Key Stats for Nebius Stock

- 52-Week Range: $23.25 to $168.71

- Current Price: $141.19

- Street Mean Target: ~$170

- Market Cap: $35.7 billion

- Forward 2-Year Revenue CAGR: around 336%

Value your favorite stocks like NBIS with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

Nebius Just Reported Q1 2026 Earnings, Here Is What the Numbers Show.

Nebius (NBIS) builds full-stack AI infrastructure, designing its own server racks, networking software, and GPU clusters for AI training and inference workloads. Spun out from Yandex’s international operations in 2024, it came into existence with something most startups never have: hundreds of experienced infrastructure engineers and roughly $2.5 billion in starting capital.

Q1 2026 results reported this week came in ahead of expectations. Analysts had forecast a loss of $0.81 per share on revenue of around $375 million. The stock moved up around 4% on the day, adding to a one-year return of 492%.

The contract backlog is what underpins the whole story. Nebius closed a $19.4 billion deal with Microsoft in September 2025, a $27 billion partnership with Meta in December, and Nvidia followed with a $2 billion direct equity investment.

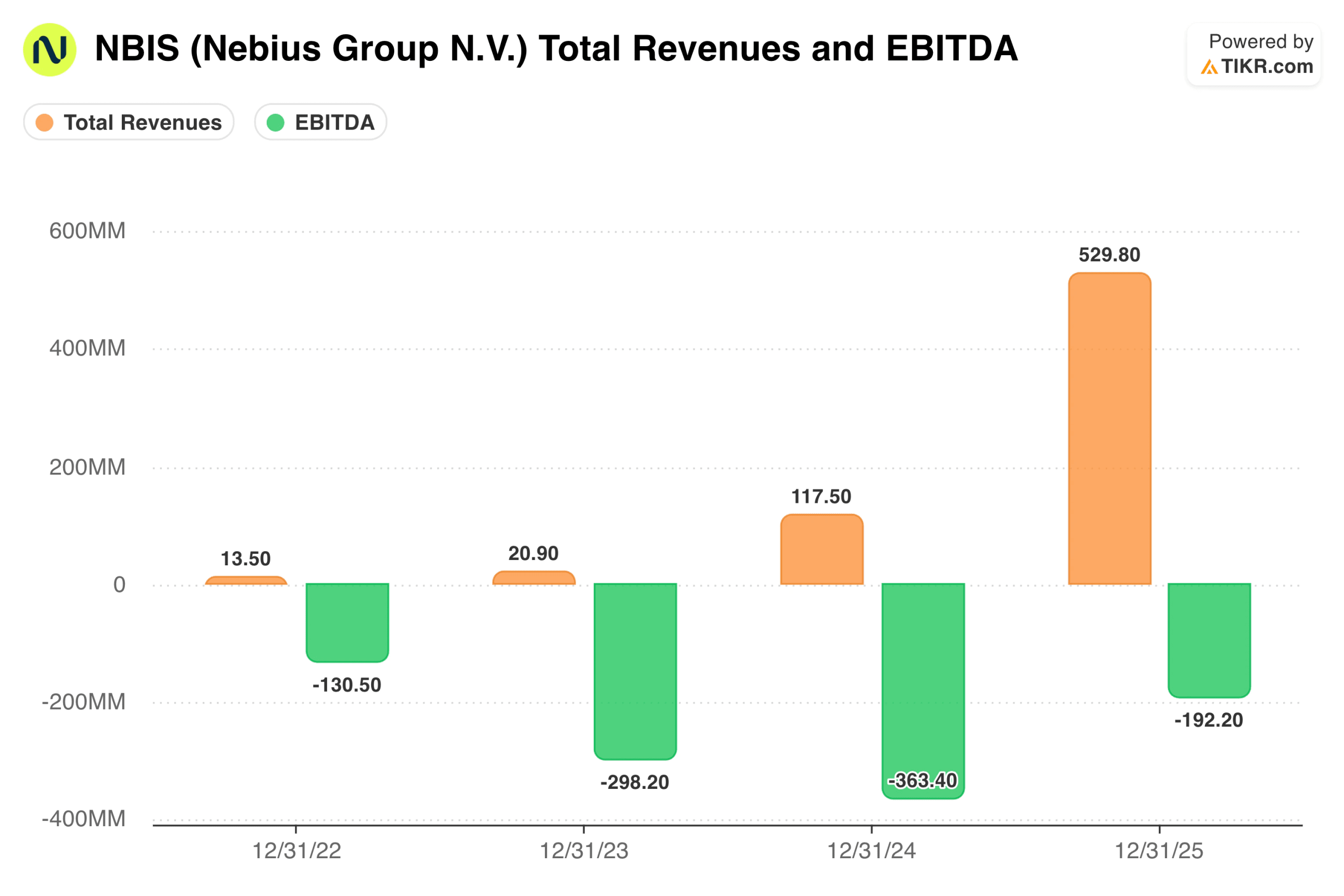

Total contracted backlog now approaches $50 billion through 2031, against 2025 revenue of $530 million. Full year 2026 guidance stands at $3 to $3.4 billion, roughly a sixfold increase, with adjusted EBITDA margins of around 40% targeted by year-end.

See analysts’ growth forecasts and price targets for NBIS (It’s free) >>>

What Wall Street Is Saying About Nebius

The analyst community holds a strong buy consensus, with price targets ranging from around $143 to $200. BofA raised its target to $175 in April, citing new contracts with CoreWeave as further validation of demand. DA Davidson and BWS Financial are at $200.

The counterargument is harder to find in the formal analyst community, but it is worth knowing. Wolfe Research initiated at Peer Perform, acknowledging the demand story as proven but flagging execution and financing risk. Insider selling of around $14.7 million over the past 90 days, including by CEO Arkady Volozh, has added caution for some investors.

Nebius also missed revenue estimates in three of its last four quarters before today’s print, which is a relevant data point for a stock trading at over 11x forward revenue

Nebius Stock Financials: The Revenue Acceleration Is Real

The quarterly revenue chart tells the story more clearly than any prose summary could. Revenue went from $11.4 million in Q1 2024 to $227.7 million in Q4 2025, an acceleration that very few infrastructure companies have matched at this scale. Each bar in that chart represents new capacity coming online, new contracts converting into revenue, and a business model that works in practice, not just on paper.

The annual picture adds important context. EBITDA losses have widened in absolute terms as the buildout has accelerated, but they are narrowing significantly as a percentage of revenue. The business went from a negative EBITDA of $363 million in 2024 to $192 million in 2025, while revenue grew by more than four times. The direction is right, even if profitability is still a future milestone.

Getting there requires significant capital. Nebius is spending $16-$20 billion in capital expenditures in 2026 alone, funded by a $4 billion convertible debt raise. The 2026 capex plan covers new AI factory campuses in Finland, Missouri, and Alabama. The Missouri campus alone is approved for up to 1.2 gigawatts of capacity. At full build, that infrastructure footprint would put Nebius in a category occupied by very few companies globally.

CoreWeave is the most direct comparable, though Nebius’s vertically integrated model, European data center presence, and proprietary infrastructure stack give it a meaningfully differentiated position. The company also designs its own InfiniBand-based networking software called Nebius Fabric, which enables lower latency and more competitive pricing than general-purpose cloud providers for AI-specific workloads.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Nebius?

Nebius is one of the most straightforward high-conviction bets in AI infrastructure and one of the most demanding. The contracted backlog is real, the hyperscaler relationships are real, and the Nvidia equity investment is about as strong a technical endorsement as the industry offers.

At $141 with a forward revenue CAGR of around 336%, you are paying for a business that needs to execute a sixfold revenue expansion in a single year while managing one of the largest infrastructure buildouts in the technology sector. Add Nebius to your TIKR watchlist and track quarterly revenue against the $3 to $3.4 billion full-year guidance.

Each earnings print between now and year-end will tell you whether the acceleration visible in that quarterly chart is holding. Start your own analysis of NBIS alongside every other stock on your radar with a free TIKR account.

Analyze NBIS stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!