Key Stats for AXON Stock

- 52-Week Range: $339.01 to $885.92

- Current Price: $393.75

- Street Mean Target: ~$702

- TIKR Model Target (Mid): ~$1,201

- Earnings Date: May 6, 2026

Value your favorite stocks like AXON with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

How a $886 Stock Became a $394 Stock Without the Business Changing Much

Axon (AXON) makes the Taser, which most people know, but the Taser has become almost secondary to what the company actually is today. The real business is a deeply integrated public safety platform that combines hardware, cloud software, and increasingly AI, covering everything from body cameras and in-car video to digital evidence management, real-time situational awareness through its Fusus acquisition, and Draft One, an AI tool that automatically generates police report drafts from body camera footage.

Every piece of hardware Axon sells is essentially a subscription onramp, and that software ecosystem is what makes the business genuinely difficult to displace once a department adopts it.

The stock’s decline from its highs has less to do with the business and more to do with the multiple. Axon was trading at a premium that assumed flawless execution and continued margin expansion, and when the Q3 2025 EPS print came in below estimates for the first time in several quarters, the stock dropped sharply. What followed was a broader de-rating of high-multiple growth names, and Axon got caught in that current alongside many others.

The underlying results have remained strong throughout the pullback, which is the part of this story worth paying attention to.

See analysts’ growth forecasts and price targets for AXON (It’s free) >>>

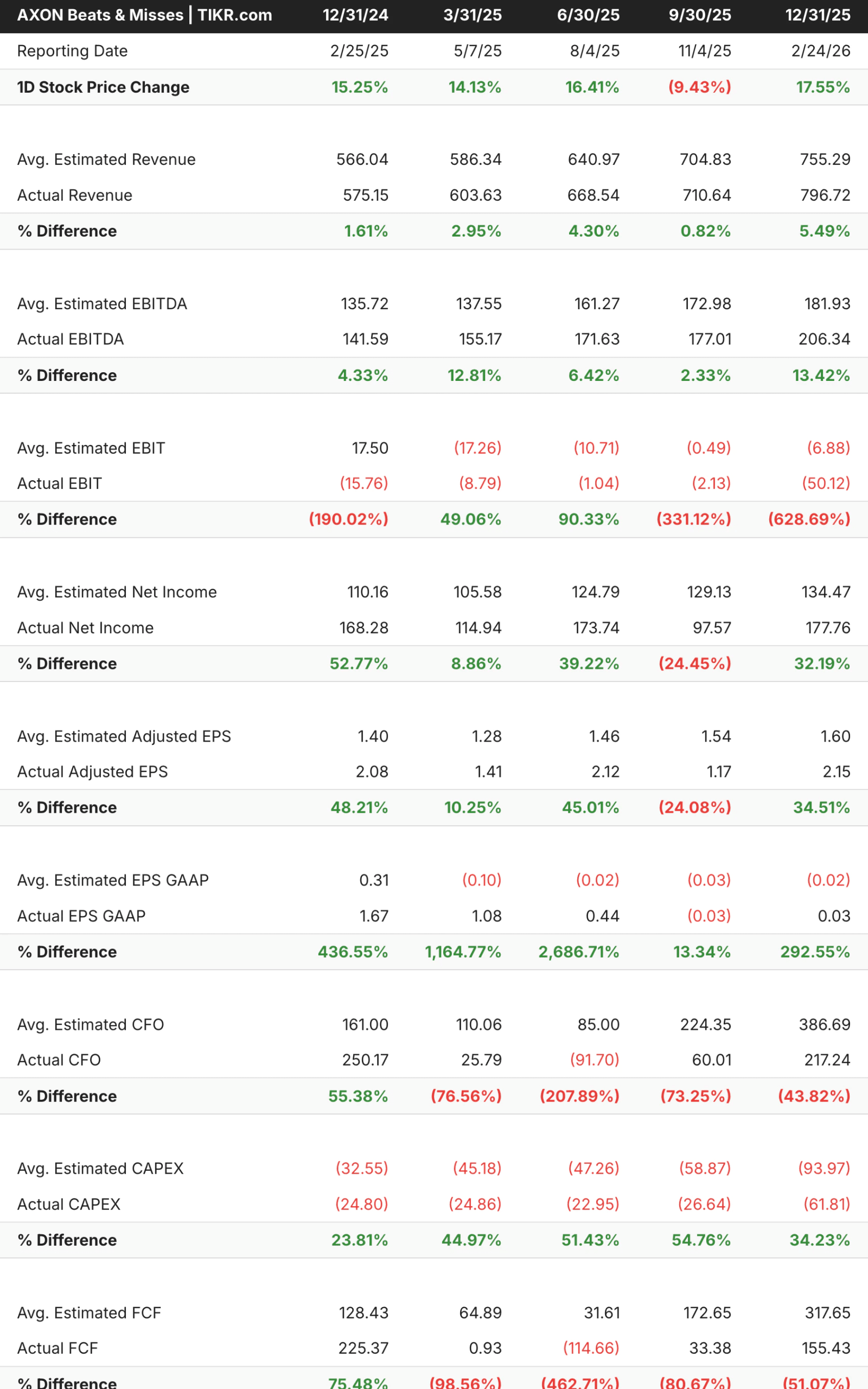

What Five Quarters of Beats Tell You About Tomorrow’s Print

Looking at the last five quarters together, Axon has beaten revenue estimates in every single one, and the beats have been getting larger, going from around 2% in early 2025 to nearly 5.5% in Q4. EBITDA has been similarly consistent, with beats ranging from around 4% to 13%.

The one blemish is Q3 adjusted EPS, which missed by about 24% and was the catalyst for that quarter’s selloff, but the subsequent Q4 print of $2.15 against a $1.60 estimate went a long way toward restoring confidence in the earnings trajectory.

Heading into tomorrow, analysts are looking for revenue of around $780 million, up around 29% year over year, with adjusted EPS of around $1.66. Given the track record, the base case is that Axon beats both numbers, which is exactly what a stock sitting this far below its highs would need to start recovering.

Axon Stock Financials: The Operating Margin Story Deserves Attention

Revenue has grown from $863 million in 2021 to $2.78 billion in 2025, reflecting both the underlying strength of the public safety market and Axon’s ability to expand within it. Gross margins have been remarkably stable throughout that period, holding around 60%, indicating that the platform’s pricing power and competitive position have not eroded despite rapid growth.

The operating margin line is where investors have been more cautious. After improving from deeply negative in 2021 to around 3% in 2024, operating margins dipped slightly to around negative 1% in 2025, reflecting heavy investment in R&D, the Fusus integration, and international expansion.

This is not a sign of structural deterioration so much as a business that is deliberately investing ahead of its revenue curve, which is what you would expect from a company guiding toward $3.1 billion in 2026 revenue and well beyond that in subsequent years.

The forward two-year revenue CAGR consensus sits around 30%, and the forward two-year EBITDA CAGR around 33%, both of which would require the operating leverage to start showing up in the back half of 2026.

Motorola Solutions is the most direct comparable and trades at a premium multiple, which gives you a sense of how the market values durable public safety platforms with recurring revenue. Axon’s software mix and AI integration give it a growth profile that Motorola cannot currently match.

What Does a $1,201 Price Target Actually Require From Axon?

TIKR’s mid-case model targets around $1,201 for Axon, built on around 23% annual revenue growth through 2030 and net income margins expanding toward 20%. Based on the current price, that implies an around 205% total return over roughly 4.7 years, or about 27% annualized. The high case gets you toward $3,032 by the full 2034 horizon.

What the Bulls Are Betting On:

- The AI platform keeps compounding. Draft One, which automatically generates police reports from body camera audio and video, is already seeing strong adoption and should drive meaningful upsell within the existing customer base. If it becomes a standard workflow tool for departments, the revenue per customer expands without requiring new hardware sales.

- Federal and international expand the addressable market. Axon has historically been concentrated in U.S. municipal law enforcement, but the federal pipeline and international deployments are both accelerating, opening a significantly larger opportunity than the domestic market alone.

- Operating leverage returns in 2026. The investment cycle that suppressed margins in 2025 should start generating returns this year. If EBITDA margins expand toward the mid-to-high teens, as management has guided, the business’s earnings power will look very different from where it sits today.

What the Bears Are Watching:

- The valuation still requires significant growth. Even at $394, Axon trades at around 51x forward earnings, which assumes continued strong execution. Any guidance reduction tomorrow would likely push the stock lower from already-depressed levels.

- Department budget pressure could slow hardware refresh cycles. Municipal budgets are under pressure in some markets, which could lengthen hardware upgrade cycles and slow near-term revenue growth, even if the platform remains sticky.

- AI competition is not standing still. Motorola, Microsoft, and a growing field of public safety technology startups are all building AI-powered tools for law enforcement. Axon’s early mover advantage is real, but it is not guaranteed to be permanent.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in AXON?

Axon is a business that has been growing revenue at around 30% annually for several years, has a platform with genuine switching costs, is trading at one of the lowest multiples in recent memory, and reports tomorrow. That combination does not come along often.

The question heading into May 6 is whether the Q1 print and full year guidance give investors a reason to close the gap between a $394 stock price and a $702 street consensus. Track revenue growth against the $780 million estimate, any update to full-year guidance, and what management says about the operating margin trajectory in the second half.

Those three things will tell you most of what you need to know. Add Axon to your TIKR watchlist and start your own analysis alongside every other stock on your radar with a free TIKR account.

Analyze AXON stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!