Key Stats

- Current price: ~$79 (April 30, 2026)

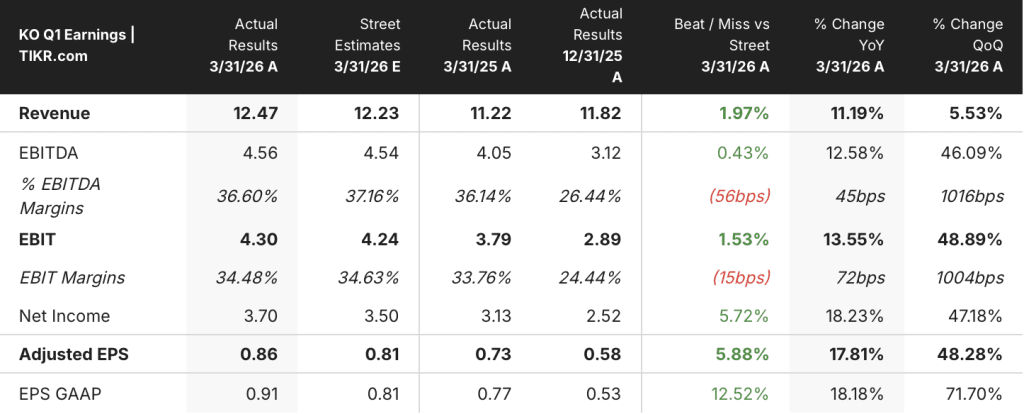

- Q1 2026 revenue: $12.5B, up 11% YoY

- Q1 2026 comparable EPS: $0.86, up 18% YoY

- Full-year 2026 organic revenue growth guidance: 4% to 5% (unchanged)

- Full-year 2026 comparable EPS growth guidance: 8% to 9% vs. $3.00 in 2025 (raised from 7% to 8%)

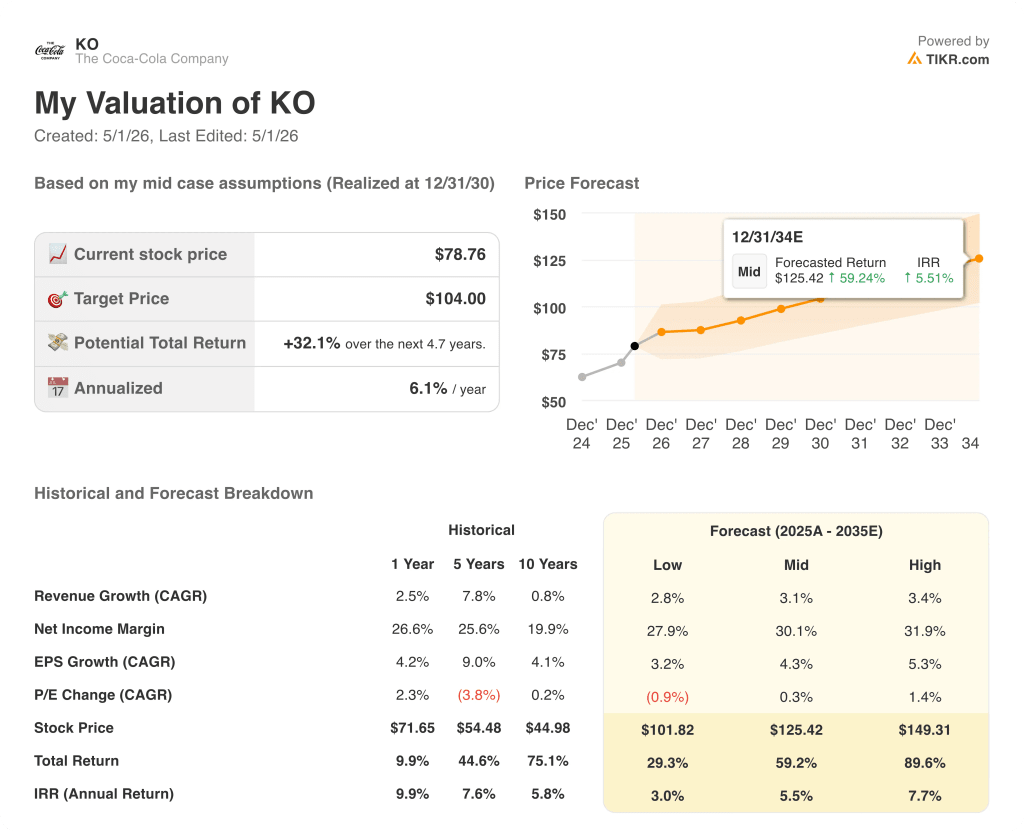

- TIKR model price target: $104

- Implied upside: ~32%

Coca-Cola Stock Posts 18% EPS Growth as Q1 Organic Revenue Runs at 10%

Coca-Cola stock (KO) delivered a standout first quarter, with comparable EPS of $0.86 rising 18% year-over-year and revenue of $12.5B growing 11% against the prior-year period.

Organic revenue grew 10%, driven by 3% unit case volume growth across all operating segments and 2% price/mix growth, according to CFO John Murphy on the Q1 2026 earnings call.

Volume grew in every operating unit, extending what management described as 20 consecutive quarters of overall value share gains.

North America contributed solid results, with 4% volume growth and broad-based gains across trademark Coca-Cola, BODYARMOR, Powerade, smartwater, and Minute Maid.

Latin America grew volume, revenue, and profit, with strength in Brazil and Central America more than offsetting declines in Mexico, where a newly implemented sugar tax weighed on results.

EMEA grew volume across all operating units and gained value share, though management noted volume in Eurasia and the Middle East declined in March following escalation of the regional conflict.

Asia Pacific posted volume growth across all operating units but saw profit decline, driven by commodity pressure in tea and coffee and the phasing of inventory costs, according to Murphy on the call.

Comparable gross margin declined approximately 30 basis points, primarily from commodity cost pressures in tea and coffee businesses and the phasing of inventory costs, while comparable operating margin expanded approximately 70 basis points as operating expense efficiencies offset those pressures.

Coca-Cola stock raised its full-year 2026 comparable EPS growth outlook to 8% to 9% versus $3.00 in 2025, up from the prior 7% to 8% range, citing a 1-point reduction in the underlying effective tax rate to 19.9%.

Free cash flow was approximately $1.8B in Q1, up versus the prior year, and the company carries net debt leverage of 1.6x EBITDA, below its targeted range of 2.0x to 2.5x.

The pending sale of Coca-Cola Beverages Africa, expected to close in the second half of 2026, is projected to represent an approximate 4-point headwind to comparable net revenues and an approximate 1-point headwind to comparable EPS.

Coca-Cola Stock Financials: Operating Leverage Returns to the P&L

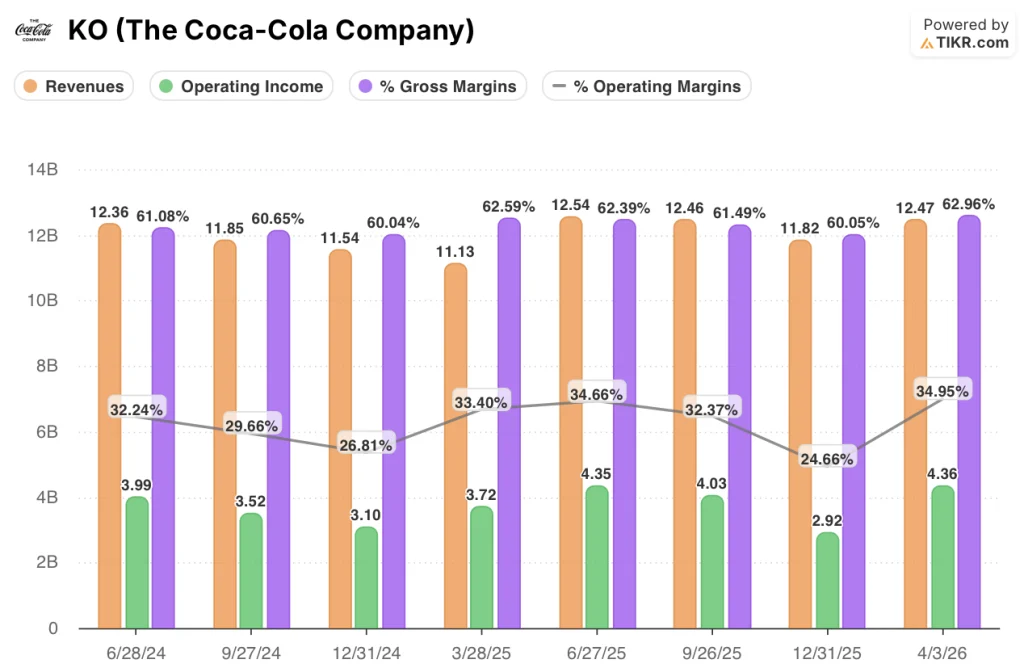

The Q1 income statement shows a business where operating leverage has reasserted itself above the gross margin line, even as commodity-driven gross margin compression created a near-term divergence between the two margin lines.

Revenue recovered from a dip to $11.1B in Q1 2025 and climbed steadily through $12.5B in Q2 2025, $12.5B in Q3 2025, $11.8B in Q4 2025, and now $12.5B in Q1 2026, a trajectory that confirms the 11% year-over-year advance is not a one-quarter anomaly.

Gross margin reached 63% in Q1 2026, up from 63% in Q1 2025, though management attributed approximately 30 basis points of underlying gross margin pressure in Q1 to tea and coffee commodity costs and an inventory phasing item in Asia Pacific that Murphy characterized as a one-off.

Operating income came in at $4.4B, up 17% year-over-year from $3.7B in Q1 2025, and operating margin expanded to 35% from 33% in the prior-year quarter.

The operating margin expansion reflects meaningful SG&A efficiency: total operating expenses fell to $3.5B in Q1 2026 from $3.3B in Q1 2025 on a much higher revenue base.

Murphy noted on the call that 2/3 of the gross margin compression in Q1 was attributable to the inventory item in Asia Pacific, framing the underlying annual gross margin trajectory as broadly intact.

What Does the Valuation Model Say?

The TIKR model prices Coca-Cola stock at $104, implying approximately 32% total return potential from the current price of ~$79 over the next ~5 years, or about 6% annualized.

The model assumes a revenue CAGR of 3% and a net income margin of 30% in the mid-case scenario, figures that now look achievable given Q1’s operating leverage and the tax rate revision that lifted full-year EPS guidance.

Q1’s combination of 18% EPS growth, a guidance raise, and margin expansion removes near-term execution risk from the thesis and tilts the risk/reward picture modestly in favor of long-term holders.

At current prices, Coca-Cola stock is not cheap relative to its growth rate, but the TIKR model’s $104 target suggests the market is still not fully pricing the multi-year earnings compounding capacity embedded in the franchise.

The central tension: Coca-Cola stock’s bull case depends on whether operating margin expansion can continue even as commodity costs in tea, coffee, and packaging pressure the system in 2026 and beyond.

Bull Case

- Operating margin expanded to 35% in Q1 2026 from 33% in Q1 2025, with operating income growing 17% YoY to $4.4B, demonstrating that SG&A efficiency is more than offsetting gross margin headwinds.

- The CCBA divestiture, expected in H2 2026, will mechanically lift consolidated margins by removing a lower-margin bottling business from the P&L.

- The full-year EPS guidance raise to 8% to 9% growth, driven partly by the tax rate reduction to 19.9%, provides a more durable earnings floor for multiple expansion.

- Volume growth across all operating units and 20 consecutive quarters of value share gains indicate the brand portfolio is executing ahead of peers in a pressured consumer environment.

Bear Case

- Comparable gross margin declined approximately 30 basis points in Q1, and Murphy acknowledged on the call that tea and coffee commodity pressure will continue through the year.

- Price/mix growth of only 2% reflects affordability investments and geographic mix headwinds that could persist if low-income consumer pressure intensifies across Latin America and Asia Pacific.

- The TIKR model’s mid-case assumes a 3.1% revenue CAGR, which requires consistent volume and pricing execution in markets where Mexico’s sugar tax, Middle East conflict impact, and APAC inventory normalization all represent active headwinds in 2026.

- Free cash flow generation remains subject to the unresolved IRS tax dispute, which management cited as a reason for maintaining a conservative 1.6x net leverage position rather than accelerating capital returns.

Should You Invest in The Coca-Cola Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up KO stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Coca-Cola Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze KO stock on TIKR for Free →