Key Stats for PepsiCo Stock

- 52-Week Range: $128 to $171

- Current Price: $155

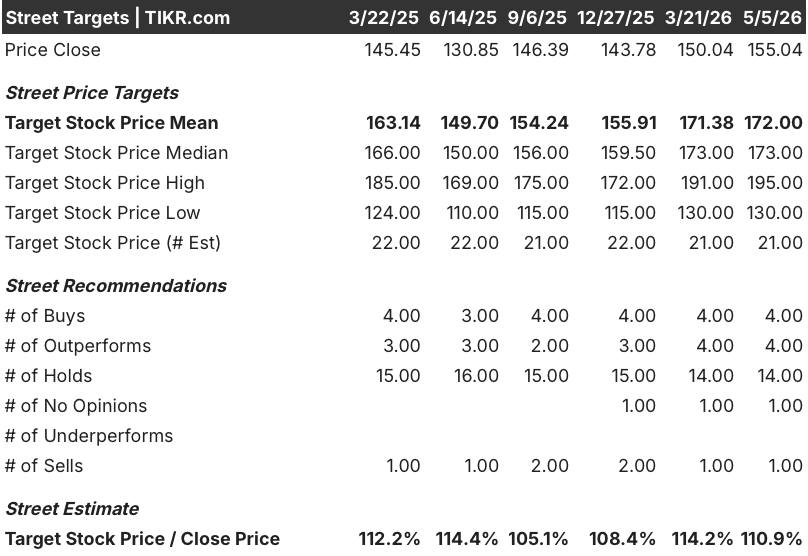

- Street Mean Target: $172

- Street High Target: $195

- Analyst Consensus: 4 Buys / 4 Outperforms / 14 Holds / 1 No Opinion / 1 Sell

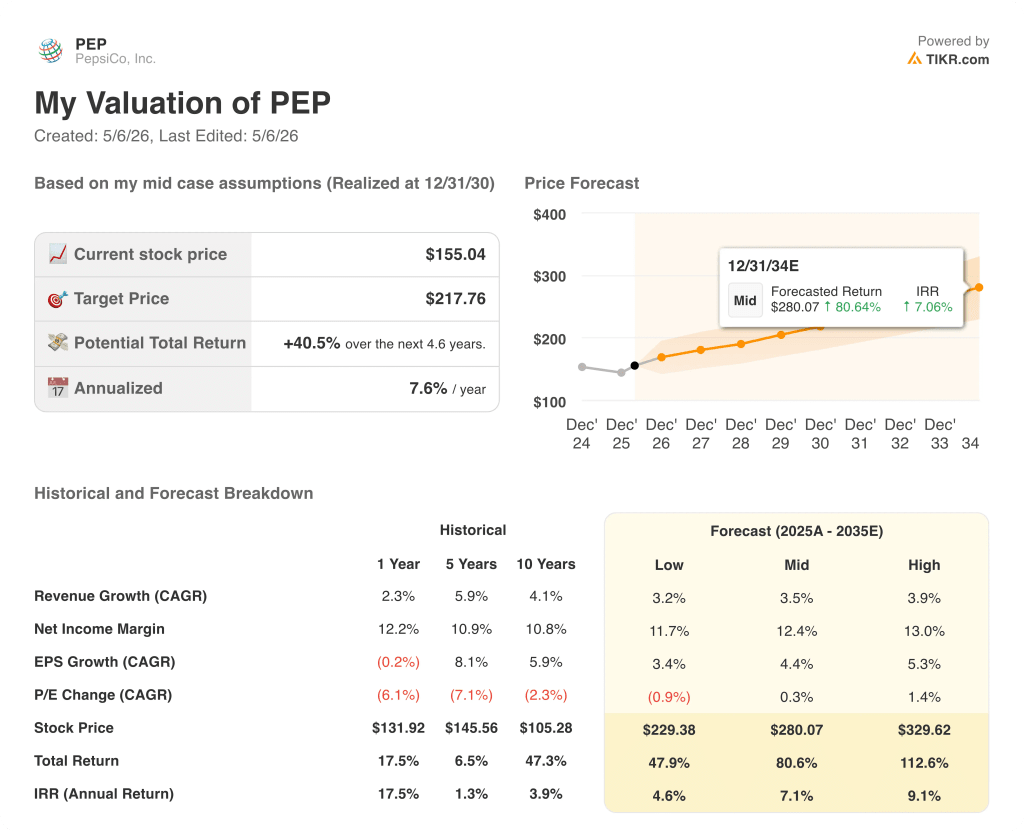

- TIKR Model Target (Dec. 2030): $218

What Happened?

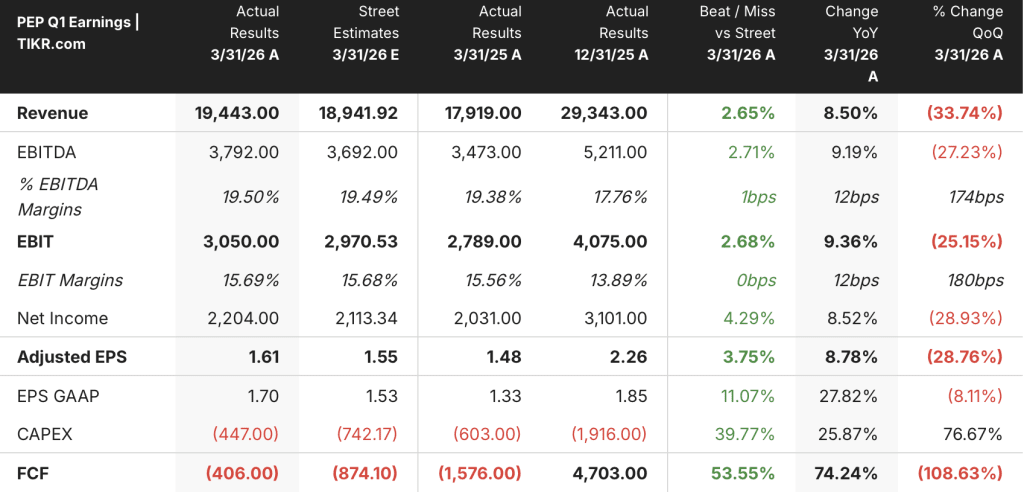

PepsiCo (PEP), the world’s largest convenient food and beverage company by revenue, reported first-quarter results on April 16 that beat Wall Street estimates on both the top and bottom lines.

Net revenue rose 8.5% to $19.44 billion, topping the $18.94 billion consensus, with 2.6% organic revenue growth driven by effective net pricing and a modest contribution from volume.

The number that mattered most was volume: North America Foods finally turned positive, growing 2% after a 1% decline in the fourth quarter, as price cuts of up to 15% on Lay’s and Doritos drove the first meaningful demand recovery in years.

CEO Ramon Laguarta said the company added 300 million new consumption occasions in North America Foods during the quarter compared with the same period a year ago, framing the result as confirmation that the affordability strategy is working.

Adjusted EPS came in at $1.61, ahead of the $1.55 estimate, and PepsiCo stock rose roughly 3% on the day before settling back near $155 as investors weighed the beat against lingering cost uncertainty from the Iran war.

CFO Steve Schmitt flagged that the company’s 6-to-12-month commodity hedges provide near-term cost protection, but acknowledged that inflation from rising energy and packaging costs is likely to land at some point in 2026.

Management reaffirmed full-year guidance for 2% to 4% organic revenue growth and 4% to 6% core constant currency EPS growth, a signal that leadership believes the Q1 momentum is sustainable and not a one-quarter anomaly.

Wall Street’s Take on PEP Stock

The Q1 beat closes the loop on the first leg of the turnaround argument: price cuts work, volumes are moving, and management has the discipline to hold guidance in a geopolitically uncertain environment.

PEP’s normalized EPS of $1.61 in Q1 grew 8.8% year-over-year, and consensus now projects that figure reaching around $2.23 in Q2 and around $2.44 in Q3 as the volume recovery compounds through the peak summer season with the FIFA World Cup providing additional brand activation at scale.

Of 24 analysts covering PEP stock, 4 rate it a Buy, 4 an Outperform, 14 a Hold, and 1 a Sell, with a mean price target of $172, implying roughly 11% upside from current levels; the split reflects a Street that acknowledges the progress but wants to see the turnaround hold across multiple quarters before raising conviction.

The bull and bear price targets span $130 to $195, a $65 range anchored on opposite reads of the same variable: whether the affordability-driven volume recovery can absorb the cost inflation arriving later in the year without management reverting to price hikes that would restart the volume erosion cycle.

Priced at roughly 18x forward earnings against a 5-year historical average closer to 21x, PepsiCo stock appears undervalued given that EPS is now growing again and management has reaffirmed guidance for a second consecutive quarter.

If packaging and energy costs spike beyond hedge coverage before productivity savings can offset them, management faces the lose-lose of margin compression or volume-killing price hikes.

The specific number to watch in Q2 is North America Foods organic revenue growth: if it clears 3%, the summer volume thesis is confirmed and Hold-rated analysts have a clear reason to upgrade.

What Does the Valuation Model Say?

TIKR’s mid-case model puts PEP’s fair value at around $218, anchored to roughly 4% revenue CAGR and a net income margin of around 12% through 2030, assumptions management made more credible by delivering ~9% revenue growth and double-digit operating profit expansion in a single quarter while holding full-year guidance under geopolitical pressure.

With forward earnings trading at roughly 18x against a five-year average of 21x, and EPS growth re-accelerating above 8% year-over-year on the back of a confirmed volume inflection and a productivity program delivering record savings, PepsiCo stock is undervalued by the gap between where the multiple sits today and the premium this business has historically earned at comparable growth rates.

The entire bull case hinges on one variable: whether the volume recovery in North America Foods can survive the cost cycle arriving later in 2026 without triggering a pricing reversal that restarts the brand erosion the company spent the last year unwinding.

What Has to Go Right

- North America Foods volumes must continue improving sequentially through Q2 and Q3, building on the 2% gain and 300 million incremental consumption occasions added in Q1

- The Gatorade restage targeting everyday hydration occasions, including new low-sugar formulas launching later this year, needs to expand the brand’s addressable market beyond the sports-use-case that has capped its growth for years

- FIFA World Cup activation across global markets, where Lay’s “No Lay’s, No Game” is deploying with personalized digital campaigns, must convert brand exposure into measurable household penetration gains in markets where per-capita consumption is low

- The Google Cloud AI partnership focused on supply chain and go-to-market execution must accelerate the productivity savings pipeline that CFO Schmitt described as the primary funding mechanism for reinvestment, targeting more than 90% free cash flow conversion by 2027

- PBNA’s 9% total revenue growth, driven by CELSIUS energy drink distribution and the poppi acquisition, must continue diversifying the beverage portfolio away from a CSD segment where volumes remain under pressure

What Could Go Wrong

- The 6-to-12-month commodity hedges expire mid-year, and if Iran war-driven energy and packaging inflation exceeds what productivity savings can offset, management faces a binary choice between margin compression and volume-killing price hikes

- Fourteen Hold ratings on PepsiCo stock reflect a Street that has seen management promise a North America Foods recovery before: any miss on Q2 organic revenue growth reopens the bear case and delays the multiple rerating

- SNAP benefit restrictions began rolling out across 8 states in Q1, covering beverages and candy, and the downstream demand impact on middle-income and lower-income shoppers — exactly the consumers the price cuts were designed to win back — remains unquantified and may not show up fully until Q3

Should You Invest in PepsiCo, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PepsiCo stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PepsiCo alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PEP stock on TIKR for Free →