Key Takeaways:

- Datadog is a cloud-based monitoring and analytics platform for modern IT environments, and has consistently beaten earnings estimates while growing its AI observability capabilities.

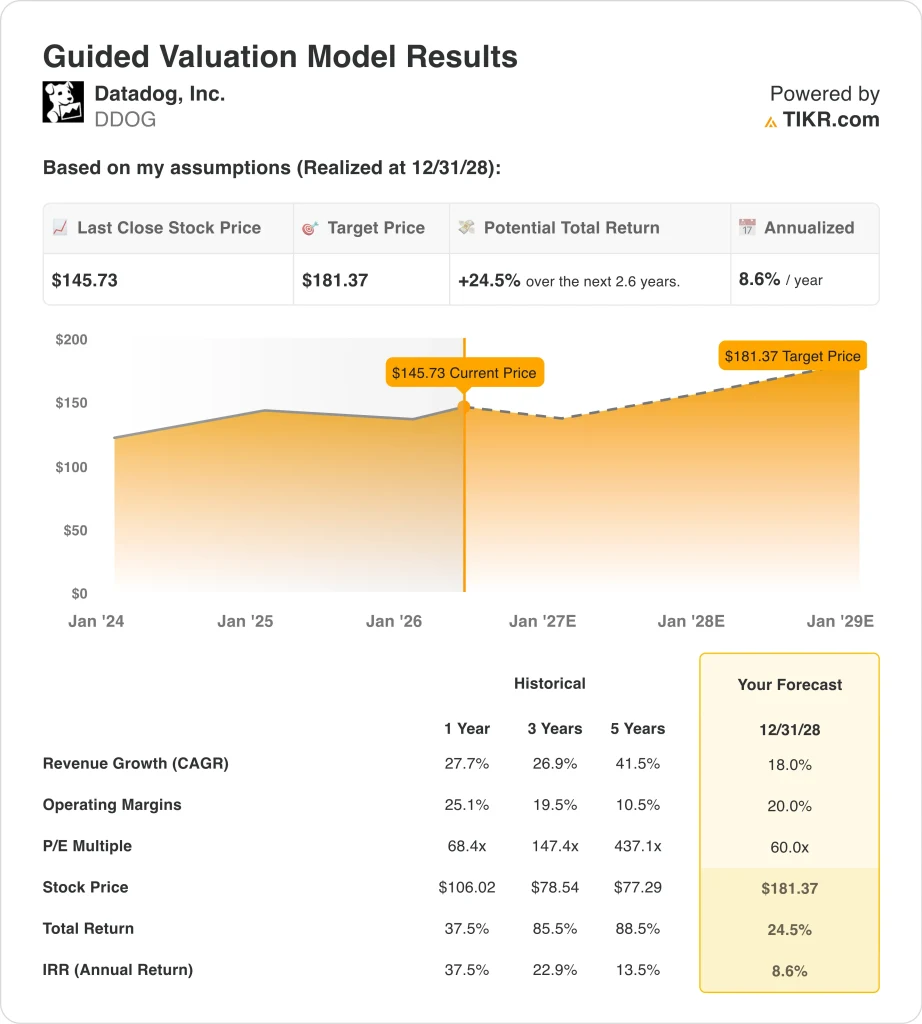

- DDOG stock trades near $146, up around 37% since late January 2026, with a street consensus target near $177.

- DDOG stock could rise from $146 to around $181 per share by December 2028, based on 18% annual revenue growth, 20% operating margins, and a 60x P/E multiple.

- That would be a 24.5% total return, or around 8.6% annualized over the next 2.6 years.

What Happened?

Datadog, Inc. (DDOG) provides a cloud-based monitoring and analytics platform that helps companies observe, track, and secure their software infrastructure in real time. The platform covers infrastructure monitoring, application performance management (APM), log management, security, and AI observability, all in one integrated system.

DevOps teams, which combine software development and operations functions, use Datadog to monitor workloads running on major cloud providers like AWS, Google Cloud, and Microsoft Azure. In April 2026, shareholders approved the company’s redomiciliation from Delaware to Nevada.

Datadog’s earnings history reflects consistent execution. Q4 2025 adjusted EPS of $0.59 beat the $0.55 estimate. Q3 2025 adjusted EPS of $0.55 also beat the $0.46 estimate. And Q2 2025 adjusted EPS of $0.46 exceeded the $0.42 estimate.

This track record shows strong demand for cloud observability tools, particularly as AI workloads create new monitoring complexity. Datadog published a report finding that 5% of AI model requests fail due to capacity limits, highlighting the acute need for AI-focused monitoring tools. So the product is solving a real and growing customer problem.

The company announced its DASH 2026 user conference for June 9 and 10 in New York City, a major platform for showcasing new capabilities and AI features. Q1 2026 earnings are scheduled for May 7, the day after this article is published, and the consistent beat-and-raise track record suggests the upcoming report could deliver another positive surprise.

Chainguard also announced a partnership with Datadog to strengthen container security and observability, adding to the platform’s growing security coverage. So product expansion and partnerships continue alongside strong core momentum.

Some investor caution emerged after IBM and ServiceNow results in late April raised questions about AI disruption for traditional software. But Datadog’s infrastructure monitoring focus makes it less susceptible to direct AI replacement than application-layer software firms.

Here’s why Datadog stock could continue to deliver above-average returns as the AI infrastructure buildout drives cloud monitoring demand higher.

What the Model Says for DDOG Stock

We analyzed the upside potential for Datadog stock based on its expanding AI observability platform, strong recurring revenue from multi-product adoption, and growing enterprise demand for unified cloud monitoring as AI infrastructure spending accelerates.

Based on estimates of 18% annual revenue growth, 20% operating margins, and a normalized P/E multiple of 60x, the model projects Datadog stock could rise from $146 to around $181 per share.

That would be a 24.5% total return, or an 8.6% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for DDOG stock:

1. Revenue Growth: 18%

Datadog’s 1-year revenue growth of 27.7% and 3-year CAGR of 26.9% reflect a strong market position in a growing space. The forward two-year revenue CAGR sits near 19.9% by analyst consensus. Based on analysts’ consensus estimates, we used 18% revenue growth, slightly below consensus to reflect natural deceleration as the company scales to a larger revenue base.

The AI infrastructure buildout is a direct and durable tailwind for Datadog. As companies deploy large language models and AI agents, they need sophisticated tools to monitor performance, cost, and failure rates. Datadog’s own research showing 5% of AI model requests fail due to capacity limits illustrates the specific pain point its platform addresses. So AI adoption should sustain above-trend revenue growth beyond the near-term comparison period.

The 5-year revenue CAGR of 41.5% shows exceptional historical growth, and the 18% forward assumption implies meaningful deceleration. But at Datadog’s current scale, maintaining 18% growth on a larger base still represents strong execution. And the multi-product platform strategy deepens customer relationships and increases average revenue per account over time.

2. Operating Margins: 20%

Datadog’s LTM GAAP operating margin is negative 1.2% because stock-based compensation and amortization reduce reported income significantly. But the company’s gross margin of 80% is best-in-class for software and provides significant operating leverage as the business scales. Based on analysts’ consensus estimates, we used 20% adjusted operating margins, reflecting the company’s path toward consistent profitability as revenue growth outpaces expense growth.

The 3-year historical adjusted operating margin of around 19.5% shows that Datadog has already operated near this level. And the 80% gross margin provides a strong foundation for long-term margin expansion as sales and marketing costs moderate as a percentage of revenue. So the 20% assumption reflects the company’s current trajectory rather than a stretch target.

The forward EBITDA CAGR of 21.5% by analyst consensus implies margins are already expected to reach and sustain the 20% level. And as operating leverage builds, Datadog could exceed this assumption if revenue growth remains above 15% through the forecast period. So the 20% margin is a reasonable and grounded baseline.

3. Exit P/E Multiple: 60x

Datadog trades at a next twelve-month P/E of 67x, and high-growth software companies with 80%+ gross margins have historically commanded premium multiples of 40x to 80x forward earnings. The 60x exit assumption reflects modest compression from today’s 67x NTM multiple as the company matures slightly. Based on analysts’ consensus estimates, we used a 60x exit P/E multiple, reflecting Datadog’s durable competitive position while acknowledging that growth-related premiums tend to compress over time.

A 60x P/E is high by absolute standards, but it is appropriate for a business growing revenue at 18% with 80% gross margins and a consistent earnings beat track record. Competitors like Dynatrace trade at lower multiples, but Datadog’s scale and multi-product platform justify the premium. So the 60x assumption reflects both current market sentiment and Datadog’s structural competitive advantages.

Investors should note that a 60x multiple leaves the stock vulnerable to derating if revenue growth slows materially below 15%. The stock’s 52-week range of $98 to $202 reflects the significant volatility investors must tolerate. But the consistent beat-and-raise earnings history provides confidence that the premium multiple is earned.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

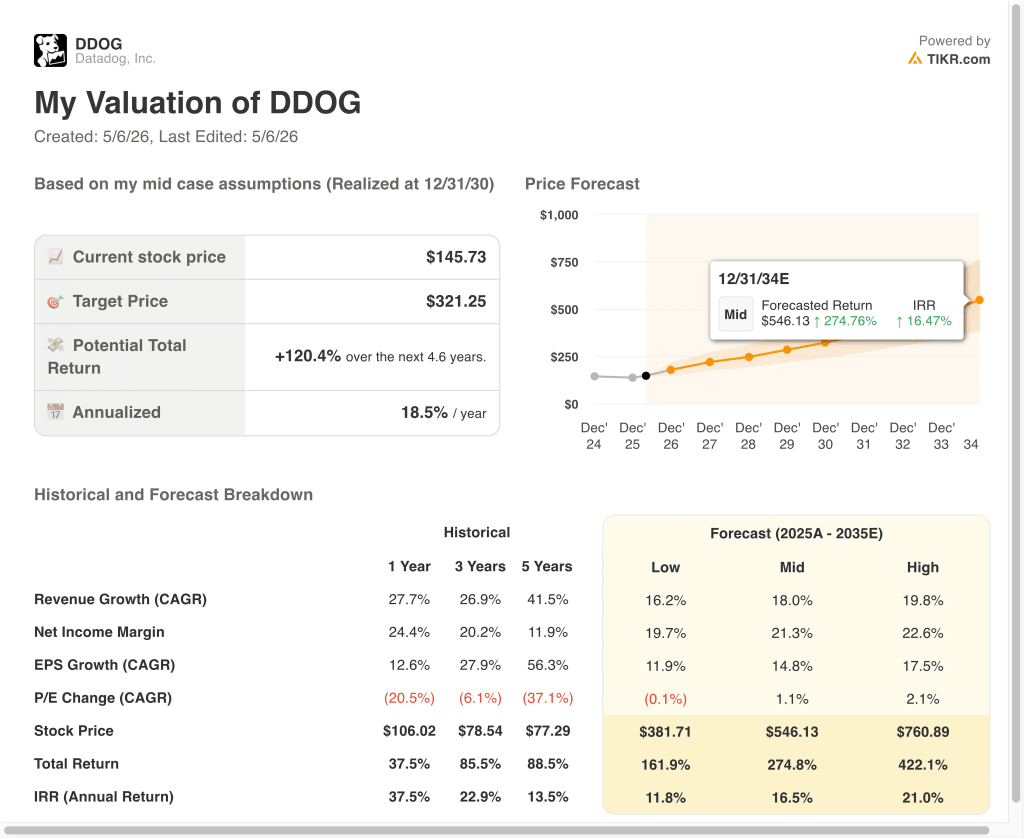

Different scenarios for DDOG stock through 2030 show varied outcomes based on AI observability adoption rates and multi-product platform expansion (these are estimates, not guaranteed returns):

- Low Case: Revenue growth decelerates faster than expected, and the multiple compresses toward industry averages → 11.8% annual returns

- Mid Case: AI tailwinds sustain growth near 18% and adjusted margins expand toward 20% as planned → 16.5% annual returns

- High Case: AI observability becomes a standard enterprise requirement, and revenue growth reaccelerates above 20% → 21% annual returns

Going forward, Datadog’s stock will be closely tied to the company’s ability to monetize the AI infrastructure buildout and sustain its track record of earnings beats. The Q1 2026 earnings report on May 7 is the most immediate catalyst, and investors will watch for any acceleration in customer spending related to AI monitoring and observability deployments.

Even in the low case, the model projects annual returns near 11.8%, which is above the 10% threshold many investors target, making DDOG an interesting setup for investors comfortable with high-multiple growth stocks.

See what analysts think about DDOG stock right now (Free with TIKR) >>>

Should You Invest in Datadog?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DDOG, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DDOG alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Datadog stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!