Key Stats for ARM Stock

- Past week’s performance: -5.9%

- 52-week range: $100 to $238

- Valuation model target price: $267

- Implied upside: +26.3% over 1.9 years

Value your favorite stocks like ARM with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Arm Holdings plc (ARM) fell roughly 6% over the past week, but shares remain up 84% in 2026 year to date. The pullback came ahead of the company’s fiscal Q4 2026 earnings release, scheduled for May 6.

Shares had surged nearly 97% over the prior three months, so some profit-taking was widely expected. Investor caution also grew because the consensus analyst price target sits near $164, well below the current price of $211.

ARM continued advancing its AI positioning during the period. The company unveiled its new AGI CPU and announced a strategic collaboration with IBM to expand enterprise computing capabilities. Both moves reinforced ARM’s role as a foundational technology layer for the global AI infrastructure buildout.

CEO Rene Haas took on an expanded role at SoftBank Group International, ARM’s majority owner, in April. That development raised questions about management bandwidth at a critical moment. CFO Jason Child also disposed of shares worth $3.8 million during the same period.

Going forward, fiscal Q4 2026 earnings on May 6 will determine whether recent momentum resumes or the stock pulls back further toward its 50-day moving average near $150.

See analysts’ growth forecasts and price targets for ARM (It’s free) >>>

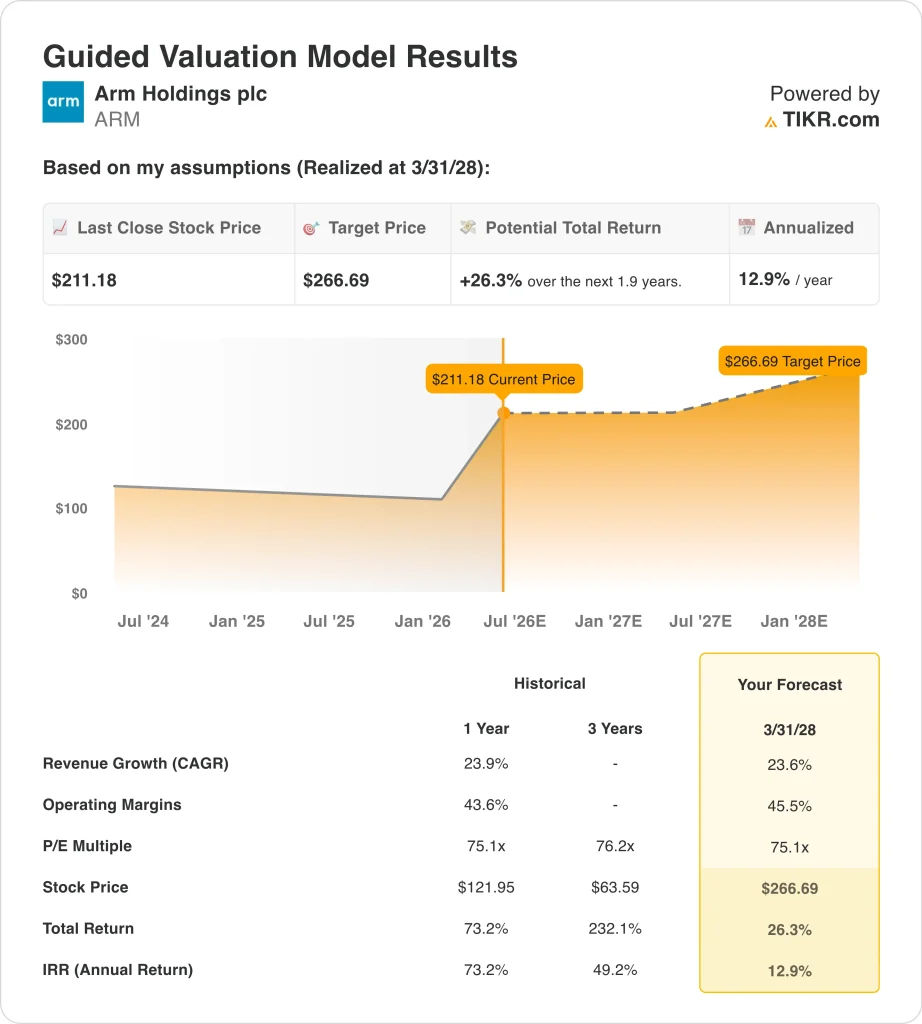

Is ARM Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 23.6%

- Operating Margins: 45.5%

- Exit P/E Multiple: 75.1x

Based on these inputs, the model estimates a target price of $267, implying +26.3% total upside from the current share price and a 12.9% annualized return over the next 1.9 years.

The 12.9% annualized return sits just above the 10% level where a stock becomes genuinely attractive for long-term investors. ARM grew revenue 23.9% in the past year, so the model’s 23.6% CAGR assumption simply holds that pace steady. But the stock trades at over 109 times forward earnings, which is a very high bar. Any miss on earnings could punish the stock sharply.

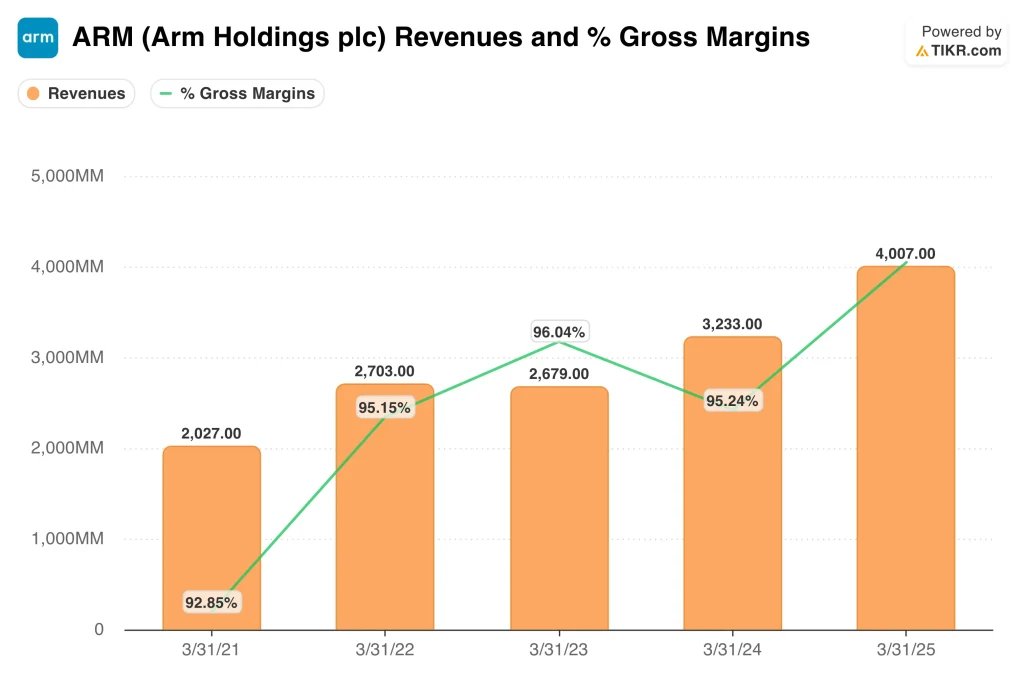

ARM licenses its chip architecture rather than manufacturing products itself. That asset-light model allows the company to sustain gross margins above 95% while keeping the cost base relatively fixed. So operating margins above 45% are realistic if royalty revenue continues growing at this pace.

The exit multiple of 75.1x reflects the scarcity of high-quality IP licensing businesses at this scale. But multiple compression is a real risk. If AI chip investment cycles slow or open source architectures gain ground, that premium could compress faster than the model assumes.

What’s Driving ARM Stock Going Forward?

Fiscal Q4 2026 earnings on May 6 are the single most important near-term catalyst for ARM. Analyst estimates call for revenue near $1.53B and EPS of about $0.56 to $0.59. A strong beat would validate the AI royalty thesis and likely push shares back toward the $238 high. Anything below expectations could accelerate the current pullback.

The new AGI CPU launch targets agentic AI, meaning AI systems that autonomously take actions and make decisions without constant human input. This is one of the fastest-growing segments in technology infrastructure. ARM architecture is already embedded in billions of chips globally, so the extension into data center AI CPUs is a natural and credible next step.

Morgan Stanley highlighted recently that agentic AI is expanding chip spending beyond graphics processors into CPUs. That directly benefits ARM because nearly every CPU in the market uses ARM architecture or licenses from ARM. IBM’s collaboration adds large enterprise customers to the demand picture.

Longer term, royalty rates may rise as AI-specific chips that incorporate ARM architecture command higher average selling prices. Revenue per chip shipped could grow even without volume acceleration. That dynamic supports the margin expansion assumptions built into the valuation model and makes the long-term thesis more durable than near-term sentiment might suggest.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Arm Holdings?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ARM, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ARM alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Arm Holdings stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!