Key Stats

- Current price: ~$166 (May 1, 2026)

- Q1 2026 revenue: $663M, up 69% YoY

- Q1 2026 adjusted EPS: $1.40, up 111% YoY

- Q1 2026 GAAP EPS: $1.01, up 677% YoY

- Q2 2026 revenue guidance: $715M to $725M (~44% YoY growth at midpoint)

- Q2 2026 adjusted EBITDA guidance: $285M to $295M (~40% margin at midpoint)

- TIKR model price target: $402

- Implied upside: ~141%

Reddit Q1 2026 Earnings Breakdown

Reddit stock (RDDT) delivered $663M in Q1 2026 revenue, up 69% year over year, its seventh consecutive quarter of 60%-plus revenue growth.

Adjusted EPS came in at $1.40, up 111% year over year, while GAAP EPS reached $1.01, up 677% from $0.13 in Q1 2025.

Advertising was the primary driver, with ad revenue reaching $625M, up 74% year over year, according to CFO Andrew Vollero on the Q1 2026 earnings call.

Lower-funnel, conversion-driven revenue grew triple digits year over year and represented over 60% of total ad revenue, with strength concentrated in retail, CPG, tech, and media and entertainment.

The number of active advertisers on the platform grew more than 75% year over year, while average revenue per user climbed 44% to $5.23.

Reddit Max, the company’s automated campaign product launched in January 2026, is already delivering measurable results: advertisers using Max campaigns are seeing a 17% reduction in cost per action and 25% more conversion outcomes on average, according to COO Jen Wong.

Other revenue, which includes content licensing, reached $39M, up 15% year over year.

Adjusted EBITDA margin reached 40% in Q1, up roughly 1,100 basis points year over year, according to Vollero.

Free cash flow margin came in at 47%, with capital expenditures of just $1M for the quarter.

For Q2 2026, Reddit guided revenue of $715M to $725M, representing approximately 44% year-over-year growth at the midpoint, against a tough comparable where Q2 2025 ad revenue grew 84%.

The company ended Q1 with $2.8B in cash and investments and approximately $995M remaining on its $1B share repurchase authorization.

Reddit Stock Financials: Margin Expansion in Full Effect

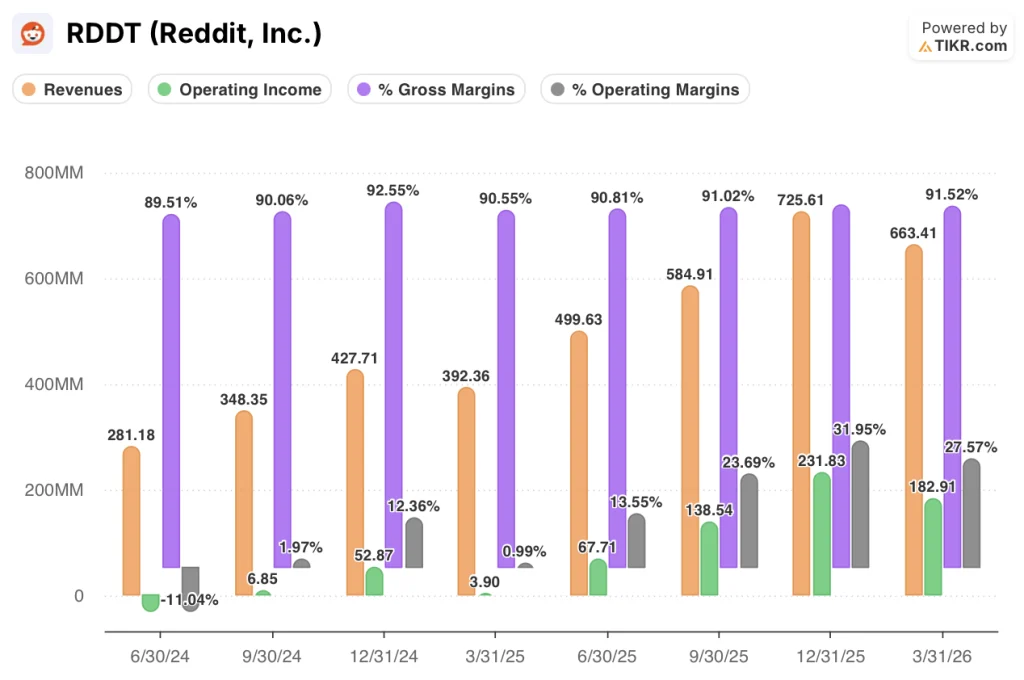

Reddit stock is executing one of the cleanest operating leverage stories in public tech, with operating margins moving from deeply negative to firmly positive across eight consecutive quarters.

Revenue rose from $280M in Q2 2024 to a peak of $726M in Q4 2025 before the typical Q1 seasonal step-down to $663M.

Gross margin has held in a tight band throughout: 89.5% in Q2 2024, moving to 91.9% in Q4 2025, and settling at 91.5% in Q1 2026, reflecting sustained hosting efficiency gains alongside revenue scale.

Operating income swung from a loss of $30M in Q2 2024 to $50M in Q3 2024, then climbed to $230M in Q4 2025 before landing at $183M in Q1 2026, consistent with seasonal patterns.

Operating margin followed the same arc: from negative 11% in Q2 2024 to 27.6% in Q1 2026, a full 38-plus percentage point swing in under two years.

Adjusted operating expenses were approximately 51% of revenue in Q1 2026, down from 61% of revenue in Q1 2025, confirming that the cost base is scaling more slowly than the top line, according to Vollero.

What Does the Valuation Model Say?

The TIKR model prices Reddit stock at $402, implying roughly 141% upside from the current price of ~$166 over approximately 4.7 years, with an annualized return of ~21% under mid-case assumptions.

The model assumes a revenue CAGR of approximately 26% from 2025 through 2035 under the mid case, alongside a net income margin expanding to approximately 33%.

Q1’s combination of 69% revenue growth, 40% adjusted EBITDA margin, and 47% free cash flow margin validates the model’s core assumption that Reddit’s financial profile continues to scale efficiently.

The investment case is meaningfully stronger after this report: Reddit stock now has seven consecutive quarters of 60%-plus revenue growth, an EBITDA margin structure that is already ahead of most software peers at this scale, and a user monetization runway that remains early relative to platform comparables.

Reddit delivered a financially dominant Q1, but the investment argument hinges on whether sustained ad revenue growth can continue while U.S. DAU sits at roughly half the 100 million target.

The demand side is holding: active advertisers grew more than 75% year over year, lower-funnel revenue grew triple digits and represents over 60% of total ad revenue, and Reddit Max is already cutting advertiser cost per action by 17%.

Q2 guidance of approximately 44% year-over-year growth reflects lapping Q2 2025’s 84% ad revenue expansion, and advertisers are signaling shorter planning cycles with lower visibility, leaving limited margin for execution error.

The DAU gap remains the unresolved variable: 200 million Americans use Reddit weekly, but only around 50 million use it daily, and the feed and ML improvements designed to close that frequency gap are mid-deployment with no disclosed KPI movement yet.

Should You Invest in Reddit, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Reddit stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Reddit, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze RDDT stock on TIKR for Free →