Key Stats for POOL Stock

- Past week’s performance: -5.3%

- 52-week range: $195 to $345

- Valuation model target price: $267

- Implied upside: 25.1% over 2.7 years

Value your favorite stocks like POOL with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Pool Corporation (POOL) fell about 5.3% over the past week, and the decline came even after the company reported a solid earnings beat on April 23, 2026. Pool Corp is the world’s largest wholesale distributor of swimming pool supplies, equipment, and maintenance products.

It serves roughly 125,000 wholesale customers through approximately 455 sales centers across North America, Europe, and Australia. The business sits between about 3,500 suppliers and a large customer base of pool service professionals, builders, and specialty retailers.

First-quarter 2026 results were strong across most key metrics. Net sales reached $1.14 billion, up 6% year over year, and operating income rose 7% to $82.6 million. Non-GAAP EPS came in at $1.43, beating the Wall Street consensus of $1.35 by about 6%. So the stock initially surged 4.6% in pre-market trading after the announcement.

But the initial excitement faded quickly as the week progressed. Bank of America lowered its price target on Pool Corp to $226 from $229 and kept its Underperform rating on the shares. Investor sentiment also cooled as questions around new pool construction and consumer discretionary spending remained unresolved.

CEO Peter Arvan acknowledged the environment on the earnings call, stating that the company continues to “navigate a challenging consumer environment.” Pool confirmed its full-year 2026 EPS guidance of $10.87 to $11.17 per diluted share. Management expects new pool construction to remain near 58,000 units in 2026, staying close to 2025 levels.

Going forward, investors will watch whether Pool’s maintenance-driven revenue base holds up through the critical spring and summer selling months.

See analysts’ growth forecasts and price targets for POOL (It’s free) >>>

Is POOL Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 3.7%

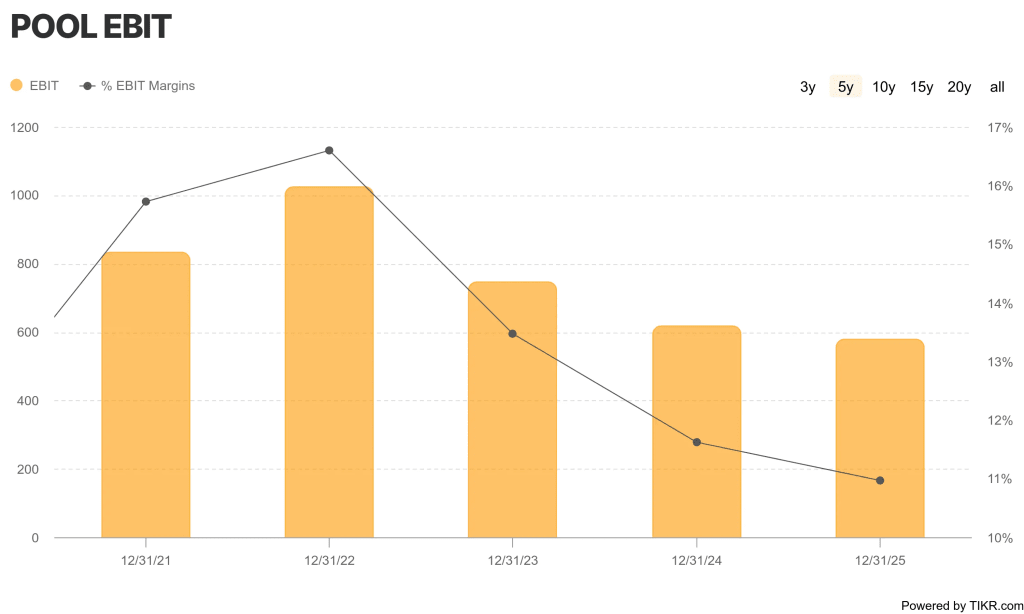

- Operating Margins: 11.2%

- Exit P/E Multiple: 19x

Based on these inputs, the model estimates a target price of $267, implying a 25.1% total return from the current share price of $213 and an annualized return of 8.7% per year over the next 2.7 years.

The revenue growth assumption of 3.7% is modest but deliberate. Pool’s revenue grew at an 8.4% annual rate over the past 10 years, so the model is not embedding any recovery in new pool construction. But at 8.7% annualized, the stock does not screen as deeply undervalued at today’s price. Investors targeting double-digit annual returns may find the risk-reward somewhat limited at current levels.

The exit P/E multiple of 19.0x is also well below Pool’s five-year historical average of 26.2x. So the model is being conservative on both growth and valuation, and still only projects moderate returns. That suggests the stock has not yet fallen far enough to price in a compelling margin of safety, even though the underlying business remains fundamentally sound.

Pool’s competitive moat is real and durable. The company holds an estimated 25% to 35% share of the U.S. pool supply market, which is valued at roughly $16 billion. And it serves an installed base of 5.5 million in-ground pools across North America.

The bigger valuation re-rating would likely require a recovery in new pool builds, and that depends on mortgage rates and housing market conditions that are outside Pool’s direct control. But the growing mix of higher-margin private label chemicals and the steady gain of Pool’s digital ordering platform, Pool360, are gradual tailwinds that are improving the quality of earnings over time.

What’s Driving POOL Stock Going Forward?

Pool’s most immediate catalyst is its Investor Day webcast on May 12, 2026. Management is expected to lay out strategic initiatives and long-term financial targets at that event. So this is a near-term opportunity to reset investor expectations, especially on the company’s margin improvement roadmap and digital expansion plans.

Pool360, the company’s digital B2B ordering platform, continues to grow and now represents 13% of total net sales, up from 12.5% a year ago. Some high-performing branches are already exceeding 30% digital utilization. Because Pool360 reduces friction for wholesale customers, it tends to drive loyalty and repeat ordering behavior, which supports revenue visibility and operating efficiency over time.

Private label and proprietary chemical products are another driver worth watching closely. These products carry higher margins than branded third-party alternatives, and Pool has been steadily expanding this category.

Management noted in the Q1 earnings call that chemical pricing appears stable and not subject to structural decline, which removes a near-term headwind and supports the gross margin trajectory. The biggest long-term catalyst remains a recovery in new pool construction. New builds are expected to stay near 58,000 units for 2026, but in peak years, that number ran as high as 75,000 to 100,000 units.

CEO Peter Arvan was clear on the Q1 call that Pool’s growth thesis does not require new construction to recover, because the business is anchored in maintenance and remodeling of the existing installed base. But with Q2 2026 results scheduled for July 23, investors will soon get a read on how Pool performed during the heart of its peak selling season.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Pool Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up POOL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track POOL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze POOL stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!