Key Stats for Amphenol Stock

- Current Price: $147.27

- Target Price (Mid): ~$241

- Street Target: ~$176

- Potential Total Return: ~63%

- Annualized IRR: ~11% / year

- Earnings Reaction: -0.75% (April 30, 2026)

- Max Drawdown: -28.33% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Amphenol (APH) jumped as much as 9.2% the morning after its Q1 2026 earnings report, briefly touching $157, then gave nearly all of it back by the April 30 close at $147.27, down 0.75% on the day. That fade is the real story: the market is not debating whether Amphenol is a great business. It is debated whether a great business is already priced at 30x forward earnings.

Bulls point to the strongest single quarter in the company’s 94-year history. Bears point to $18.7 billion in debt following its largest acquisition ever. The unresolved question is whether Amphenol’s AI interconnect dominance can compound fast enough to justify today’s valuation.

A Quarter That Was Hard to Argue With

On April 29, Amphenol posted Q1 2026 sales of $7.620 billion, beating the $7.094 billion consensus by $526 million, or 7.42%. Adjusted diluted EPS of $1.06 beat by $0.11. Orders reached a record $9.435 billion, up 78% year over year, with a book-to-bill of 1.24:1. Every end market posted a positive book-to-bill, a detail that stands out amid demand uncertainty for most technology companies.

The engine behind the print was IT datacom, representing 41% of total sales. CEO R. Adam Norwitt stated on the earnings call that the segment grew 99% in U.S. dollars and 81% organically year over year, with virtually all of the organic sequential growth driven by AI-related products. That 81% organic figure strips out CommScope’s contribution, confirming that the AI demand wave is hitting Amphenol’s existing product lines, not just newly acquired ones.

Defense added breadth to the story. That segment grew 44% in U.S. dollars and 25% organically, representing 8% of sales. Norwitt described the geopolitical backdrop as a potential “long-term structural shift in demand dynamics.” The Q2 guide calls for high single-digit sequential growth in defense, suggesting the momentum is not a one-quarter event.

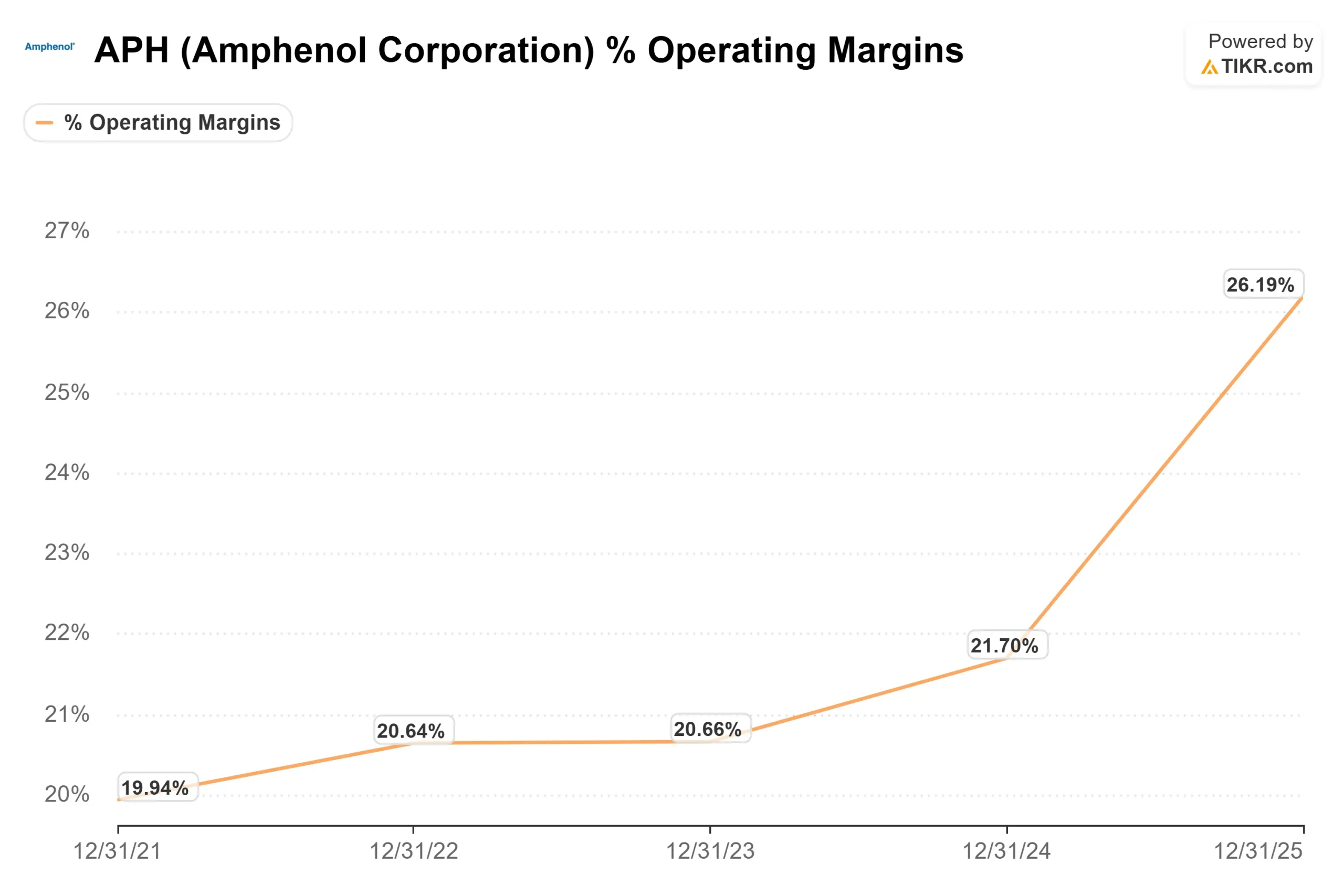

Adjusted operating margin came in at 27.3%, up 380 basis points year over year, despite dilution from the CommScope acquisition. Without that drag, the underlying organic business is running even higher. CFO Craig Lampo confirmed that CommScope is still dilutive but that the gap closes over time, consistent with Amphenol’s historical integration track record.

See historical and forward estimates for Amphenol stock (It’s free!) >>>

The CommScope Bet Is Ahead of Plan

The $10.5 billion acquisition of CommScope’s Connectivity and Cable Solutions (CCS) business closed on January 9, 2026. At the announcement, management projected CCS as roughly a $3.5 to $3.6 billion business growing at mid-teens rates.

Three months in, Norwitt described CCS growing at a pace broadly in line with Amphenol’s own 33% organic growth rate, a meaningful upgrade to the original assumption. Management maintained its 2026 target of approximately $4.1 billion in CCS revenue and $0.15 of adjusted EPS accretion.

Strategically, CCS fills a gap. Amphenol now covers the full data center signal path: high-speed copper, power, active copper, passive fiber, and active optics. Norwitt’s answer to the co-packaged optics question was direct: customers are not choosing between copper and optics, they want more interconnect across both. That framing insulates the revenue thesis from any single architecture outcome.

CCS also opens the building connectivity market across more than 150 countries through specialized distribution channels that Amphenol previously lacked. Norwitt flagged antenna and sensor products as natural cross-sell opportunities. It is early, but it mirrors how prior acquisitions eventually monetized new channels.

The valuation gap between Amphenol and its peers reflects the market’s premium for its AI positioning. At an NTM EV/EBITDA of 17.81x, Amphenol trades above TE Connectivity’s 12.47x but roughly in line with Littelfuse at 18.36x, according to the TIKR Competitors page. That premium holds as long as CommScope integration stays on track and AI capex does not slow materially.

See how Amphenol performs against its peers in TIKR (It’s free!) >>>

The Risk of the Initial Surge Ignored

One disclosure in the Q1 results explains the post-earnings fade. Amphenol booked a $130 million China tax accrual in Q1, layered on top of a $100 million accrual from Q4 2025. Beyond the one-time charges, management raised its adjusted effective tax rate from 24.5% to 27% for the remainder of 2026, a recurring headwind to earnings power flowing through every future quarter.

Combined with $18.7 billion in total debt and 1.6x net leverage, the company’s financial profile is more complex than it was a year ago. None of this is a crisis for a business that generated $1.1 billion in operating cash flow in Q1 alone. But it does explain why a record print produced a flat close on the day.

TIKR Advanced Model Analysis

- Current Price: $147.27

- Target Price (Mid): ~$241

- Potential Total Return: ~63%

- Annualized IRR: ~11% / year

See analysts’ growth forecasts and price targets for Amphenol stock (It’s free!) >>>

The TIKR mid-case model applies a revenue CAGR of around 11% and net income margins expanding to around 20%. The two drivers behind the revenue forecast are IT datacom content gains from AI architecture buildout and communications networks growth through the CCS fiber portfolio. The margin driver is organic operating leverage, which Q1 already demonstrated, even while absorbing CommScope dilution. The primary risk is a deceleration in hyperscaler AI capital spending, which would compress both the growth rate and the multiple.

The high case models around 12% revenue growth and around 21% net income margins, producing a meaningfully higher target. The low case at around 10% growth and around 19% margins still implies upside from today’s price, which explains why 15 of 19 covering analysts rate APH a Buy or Outperform, against a Street mean target of ~$176.

The gap between ~$176 (Street) and ~$241 (TIKR mid) represents the market’s current uncertainty premium on CommScope integration and AI spend durability. Investors who believe both will resolve favorably over the next several years are the buyers at $147.

Conclusion

The metric to watch at the next earnings report, expected around late July 2026, is Q2 IT datacom organic sequential growth against Amphenol’s own low-teens guidance. In Q1, actual organic sequential growth of 16% came in substantially above the guided low-double-digit increase. If Q2 repeats that pattern, it confirms AI infrastructure spending is still accelerating. A miss or a guidance cut on that line is the first signal that today’s valuation premium becomes hard to defend.

Amphenol enters Q2 with record orders, the broadest interconnect portfolio in its industry, and a CommScope integration running ahead of plan. The post-earnings fade is either an opportunity or a warning, depending on how Q2 answers that one question.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Amphenol?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Amphenol, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amphenol alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Amphenol on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!