Key Takeaways:

- FedEx Corporation provides transportation, e-commerce, and business services across more than 220 countries. Its DRIVE transformation program and Network 2.0 initiative are targeting more than $1 billion in permanent structural cost savings through automation and route consolidation.

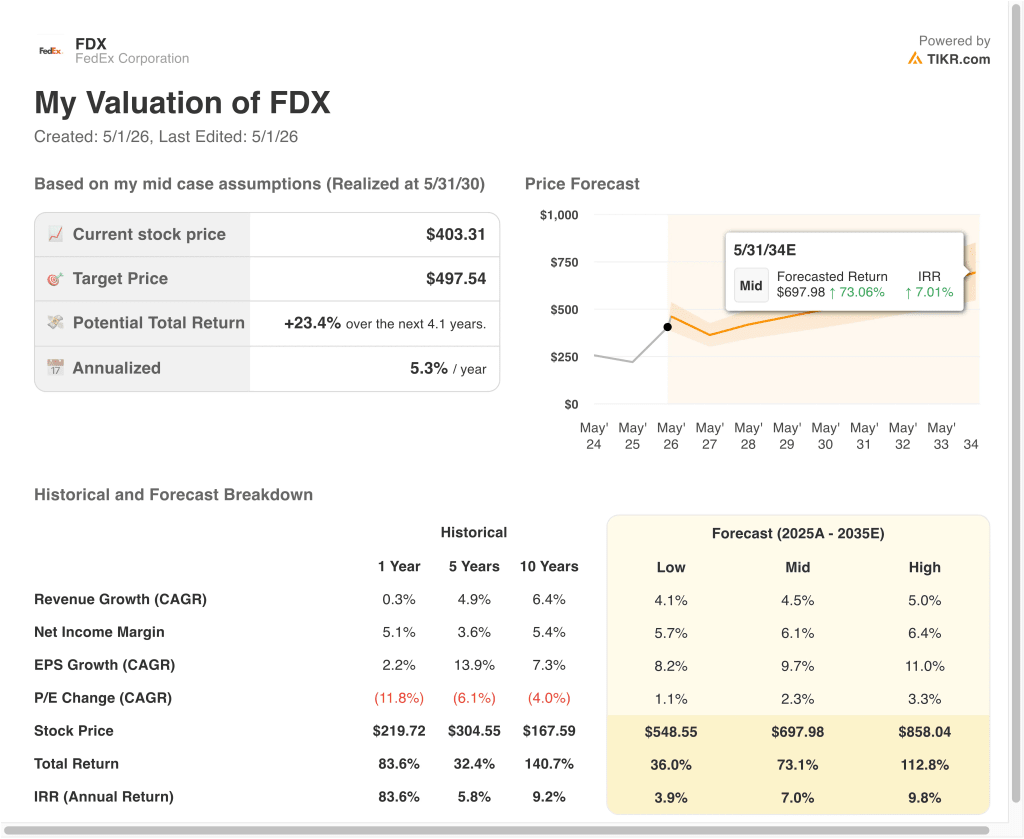

- FDX stock could reach around $425 per share by May 2028, based on our valuation assumptions.

- This implies a total return of 5.4% from today’s price of $403, with an annualized return of around 3% per year over the next 2.1 years.

What Happened?

FedEx Corporation (FDX) reported fiscal Q3 2026 results on March 19, 2026, and beat Wall Street’s expectations by a wide margin. Adjusted EPS came in at $5.25, well above the $4.13 analyst consensus estimate. Revenue reached $24 billion, up 8.1% year over year. And the company raised its full-year fiscal 2026 revenue growth guidance to 6.0% to 6.5%.

CEO Raj Subramaniam said the quarter reflected “disciplined operational execution, the resilience of our global network, and the accelerating impact of our advanced digital solutions.” The DRIVE program is FedEx’s multi-year cost-reduction initiative built on automation and consolidation.

And Network 2.0 is the related effort to combine FedEx Express and Ground operations to reduce overlap and lower costs per package. Together, these programs are now expected to deliver more than $1 billion in permanent structural savings.

FedEx also confirmed the spin-off of FedEx Freight remains on track for June 1, 2026. FedEx Freight handles less-than-truckload, or LTL, shipping, which means consolidating large partial shipments from multiple customers into one truck.

Spinning it off as a standalone public company will let the core delivery business focus on higher-margin e-commerce and international shipping. But the Street consensus price target sits at around $402, essentially in line with today’s stock price of $403.

FDX stock has surged around 96% over the past year and now trades near its 52-week high of $404. Investors are questioning how much of the transformation story is already priced in.

Here’s why FedEx stock could deliver more moderate returns from here as the market weighs a historic earnings acceleration against the stock’s elevated current price.

What the Model Says for FedEx Stock

We analyzed the upside potential for FedEx stock using valuation assumptions based on its DRIVE cost transformation program, Network 2.0 efficiency gains, and improving package yields across U.S. and international markets.

Based on estimates of 5.2% annual revenue growth, 7.7% operating margins, and a normalized P/E multiple of 15.0x, the model projects FedEx stock could rise from $403 to around $425 per share.

That would be a 5.4% total return, or an annualized return of around 3% over the next 2.1 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple and calculates the stock’s expected returns.

Here’s what we used for FDX stock:

1. Revenue Growth: 5.2%

FedEx grew revenue 8.1% year over year in fiscal Q3 2026, reaching $24 billion. But the company’s trailing three-year revenue CAGR, meaning the average yearly growth rate over that period, is slightly negative as growth slowed after the pandemic-era shipping surge. So the 5.2% assumption is more moderate than the most recent quarterly beat suggests.

Management raised full-year fiscal 2026 revenue growth guidance to 6.0% to 6.5%. Analysts project forward two-year revenue growth of around 5.6%. But the Freight spin-off in June 2026 will shift the revenue base. So reported growth rates will look different in future reporting periods.

Based on analysts’ consensus estimates, we used 5.2% annual revenue growth. This reflects sustained demand across FedEx’s core package and international priority services, balanced against post-Freight spin-off mix changes and moderating e-commerce growth trends.

2. Operating Margins: 7.7%

FedEx’s trailing EBIT margin, meaning operating income as a share of revenue, is around 6.8%. And net profit margin sits at around 4.9%. But DRIVE program savings and Network 2.0 consolidation are delivering quarter-by-quarter margin gains through automation, route optimization, and aircraft fleet changes.

Management targets more than $1 billion in permanent structural cost savings. The Federal Express segment adjusted operating margin reached 7.9% in fiscal Q3 2026, up from 7.4% a year earlier. So the transformation is already showing up in the numbers within the core business.

Based on analysts’ consensus estimates, we used 7.7% operating margins. This reflects meaningful improvement from current levels, but also accounts for ongoing wage inflation, fuel cost risks, and the operational complexity of transitioning to a post-Freight spin-off structure.

3. Exit P/E Multiple: 15x

FedEx currently trades at a trailing P/E of around 21.5x. The forward NTM P/E is around 19.2x. But the stock averaged a P/E of around 12.8x over the past 5 years. And the 1-year average sits at around 14.4x. So our assumed exit P/E of 15.0x reflects a modest expansion above recent historical norms.

As DRIVE and Network 2.0 mature, earnings should become more predictable. And more predictable earnings typically support higher P/E multiples over time. But global trade policy uncertainty, fuel price volatility, and the Freight spin-off transition limit how far the multiple can realistically expand.

Based on analysts’ consensus estimates, we use 15.0x as our exit P/E. This represents a slight expansion from the recent historical average, reflecting improved earnings quality from cost transformation, balanced against cyclical risks and the near-term complexity of the Freight separation.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for FDX stock through 2030 show varied outcomes based on DRIVE cost savings, Network 2.0 efficiency gains, and package volume recovery trends (these are estimates, not guaranteed returns):

- Low Case: Cost savings plateau and post-spin-off volume growth disappoints → around 4% annual returns

- Mid Case: Network 2.0 delivers planned savings, and package volumes grow steadily → around 7% annual returns

- High Case: Full DRIVE benefits are realized, and e-commerce demand accelerates → around 10% annual returns

Going forward, FedEx’s transformation story is real, and near-term earnings momentum is strong. But the stock trades near a 52-week high, and Street consensus targets sit essentially in line with today’s price. So the margin of safety looks thin, and the Freight spin-off in June 2026 and Q4 earnings on June 23 are the key milestones to watch.

See what analysts think about FDX stock right now (Free with TIKR) >>>

Should You Invest in FedEx?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FDX, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track FDX alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze FedEx stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!