Key Takeaways

- CrowdStrike generated $4.812 billion in fiscal year 2026 revenue at 21.7% year-over-year growth, with a record $330.7 million in net new ARR in Q4 2026, up 47% year over year, bringing total ending ARR to $5.25 billion, according to CrowdStrike’s Q4 FY2026 earnings release.

- Palo Alto Networks generated $9.221 billion in fiscal year 2025 revenue at 14.9% growth and $4.129 billion in free cash flow at a 37.6% FCF margin, while closing its $25 billion CyberArk acquisition in February 2026 and guiding for NGS ARR of $7.94 to $7.96 billion in fiscal Q3 2026.

- CrowdStrike trades at 93.19x NTM P/E and 18.76x NTM EV/Revenues against a peer software median of 4.03x NTM EV/Revenues across its 21-company comparable set on TIKR. Palo Alto trades at 50.24x NTM P/E and 11.27x NTM EV/Revenues.

- TIKR’s Valuation Model assigns CrowdStrike a base-case target of around $1,174, implying a total return of around 159% and an annualized IRR of around 22%. Palo Alto’s base case points to around $320, implying a total return of around 76% and an annualized IRR of around 14%.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Same Sector, Very Different Premiums

Enterprise cybersecurity is one of the few technology categories where budget cuts rarely apply. AI is expanding the enterprise attack surface at a pace that makes security spending non-discretionary for large organizations. Inside that environment, CrowdStrike (CRWD) and Palo Alto Networks (PANW) are competing for the same consolidation dollars. Both have built platform-level architectures. Both are growing above 20% at scale. Both have pulled back sharply from their 2025 highs.

The disagreement is about price. CrowdStrike trades at 93.19x NTM P/E. Palo Alto trades at 50.24x. That is a 43-point spread between two companies whose forward 2-year revenue CAGR estimates differ by roughly 1 point, around 22% for CrowdStrike versus around 21% for Palo Alto, according to TIKR. Whether that spread is justified is what this article answers.

CrowdStrike: One Platform, One Record Year

CrowdStrike’s architecture is its competitive thesis made concrete. A single lightweight sensor feeds a unified cloud data lake. Every module, endpoint detection, next-generation SIEM (security information and event management), identity protection, and cloud workload security, runs on that single agent with no integration required between products. That design makes it low-friction for customers to add modules over time.

The fiscal year 2026 results proved the model is working. According to CrowdStrike’s Q4 FY2026 earnings release, the company surpassed $5 billion in ending ARR for the first time, reaching $5.25 billion at 24% year-over-year growth, driven by a record $1.01 billion in net new ARR for the full fiscal year. The $330.7 million in Q4 net new ARR was the largest single-quarter addition in company history, up 47% year over year. According to the same release, Falcon Flex ARR, the flexible licensing model that lets customers draw down across all 33 platform modules within a single contract, reached $1.69 billion, up over 120% year over year.

George Kurtz, CrowdStrike’s Founder and CEO, stated in the Q4 FY2026 earnings release: “We achieved $5.25 billion in ending ARR–the fastest and only pure-play cybersecurity software company to achieve this milestone–driven by a record $1.01 billion of net new ARR, our first year exceeding $1 billion of net new ARR.” That milestone matters to the investment case because it demonstrates that the Falcon platform’s expansion motion is compounding, not decelerating, following the July 2024 outage.

The TIKR estimates table confirms the financial trajectory:

- Revenue: $4.812 billion in FY2026, 21.7% growth; consensus estimates approximately $5.906 billion for FY2027 at around 23% growth

- Gross margin: 78.00% in FY2026

- Free cash flow: $1.235 billion in FY2026 at a 25.7% FCF margin; consensus projects approximately $1.780 billion in FY2027 and approximately $2.316 billion in FY2028 at around 32% margins

- EBITDA beats vs. consensus across last five quarters: 16.8%, 14.2%, 9.3%, 2.6%, 3.7%

See what analysts think about CrowdStrike stock right now (Free with TIKR) >>>

Palo Alto Networks: Scale, Cash, and a $25 Billion Bet on Identity

Palo Alto Networks built its platform through acquisition rather than architectural purity. Its three platforms, Strata for network security, Prisma for cloud security, and SASE (secure access service edge, meaning cloud-delivered network security), and Cortex for AI-powered security operations, were assembled across roughly 33 deals over the past decade. The platformization strategy pushes enterprises to consolidate onto Palo Alto through bundled contracts that replace multiple point-solution vendors at once.

The results are measurable. Per Nikesh Arora’s commentary on Palo Alto’s Q2 FY2026 earnings call, NGS ARR reached $6.33 billion, growing 33% year over year, with approximately 1,550 total platformized customers up 35%, and a net retention rate of 119% with low single-digit churn among platformized accounts. That retention figure means customers who fully commit consistently spend more over time.

The CyberArk acquisition closed on February 11, 2026, establishing identity security as the fourth pillar of Palo Alto’s platform. Arora explained the rationale directly on the Q2 earnings call: “The emerging wave of AI agents will require us to secure every identity, human, machine, and agent. This is why we moved decisively by announcing our intent to acquire CyberArk last July.” As AI agents take autonomous roles inside enterprise systems, every action is credentialed through an identity. Owning the leading privileged access management platform means Palo Alto can now offer unified coverage across network, cloud, and identity security, a combination no other vendor currently matches at scale.

The TIKR estimates table shows the financial profile of a company that has already reached durable scale:

- Revenue: $9.221 billion in FY2025 at 14.9% growth; consensus projects approximately $11.292 billion in FY2026 at around 22% growth

- Gross margin: 73.5% LTM

- Free cash flow: $4.129 billion in FY2025 at 37.6% FCF margin; consensus projects approximately $5.052 billion in FY2027 at approximately 37% margins

- Non-GAAP operating margin: 30%-plus for three consecutive quarters per Q2 FY2026 earnings call

- EBITDA beats vs. consensus across last five quarters: 4.7%, 3.5%, 4.4%, 2.9%, 3.4%

Estimate a company’s fair value instantly (Free with TIKR) >>>

Growth, Margins, and FCF: Where the Numbers Diverge

CrowdStrike’s 21.7% fiscal year 2026 growth comes against a $4.8 billion base. Palo Alto’s 14.9% comes against a $9.2 billion base, nearly double the size. The forward 2-year revenue CAGR estimates from TIKR put CrowdStrike at around 22% versus Palo Alto at around 21%. A 1-point growth differential does not explain a 43-point NTM P/E gap.

On cash generation, Palo Alto’s $4.129 billion in FCF at 37.6% margins today dwarfs CrowdStrike’s $1.235 billion at 25.7%. Even by fiscal year 2028, TIKR consensus projects CrowdStrike’s FCF margin reaching only around 32%, still below where Palo Alto sits today.

On valuation multiples, the divergence is direct:

- NTM EV/EBITDA: CrowdStrike 63.72x vs. Palo Alto 36.93x

- NTM MC/FCF: CrowdStrike 64.70x vs. Palo Alto 32.38x

- LTM EV/Revenues: CrowdStrike 23.03x vs. Palo Alto 14.47x

- Peer software median NTM EV/Revenue: 4.03x across CrowdStrike’s 21-company comparable set on TIKR

Analyst consensus on TIKR is broadly constructive on both but implies more near-term upside for Palo Alto. CrowdStrike’s mean target of $491.72 across 51 analysts implies around 9% upside from $452.38, with 31 Buys, 11 Outperforms, and 11 Holds. Palo Alto’s mean target of $206.14 across 50 analysts implies around 14% upside from $181.54, with 34 Buys, 11 Outperforms, 10 Holds, and 1 Sell.

One important caveat on Palo Alto’s headline growth: its Q3 FY2026 NGS ARR guidance of $7.94 to $7.96 billion includes approximately $1.47 billion of contribution from the CyberArk and Chronosphere acquisitions, per the Q2 FY2026 earnings call. The organic NGS ARR growth rate runs at a meaningfully lower pace than the 56% headline figure implies.

See analysts’ full growth forecasts and estimates for CRWD and PANW (It’s free) >>>

What the TIKR Valuation Model Says

The TIKR Valuation Model’s base case for CrowdStrike, as of January 31, 2031, produces a target price of around $1,174, implying a total return of approximately 159% from the current $452.38 over approximately 4.7 years, at an annualized IRR of approximately 22%. The mid-case assumes around 20% revenue growth CAGR and around 24% net income margins. The two key drivers are Falcon Flex expansion within the installed base and continued module penetration in identity and SIEM. The primary risk is exit multiple compression: at 93x NTM earnings, the base-case IRR is explicitly sensitive to whether the market continues pricing CrowdStrike as a high-growth platform at the end of the projection window.

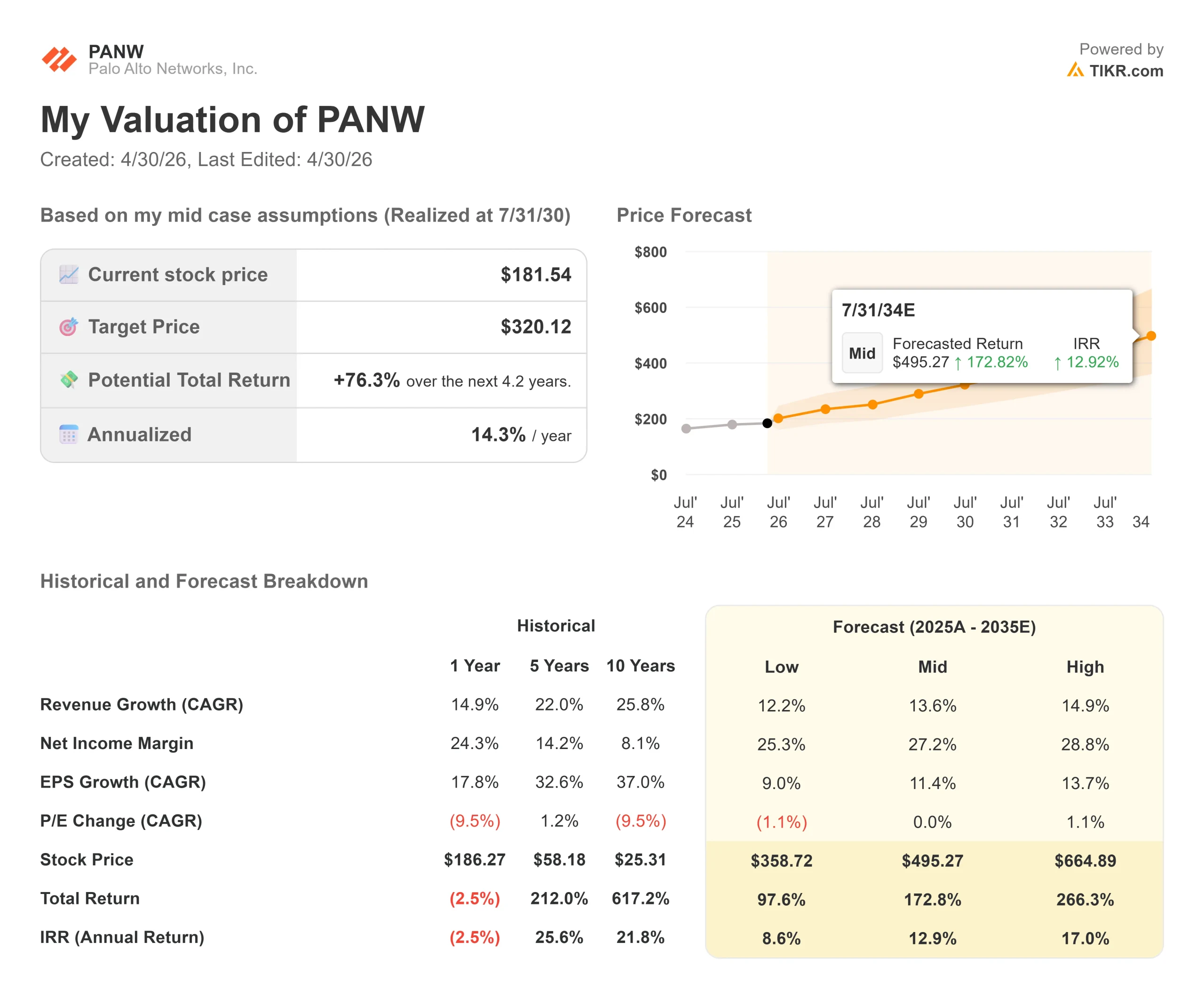

The TIKR Valuation Model’s base case for Palo Alto, as of July 31, 2030, produces a target price of around $320, implying a total return of approximately 76% from $181.54 over approximately 4.2 years, at an annualized IRR of approximately 14%. The mid-case assumes a 14% CAGR in revenue growth and a 27% net income margin, consistent with FCF expansion toward the company’s 40% target by fiscal 2028. The two key drivers are NGS ARR growth through platformization wins, and CyberArk cross-sell across Palo Alto’s 65,000-plus firewall customers. The primary risk is M&A integration: absorbing approximately $28.35 billion in acquisitions within months of each other creates real go-to-market execution risk while the CyberArk and Chronosphere integrations are underway.

Most investors never know if a stock is truly undervalued or overpriced. TIKR’s professional-grade valuation tools give you a clear, data-backed answer across 60,000+ stocks for free →

Which Premium Is Justified?

CrowdStrike suits investors focused on pure-play platform growth who can accept significant valuation multiple risk. The execution record is among the cleanest in large-cap software: five consecutive EBITDA beats, three consecutive quarters of net new ARR acceleration, and a Q1 FY2027 pipeline running 49% above the prior year per CFO Burt Podbere’s March 2026 Morgan Stanley conference commentary. The position requires confidence that mid-20% revenue growth is sustainable and that the NTM P/E of 93.19x does not compress materially before 2031. The TIKR base case implies around 22% annualized IRR under those conditions.

Palo Alto Networks suits investors who prioritize durable free cash flow generation from a platform that already spans network, cloud, and identity security at a relatively lower multiple. Its 37.6% FCF margin today exceeds where CrowdStrike is projected to reach by fiscal year 2028. The CyberArk acquisition carries near-term integration risk, but if the cross-sell ramp into the existing firewall customer base materializes, the identity pillar adds a meaningful growth layer without requiring platform expansion from scratch. The TIKR base case implies around 14% annualized IRR with less sensitivity to multiple compression than CRWD.

Both companies are building toward the same outcome: enterprises running their security stack on one or two consolidated platforms. The difference is how much of that outcome is already priced in at current levels.

Get the most up-to-date financial snapshots of 100K+ stocks with TIKR (It’s free) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!