027 guidance will not come until August, and free cash flow visibility is limited. With consensus estimates projecting net debt around $5.1 billion post-GOJO and net debt/EBITDA around 4.1x for fiscal 2026 per TIKR, the balance sheet has less room for error than usual.

The bull case rests on three management commitments: ERP costs are done, GOJO synergies begin in year two, and innovation outside of Litter is performing above expectations. Distribution points grew more than 5% in Q3. If those shelf gains convert to velocity as resets complete, the revenue picture improves faster than consensus implies.

TIKR Advanced Model Analysis

- Current Price: $87.11

- Target Price (Mid): ~$130

- Potential Total Return: ~49%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Clorox stock (It’s free!) >>>

TIKR’s mid-case model uses a revenue CAGR of around 2% through 6/30/30, driven by GOJO’s $800 million revenue base growing mid-single digits and a gradual recovery in Clorox’s core categories. The net income margin is modeled at around 11% in the mid case, rising as ERP costs roll off and cost savings from integrated margin management take hold.

The mid-case target of around $130 implies roughly 49% total return through 6/30/30, or around 10% annualized. The high case reaches around $186 on faster synergy realization. Even the low case at around $136 still implies meaningful upside from current prices. The primary risk is oil: at around $100 per barrel, Q4 faces a $20–$25 million gross margin headwind with no mitigation yet deployed. Leverage at around 4.1x net debt/EBITDA limits the company’s flexibility if costs stay elevated.

The Street mean target is around $115, about 32% above current levels. The analyst breakdown per TIKR as of 5/1/26: 2 Buys, 1 Outperform, 13 Holds, 2 No Opinions, 1 Underperform, 2 Sells. Consensus is cautiously neutral, which historically shifts fast when a recovery quarter confirms the cost narrative.

Conclusion

Watch gross margin at the Q4 FY2026 report, expected in late July or early August 2026. If gross margin prints above 43.5%, the ERP cost story is closed, and GOJO one-time charges are confirmed non-repeating. If it comes in below 43%, the fiscal 2027 debate reopens. At around 10x forward EBITDA with a near 6% dividend yield, the market may already be pricing in the worst. Whether that is a floor or just a waypoint depends almost entirely on oil prices and what management says in August.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Clorox?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Clorox, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Clorox alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!