Key Stats for Meta Stock

- 52-Week Range: $520 to $796

- Current Price: $613

- Street Mean Target: $828

- Street High Target: $1,015

- Analyst Consensus: 48 Buy, 8 Outperform, 7 Hold, 0 Sells

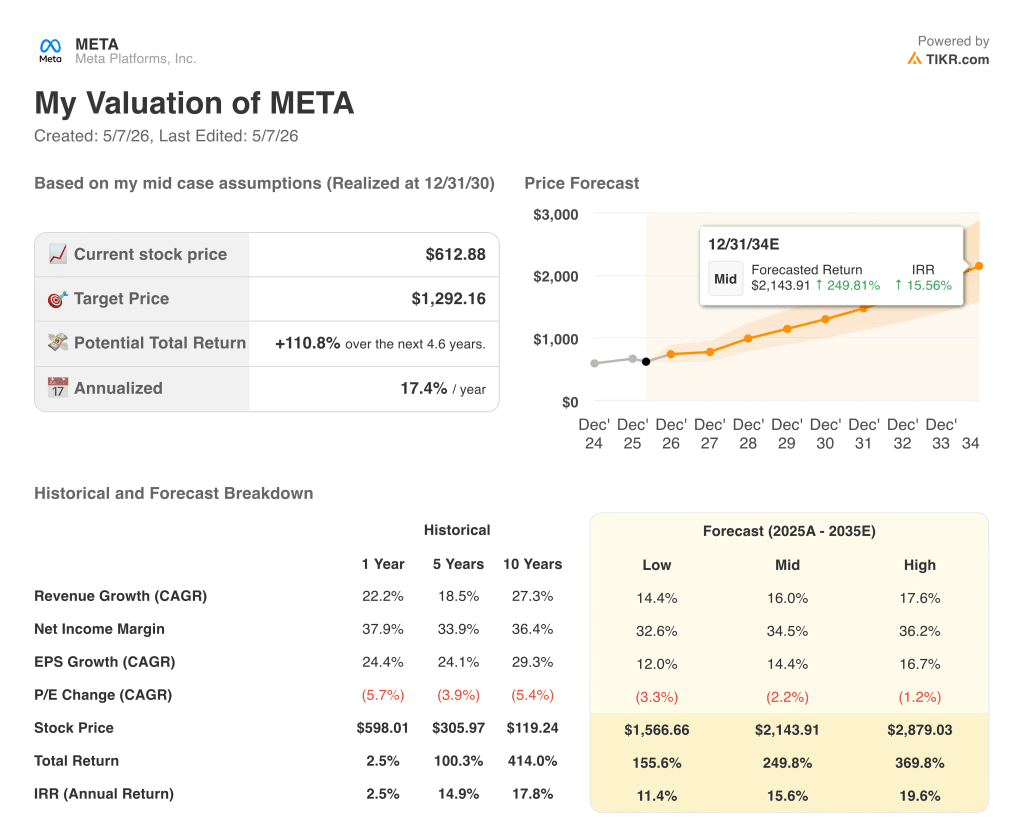

- TIKR Model Target (Dec. 2030): $1,292

What Happened to Meta Stock After Q1 2026 Earnings

Meta Platforms (META) delivered what should have been a clean quarter.

Revenue of $56.31 billion beat estimates by roughly $755 million, growing 33% year-over-year — the fastest quarterly growth rate the company has posted since 2021.

Adjusted EPS of $7.31 cleared the Street by 7.2%.

The ad business ran hot: ad impressions across the Family of Apps grew 19%, average price per ad rose 12%, and operating margin held at 40.6%.

The stock fell anyway, dropping as much as 10% after hours.

The reason was one line in the outlook section: Meta raised its 2026 capex forecast to $125B–$145B, up from $115B–$135B, citing higher component pricing and additional data center costs.

That $10 billion step-up in the guidance range landed harder than the beat did.

The Q1 bottom line was also partially inflated by an $8.03 billion one-time tax benefit tied to the One Big Beautiful Bill Act. Strip that out, and net income was $18.7 billion rather than the reported $26.8 billion.

On a normalized basis, Meta stock is running at $7.31 in adjusted EPS — solid, but not the 62% headline growth the GAAP figure implies.

What is not in dispute is the advertising business’s resilience.

The value optimization suite now runs at an annualized revenue run rate above $20 billion, more than doubling year-over-year.

Partnerships ads, driven by creator-brand collaborations, crossed a $10 billion revenue run rate, also more than doubling year-over-year.

Reels time spent on Instagram rose 10% after ranking improvements made in Q1, and Facebook video watch time in the U.S. and Canada grew 9% in the quarter alone.

The Muse Spark model release from Meta Superintelligence Labs was the other centerpiece of the quarter, with Zuckerberg describing it as the first step on a scaling ladder toward more advanced models already in training.

Meta AI sessions per user rose by double-digit percentages following the rollout, and Business AIs on WhatsApp and Messenger grew from 1 million weekly conversations at the start of the year to over 10 million.

These are engagement metrics, not revenue metrics — agentic product monetization remains a future-year story — but the trajectory is moving in the right direction.

Headcount ended Q1 at 77,986, down 1% sequentially, with management confirming a roughly 10% reduction-in-force in May targeting approximately 8,000 employees.

Total expense guidance for the full year held steady at $162B–$169B, meaning management believes the headcount savings roughly offset the capex overage.

DAP declined slightly from Q4, attributed to internet disruptions in Iran and WhatsApp access restrictions in Russia. Absent those two factors, CFO Susan Li noted that DAP growth would have been positive quarter-over-quarter.

The bear case on Meta stock is a timing argument: the company is suppressing free cash flow through at least 2026 while the payoff from agentic products remains uncertain, and the stock has already retreated 23% from its 52-week high of $796.

The bull case is that the core advertising business is growing at 33% with 41% operating margins, and $613 is buying that compounding machine at roughly 26% below Wall Street’s mean price target of $828 before any AI optionality is priced in.

Meta Stock Financials: What the Income Statement Shows

The income statement tells a resilience story under infrastructure cost pressure.

Gross margin was 81.9% in Q1 2026, essentially flat against the 82.1% posted in Q1 2025, and stable across the trailing eight quarters despite significant increases in infrastructure spending. That stability reflects how efficiently Meta monetizes digital inventory with near-zero marginal cost per ad impression.

Operating income was $22.87 billion, up 30.3% year-over-year, producing a 40.6% operating margin. That compares to 41.5% in Q1 2025, meaning Meta absorbed a year of heavy AI investment with less than 90 basis points of margin compression.

Total operating expenses rose 35% year-over-year to $33.44 billion, driven by infrastructure costs (depreciation, data center operating spend, cloud) and AI technical hiring. The growth rate in expenses outpacing revenue growth by two points is what the market is watching.

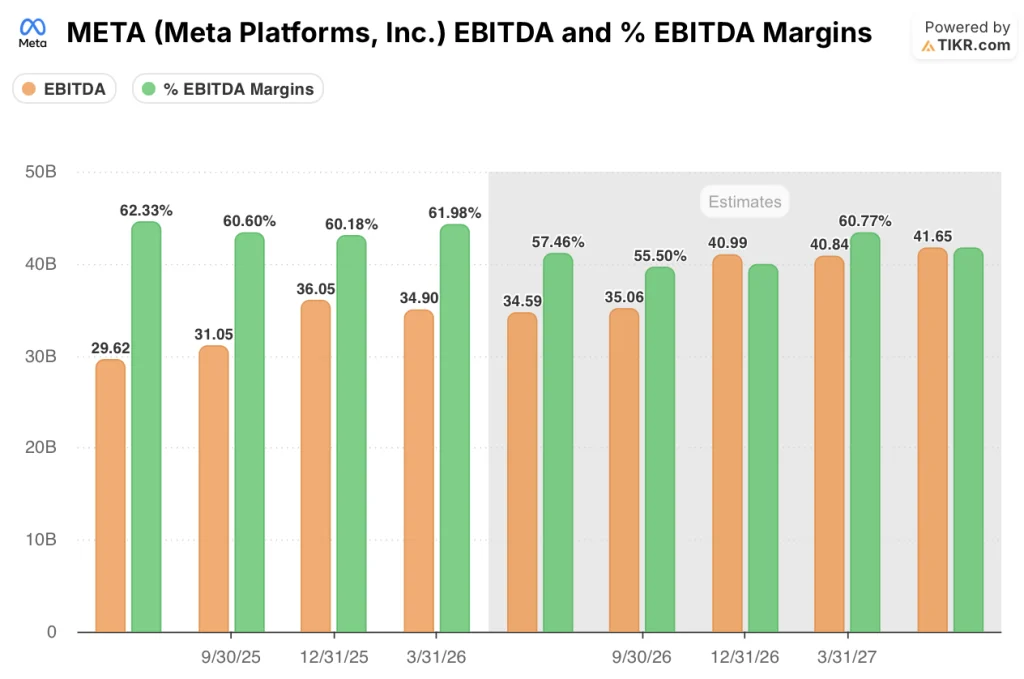

EBITDA came in at $34.9 billion, up 36.3% year-over-year, with EBITDA margins at 61.98% — 575 basis points above Street estimates. That margin beat is the single cleanest signal of operating leverage in an otherwise heavy-spend quarter.

What Does the Valuation Model Say?

TIKR’s valuation model puts Meta stock’s mid-case price target at $1,292.16, implying roughly 111% upside from the current price of $612.88.

The model assumes a 16% revenue CAGR through 2035, with net income margins holding around 34.5%.

Those are not aggressive assumptions — Meta has grown revenue at an 18.5% CAGR over the past five years and has historically run net income margins around 33.9%.

In the low case, the model reaches $1,566.66 by 2035, implying a 155.6% total return at an 11.4% annualized rate.

The mid case reaches $2,143.91, implying a 249.8% total return at near 16% annually.

The high case reaches $2,879.03, implying a 369.8% total return at ~20% annually.

All three scenarios are realized at December 2034, and all three are built on a business that is already generating $56 billion in quarterly revenue with 41% operating margins.

The risk to the model is timing: Meta is spending $125–$145 billion in capex this year alone, which means free cash flow is expected to run negative through most of 2026 before recovering in 2027.

The Q1 report does not change the long-term model, but it does make the near-term path harder to defend — investors are being asked to look through a heavy spending cycle on the promise that the AI infrastructure pays off.

At $612.88, the stock is trading at roughly 26% below Wall Street’s mean price target of $828, which does not yet price in the upside from agentic products, Meta AI at scale, or the glasses business.

Should You Invest in Meta Platforms, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Meta Platforms stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Meta Platforms stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze META stock on TIKR for Free →