Key Stats

- Current price: ~$291 (closed: May 1)

- Q1 2026 revenue: $751M, +130% YoY

- Q1 2026 non-GAAP EPS: $0.44 vs. $0.03 a year ago

- 2026 revenue guidance (raised): $3.4B–$3.8B (midpoint ~80% YoY growth, up from prior $3.1B–$3.3B)

- 2026 non-GAAP EPS guidance (raised): $1.85–$2.25

- TIKR model price target: ~$826 (mid case, realized 12/31/30)

- Implied upside: ~190

Bloom Energy Stock Earnings Breakdown: Q1 2026

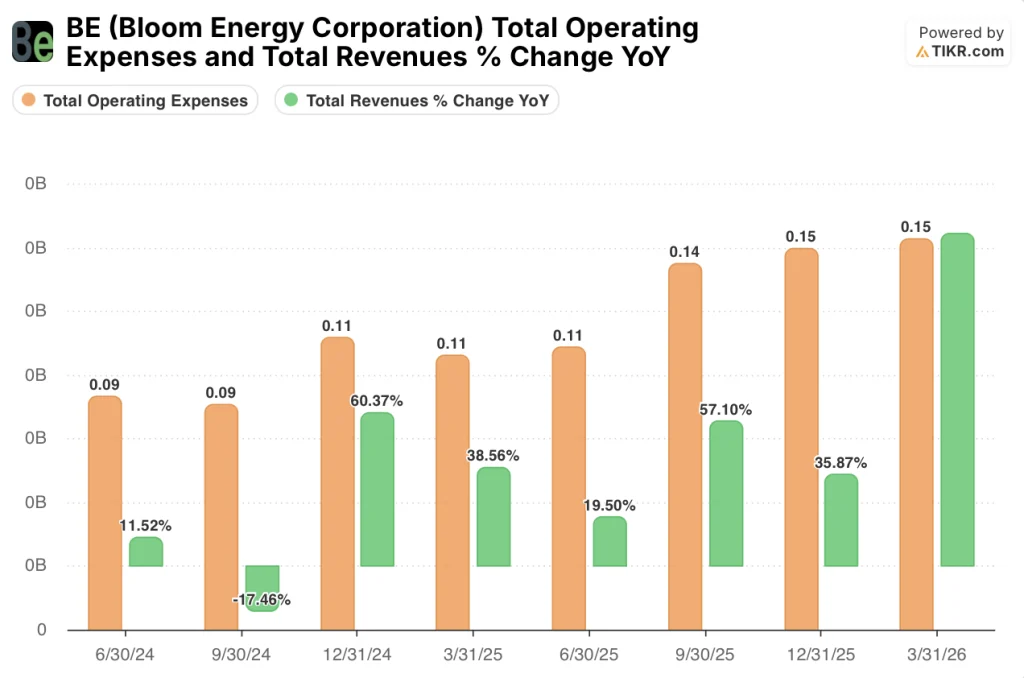

Bloom Energy stock (BE) posted $751M in Q1 2026 revenue, up 130% year over year and representing the first quarter of greater than 100% YoY growth in the company’s public history.

Non-GAAP EPS came in at $0.44 compared to $0.03 in Q1 2025, a roughly 15-fold increase.

Product revenue drove the headline result, reaching an all-time high of $653M for the quarter, up both year over year and sequentially.

Service revenue reached $62M, up 16% year over year, with gross margin in the services segment at 18%, up 13 points from Q1 last year and profitable for the ninth consecutive quarter, according to CFO Simon Edwards on the Q1 2026 earnings call.

Operating income reached $130M compared to $13M in Q1 2025, an increase of $117M, with operating margin expanding to 17% from approximately 4% a year ago, according to CFO Simon Edwards on the Q1 2026 earnings call.

The Oracle Project Jupiter announcement anchored the quarter’s commercial story: Oracle selected Bloom as the sole power provider for a planned multi-gigawatt AI factory in New Mexico, replacing previously planned gas turbines and backup diesel generators with up to 2.45 GW of Bloom Energy Servers.

CEO K.R. Sridhar described the significance: “Becoming the sole power provider for Project Jupiter is a milestone for Bloom, but it’s not going to be a one-off project.”

Bloom raised its 2026 revenue guidance from $3.1B–$3.3B to $3.4B–$3.8B, with the midpoint implying ~80% year-over-year growth, up from the prior midpoint of approximately 60%.

Non-GAAP gross margin guidance increased from approximately 30% to approximately 34%, a roughly 4-point improvement.

Non-GAAP operating income guidance was raised to $600M–$750M, and non-GAAP EPS guidance was set at $1.85–$2.25.

Cash flow from operating activities was positive at $74M in Q1, the first time in Bloom’s history the first quarter has generated operating cash inflow.

Bloom ended the quarter with $2.52B in cash on the balance sheet.

Bloom Energy Stock Financials

The Q1 2026 income statement reflects an inflection in operating leverage: Bloom Energy stock is now generating material operating income on a revenue base that was structurally unprofitable as recently as a year ago.

Revenue grew from $330M in Q1 2025 to $780M in Q4 2025 and came in at $750M in Q1 2026, a modest sequential pullback from Q4 but up 130% from the year-ago quarter.

Gross margin has expanded steadily across the trailing eight quarters, moving from roughly 20% in mid-2024 to 27% in Q1 2025, 33% in Q4 2025, and 30% in Q1 2026.

The slight sequential compression in Q1 2026 from Q4 2025’s 33% to 30% appears to reflect seasonal mix, with management guiding the full-year 2026 gross margin to approximately 34%, according to CFO Simon Edwards on the Q1 2026 earnings call.

Operating margin tells the more striking story: Bloom ran operating losses through Q2 2025, turned profitable at 2% in Q3 2025, scaled to 13% in Q4 2025, and printed 10% in Q1 2026.

On a YoY basis, operating income improved from a loss of approximately $20M in Q1 2025 to a gain of approximately $70M in Q1 2026, a swing of roughly $90M.

The operating leverage embedded in the model is now visible: SG&A and R&D held roughly flat sequentially at approximately $150M combined while revenue nearly doubled year over year.

What Does the Valuation Model Say?

The TIKR model prices Bloom Energy stock at approximately $826 per share in the mid case, implying roughly 192% upside from the model’s base price of approximately $283, with a projected annualized return of ~26% per year through 2030.

The mid case assumes a revenue CAGR of approximately 26% from 2025 to 2035, alongside a net income margin expanding to approximately 25%, a substantial departure from the negative margins Bloom carried through much of its public history.

The Q1 print validates the early phases of that margin expansion: non-GAAP gross margin reached 32% and operating margins are now firmly positive, ahead of where the model would need to be to stay on track.

At current prices near $291, Bloom Energy stock is trading at a premium to the model’s base price of $283, meaning the Q1 results and raised guidance are already partially reflected in the stock.

The investment case strengthened materially this quarter: the Oracle announcement, the operating cash inflow, and the guidance raise all shift the probability distribution toward the mid and high scenarios in the model.

The question for Bloom Energy stock is whether the Oracle-driven demand surge can be sustained, or whether one headline partnership is inflating expectations ahead of execution.

Bull Case

- Q1 revenue of $751M already exceeded the prior full-year quarterly run rate, and management guided Q2 to be “at least as good as Q1,” providing near-term visibility on the raised $3.4B–$3.8B range

- The Oracle deal (up to 2.45 GW in New Mexico) represents a small portion of the data center backlog; management stated that well more than half of the current data center backlog comes from other hyperscalers, neo clouds, and colocation providers

- Service gross margin expanded 13 points year over year to 18%, its highest in at least eight quarters, with a 100% attach rate on all product sales creating a compounding annuity revenue base

- Operating cash flow turned positive for the first time in a Q1 period at $74M, with $2.52B in cash providing runway to fund the capacity expansion without dilutive financing

Bear Case

- The income statement shows sequential revenue contraction from $780M in Q4 2025 to $750M in Q1 2026, driven in part by customers’ greenfield site build timelines; if site delays accelerate across the backlog, revenue recognition could lag the order momentum

- Operating margin compressed sequentially from 13% in Q4 2025 to 10% in Q1 2026, and the path to the guided 34% gross margin for full-year 2026 requires consistent execution in the back half

- The company’s 5 GW annual manufacturing capacity ceiling has not yet been breached; scaling beyond that threshold will require new factory construction, introducing capital intensity and execution risk not yet priced into the model’s 26% revenue CAGR assumption

- Non-GAAP EPS guidance of $1.85–$2.25 for 2026 implies full-year EPS roughly in line with Q1’s $0.44 run rate, meaning there is limited margin for disappointment in Q2 through Q4 to meet the low end

Should You Invest in Bloom Energy Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up BE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Bloom Energy Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze BE stock on TIKR for Free →