Key Stats for ExxonMobil Stock

- Current Price: $154.33

- Target Price (Mid): ~$181

- Street Target: ~$166

- Potential Total Return: ~17%

- Annualized IRR: ~4% / year

- Earnings Reaction (Q4 2025, reported 1/30/26): -2.12%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

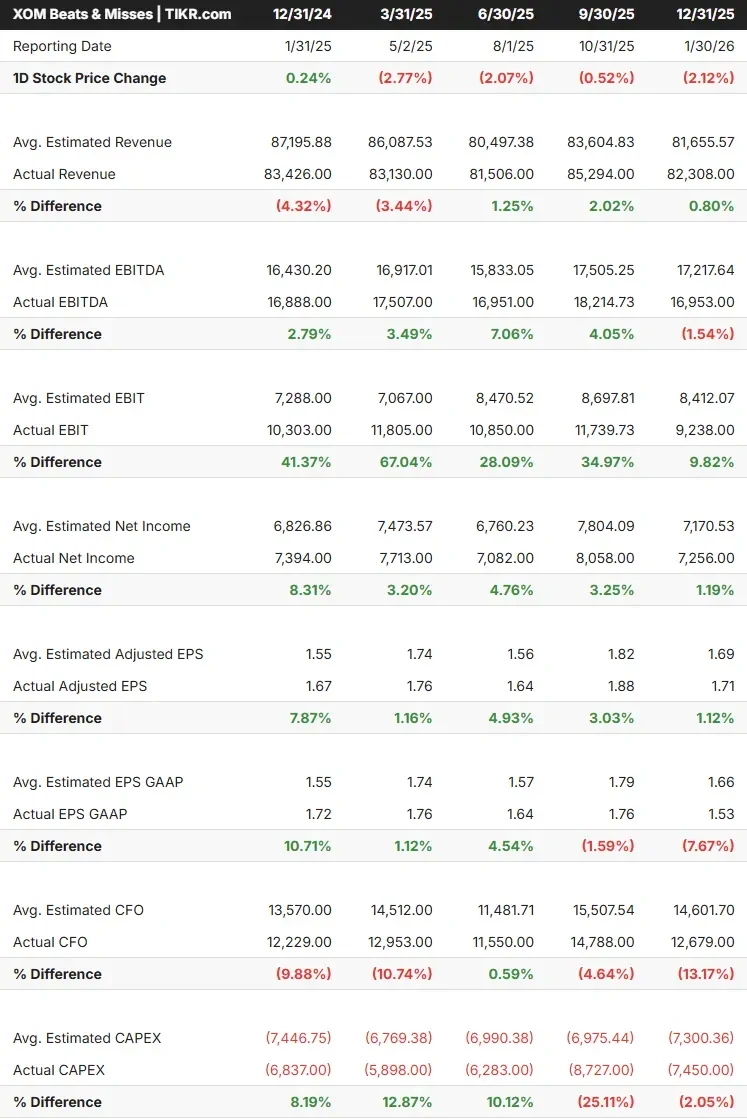

Energy investors came into Friday’s open bracing for an ugly ExxonMobil (XOM) headline. The stock has pulled back roughly 12% from its 52-week high of $176.41 reached in March. Analysts expected earnings per share to fall sharply year over year, almost entirely due to derivative timing losses, accounting effects that reverse in future quarters. The Street’s mean price target of $166.14 sits well above today’s price of $154.33. The debate is whether one-time charges are masking a structurally stronger business, or whether Q1 exposed real cracks in ExxonMobil’s earnings engine.

Why the Headline EPS Misleads This Quarter

ExxonMobil pre-disclosed the Q1 distortions in an SEC 8-K supplement filed in April. Sharp commodity price increases between December 31, 2025, and March 31, 2026, are expected to drive negative timing effects of roughly $4.9 billion to $3.5 billion, primarily in the Energy Products segment. These effects are expected to reverse over time as contracts settle, meaning they depress reported earnings today and flow back in future periods.

The core upstream business told a different story. Per the same 8-K, higher liquids prices are estimated to add $1.9–$2.3 billion to Q1 upstream earnings, and higher gas prices an additional $0.2–$0.6 billion. ExxonMobil stated explicitly that Q1 EPS, excluding these timing effects, was expected to exceed Q4 2025 levels.

The production disruption is real but bounded. The 8-K notes that Q1 global oil-equivalent production was approximately 6% below Q4 2025, with disruptions at Qatar and UAE assets that represent roughly 20% of ExxonMobil’s global production but a smaller share of earnings. Two LNG trains in Qatar affected by missile strikes accounted for around 3% of 2025 upstream production.

See historical and forward estimates for ExxonMobil stock (It’s free!) >>>

The Hormuz Context

The distortions in Q1 trace directly to what the International Energy Agency’s April 2026 Oil Market Report described as the largest oil supply disruption in the history of the global oil market. The conflict disrupted flows through the Strait of Hormuz, through which approximately 20% of global petroleum transits, sending Brent crude from roughly $70 a barrel at the start of the year to above $107 per barrel by late April, per CNN Business.

At the Morgan Stanley Energy and Power Conference 2026 on March 3, Senior Vice President Jack Williams addressed the situation directly: “We have assets all over the world. We have upstream and downstream. We have a big trading operation…I just think we have a few more tools to be able to optimize that.”

ExxonMobil operates one of the largest long-term charter fleets in the industry, which allows it to reroute supply globally when regional disruptions hit. The net result for Q1 is that higher prices helped the upstream side more than disruptions hurt it on a core earnings basis.

What the Structural Plan Actually Says

The Q1 noise does not change the multi-year build. At the Morgan Stanley conference, Williams described the 2030 roadmap in specific terms: “We have this unmatched pipeline of opportunities…manifested in a plan that generates a 13% compound annual growth rate earnings growth over that time period, $25 billion of earnings improvement, $35 billion of operating cash flow improvement. And it’s a plan. It’s not an aspiration, it’s not a target, it’s a plan.”

Three pillars support that claim, all verifiable against TIKR data.

ExxonMobil is targeting 2.5 million barrels per day by 2030 from a plan baseline of 1.2 million. Williams highlighted a 20% recovery uplift from lightweight proppant technology, a material pumped into well fractures to hold them open and increase oil extraction, which was deployed in roughly a quarter of Permian wells in 2025 and is ramping toward half of all new wells in 2026. The Pioneer Natural Resources acquisition added contiguous Midland Basin acreage that amplified the technology advantage, with Pioneer synergies now running at $4 billion annually per Williams.

Williams reported 4 FPSOs (floating production, storage and offloading vessels) producing over 900,000 barrels per day, with 3 more under construction. The recoverable resource estimate has grown from just over 3 billion barrels in 2018 to 11 billion today. The company is also shooting 4D seismic across the full block, which Williams said would help optimize recovery across the entire asset.

ExxonMobil has achieved $15 billion in savings since 2019 against a $20 billion target by 2030. Williams flagged supply chain consolidation alone as expected to contribute $5 billion of the remaining reduction, enabled by pulling previously siloed supply chain operations across the corporation into one central organization.

Williams also confirmed that AI improvements are not currently in the 2030 plan, representing potential upside if seismic analysis and enterprise data applications deliver measurable results within the horizon.

On capital returns: ExxonMobil carries 11% net debt to capital, has grown its annual dividend for 43 consecutive years, and is buying back $20 billion in shares in 2026 on a deliberately steady pace rather than opportunistically.

See how ExxonMobil performs against its peers in TIKR (It’s free!) >>>

Is XOM Undervalued Today?

At $154.33, XOM trades at 7.74x NTM EV/EBITDA, per TIKR. That is a modest premium to Chevron (CVX) at 7.09x, and a more substantial premium to Shell (SHEL) at 4.38x and TotalEnergies (TTE) at 4.74x. The premium over European peers reflects ExxonMobil’s cleaner balance sheet, lower direct Hormuz exposure, and a cost and technology program that Williams argues competitors cannot replicate quickly. Whether the premium holds once the Hormuz risk premium fades is the right question to keep asking.

On free cash flow, the picture has compressed in the near term. LTM levered FCF as of March 31, 2026, per TIKR, was approximately $14.8 billion, down from over $24 billion a year earlier, reflecting the timing effects and Q1 disruptions discussed above. The forward picture is sharply different: TIKR’s NTM levered free cash flow estimate sits at approximately $43 billion, driven by Permian volume growth, Guyana production, and Golden Pass LNG contribution. The gap between trailing and forward FCF is exactly what the Q2 rebound thesis rests on.

The Street’s mean analyst target of $166.14, per TIKR, sits about 7% above today’s price, and the breakdown is 7 Buys, 4 Outperforms, 13 Holds, 1 Underperform, and 1 Sell across 26 analysts. The majority-Hold stance alongside a rising target reflects a Street that sees upside but demands execution confirmation before upgrading.

TIKR Advanced Model Analysis

- Current Price: $154.33

- Target Price (Mid): ~$181

- Potential Total Return: ~17%

- Annualized IRR: ~4% / year

See analysts’ growth forecasts and price targets for ExxonMobil stock (It’s free!) >>>

The TIKR mid-case model targets approximately $181 by December 31, 2030, implying around 17% total return from today’s $154.33 and an annualized IRR of around 4% per year. Revenue growth is assumed at around 1% annually, which reflects ExxonMobil’s profile as a company that grows earnings through production mix improvement and cost discipline, not top-line volume acceleration. The two primary revenue drivers are Permian production growth and Product Solutions margin recovery as the Chemical Products segment normalizes from below-mid-cycle levels. Net income profit margins are forecast to expand from around 9% in 2025 toward around 11% in the mid-case, driven by the structural cost program. The primary downside risk is a rapid resolution to the Hormuz disruption, sending Brent toward $70–$75 per barrel. The 2.7% dividend yield, per TIKR, backed by 43 consecutive years of growth, provides a floor under total return regardless of how oil settles.

Conclusion

Watch Permian production volume when ExxonMobil reports Q2 2026 results, expected in late July or early August. Management guided for roughly 200,000 barrels per day of annual Permian volume growth in 2026. If Q1 production tracked toward the prior-quarter exit rate despite Middle East disruptions, the transformation thesis holds regardless of the headline EPS number. If production disappointed, the premium valuation over peers gets harder to defend. Q1’s headline was messy. The underlying business is not.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in ExxonMobil?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ExxonMobil, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ExxonMobil alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze ExxonMobil on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!