Key Stats for UPS Stock

- Past week’s performance: consolidating

- 52-week range: $82 to $122

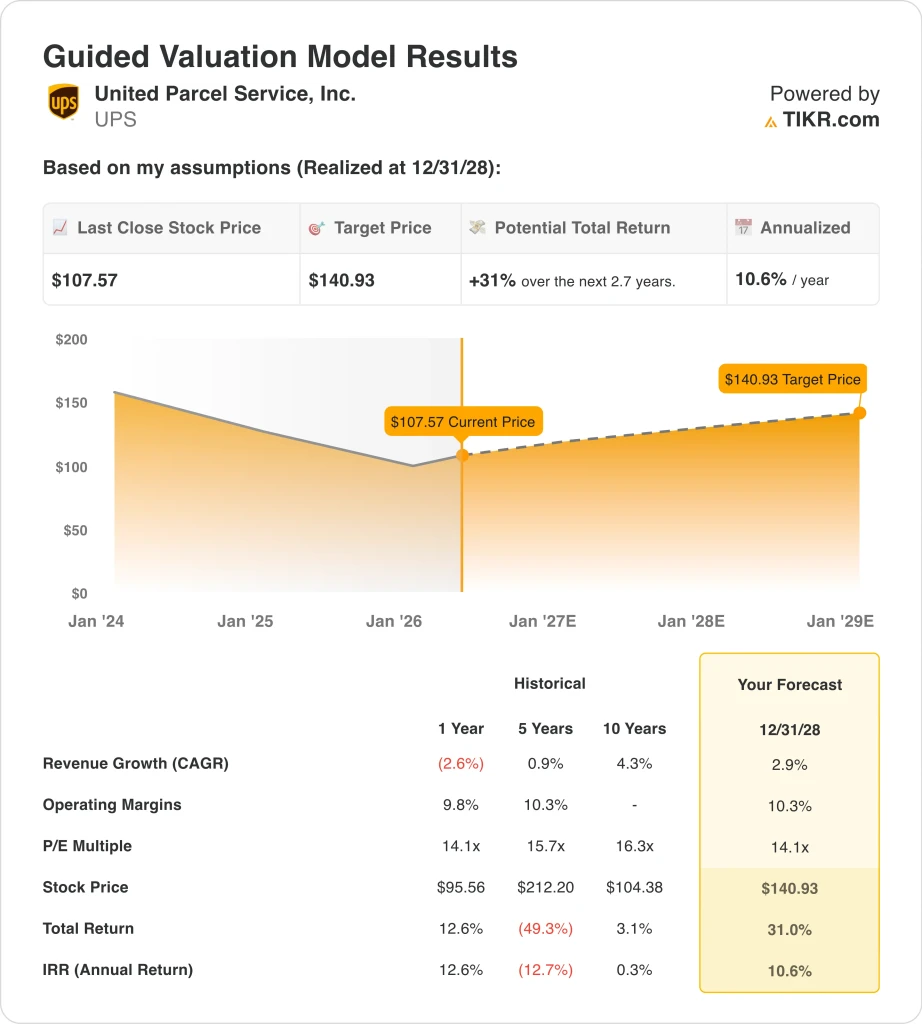

- Valuation model target price: $141

- Implied upside: 31% over 2.7 years

Value your favorite stocks like UPS with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

United Parcel Service (UPS) reported Q1 2026 earnings on April 28 and delivered a modest but meaningful beat on both revenue and profit. Revenue came in at $21.2B, topping the consensus estimate of $21.0B.

Adjusted EPS of $1.07 beat the $1.02 estimate by about 4.9%. And UPS maintained its full-year revenue guidance, which was a clear positive signal for investors who feared a downward revision.

But investor tone after the report remained cautious because management flagged several risks ahead. The CEO said higher fuel costs and softening U.S. consumer confidence are among the factors that could hurt demand.

The CFO added that elevated fuel prices could ultimately reduce shipping volume if customers pull back on purchasing behavior. Fuel is one of UPS’s largest operating expenses, so any sustained oil price increase directly pressures operating margins.

Geopolitical risk is part of the fuel cost story. UPS noted that a potential fuel price spike tied to tensions in the Middle East represents a real downside scenario. Also relevant is trade policy uncertainty.

Both UPS and FedEx pledged to return any tariff-related refunds to customers, reflecting an effort to stay competitive and protect customer relationships during an unsettled trade environment.

And the Teamsters union reached a settlement with UPS on driver severance packages in early April, removing a labor overhang that had been weighing on sentiment.

CEO Carol Tome highlighted UPS’s healthcare and pharmaceutical delivery strategy as a key offset to macro uncertainty. UPS has been expanding specialized logistics for drug makers, including temperature-controlled shipping for medications and medical devices.

Tome described drug delivery as a good antidote to economic uncertainty, because healthcare shipping demand tends to hold up better than consumer package volume during slowdowns. Going forward, investors will focus on whether the healthcare pivot grows fast enough to offset softness in the core small-package business.

See analysts’ growth forecasts and price targets for UPS (It’s free) >>>

Is UPS Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 2.9%

- Operating Margins: 10.3%

- Exit P/E Multiple: 14.1x

Based on these inputs, the model estimates a target price of $141, implying 31% total upside from the current share price of $108 and a 10.6% annualized return over the next 2.7 years.

The model assumptions are conservative and grounded in UPS’s recent financial history. Revenue declined 2.6% in the past year, so a 2.9% forward growth rate simply assumes the business stabilizes and resumes modest expansion. The operating margin target of 10.3% matches UPS’s 5-year historical average, so the model expects consistency rather than a dramatic improvement.

The 14.1x exit P/E also aligns with UPS’s historical trading range. At about $108, the stock sits well below its 52-week high of $122. That compressed valuation partly reflects uncertainty around near-term volume trends and fuel cost exposure. But a company generating $21B in quarterly revenue with a 6.1% dividend yield and a clear healthcare growth strategy is not obviously impaired.

UPS competes directly with FedEx in the U.S. domestic package market. Both companies have pivoted toward healthcare and specialized logistics as they face pressure on standard package volumes. UPS’s LTM EBIT margin of about 8.8% currently sits below the model’s 10.3% target.

The 6.1% dividend yield is the most immediate attraction for income-oriented investors. UPS has held its quarterly payout at $1.64 per share consistently, and free cash flow of $1.2B in Q1 2026 supports that payment even when earnings are compressed.

What’s Driving UPS Stock Going Forward?

The healthcare logistics strategy is the most important long-term catalyst for UPS. CEO Carol Tome has made pharmaceutical and medical delivery a central pillar of the company’s differentiation from competitors. Healthcare companies need specialized transport for biologics, lab equipment, and time-sensitive medications, and UPS is investing in temperature-controlled and time-definite shipping capabilities to serve that market.

Q2 2026 earnings are due July 28 and will be the next key test for sentiment. Analysts expect Q2 revenue of about $21.6B and EPS around $1.64. Investors will watch closely for any change to full-year guidance.

UPS held its full-year target after Q1, but fuel costs and consumer confidence remain acknowledged risk factors. A sustained fuel price spike before Q2 reports could force a guidance revision and pressure the stock further.

The Annual General Meeting on May 7 is a near-term event where shareholders vote on the 2026 long-term performance plan. That plan determines how management compensation aligns with UPS’s recovery targets over the next several years. Clarity on incentive structures helps institutional investors assess whether leadership is fully aligned with the right long-term metrics.

The tariff refund pledge alongside FedEx is also worth monitoring for competitive implications. Both carriers are committed to passing tariff-related refunds back to customers, but the broader trade environment remains uncertain.

A prolonged reduction in cross-border volume could weigh on UPS’s international package segment, which generated $5.3B in Q4 2025. Analysts currently project a forward 2-year revenue CAGR of about 2.7%, and the key question is whether the healthcare and drug delivery pivot can push growth meaningfully above that baseline before the end of 2028.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in United Parcel Service?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UPS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track UPS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze United Parcel Service stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!