Key Stats

- Current price: ~$935 (April 30, 2026 close, +9.8% on earnings day)

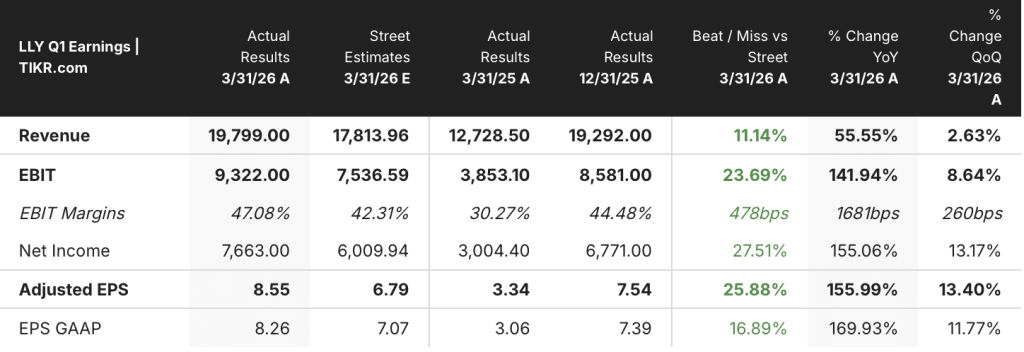

- Q1 2026 revenue: $19.8B (+56% YoY)

- Q1 2026 non-GAAP EPS: $8.55 (vs. $3.34 in Q1 2025)

- Mounjaro + Zepbound combined Q1 revenue: $12.8B

- Full-year 2026 revenue guidance: $82B–$85B (raised $2B at both ends; midpoint implies ~28% growth)

- Full-year 2026 non-GAAP EPS guidance: $35.50–$37.00 (raised $2 at both ends)

- Q1 dividends distributed: $1.5B

- Q1 share repurchases: $2.4B

- TIKR model price target: ~$1,736 (+86% implied upside)

Eli Lilly Stock Delivers a $19.8B Quarter as Incretins Drive 56% Revenue Growth

Eli Lilly stock (LLY) surged nearly 10% after the company reported Q1 2026 revenue of $19.8B, a 56% year-over-year increase driven by the continued scaling of its GLP-1 franchise.

Non-GAAP EPS came in at $8.55, up from $3.34 in Q1 2025, according to CFO Lucas Montarce on the Q1 2026 earnings call.

Mounjaro and Zepbound generated $12.8B in combined global revenue, adding $6.7B of growth versus the same quarter last year, according to Montarce on the Q1 2026 earnings call.

The U.S. incretin obesity market grew total prescriptions by over 80% in Q1, with Zepbound gaining share at an even faster pace, according to President of Lilly USA Ilya Yuffa on the Q1 2026 earnings call.

Self-pay accounted for approximately 45% of total Zepbound prescriptions in Q1 and 55% of new prescriptions.

International Mounjaro sustained momentum as well, with Lilly holding above 53% share of the market outside the U.S. and delivering over 60% share in Brazil and Korea, according to President of Lilly International Patrik Jonsson on the Q1 2026 earnings call.

Foundayo, Lilly’s newly approved oral GLP-1 for obesity (orforglipron), launched into pharmacies on April 9 with roughly 20,000 patients treated as of the earnings call, 80% of whom were new to the GLP-1 class, according to Yuffa.

Beyond the incretin franchise, Lilly’s Immunology, Oncology, and Neuroscience portfolio grew 160% year over year collectively.

Jaypirca global sales grew 79% versus Q1 2025, and Inluriyo captured over 35% share of new patient starts in metastatic breast cancer in its first full launch quarter, according to Montarce on the Q1 2026 earnings call.

Management raised full-year 2026 revenue guidance by $2B at both ends to $82B–$85B, with the midpoint representing 28% growth versus 2025.

Full-year non-GAAP EPS guidance was raised by $2 at both ends to $35.50–$37.00.

Lilly distributed $1.5B in dividends and repurchased $2.4B in shares during Q1.

U.S. price declined 7% in Q1, including the impact of direct-to-patient pricing for Zepbound, with Montarce noting that excluding a one-time rebate adjustment, the underlying decline was approximately 10%.

Eli Lilly Stock’s Margin Expansion Story Is Now Running at Full Speed

The income statement tells a clear operating leverage story: revenue is compounding faster than costs, and the margin line is moving with it every quarter.

Revenue has expanded sequentially and year over year across every period shown in the screenshot, reaching $19.8B in Q1 2026 from $12.7B in Q1 2025 and $17.6B in Q3 2025.

Gross margin came in at 82% in Q1 2026, down approximately 1 percentage point from 83% in Q1 2025, a compression Montarce attributed primarily to lower realized prices on the Q1 2026 earnings call.

Operating income reached $9.8B in Q1 2026, up 81% from $5.4B in Q1 2025.

Operating margin expanded to 49% in Q1 2026, up from 43% in Q1 2025, continuing a multi-quarter expansion arc that began at 38% in Q2 2024.

Meanwhile, R&D grew 28% year over year and SG&A grew 19%, both growing at a substantially slower rate than the 56% revenue increase, which is the mechanism driving the operating leverage story.

The non-GAAP performance margin reached 50% in Q1, up from 43% in Q1 2025, a 7 percentage point increase according to Montarce on the Q1 2026 earnings call.

What Does the Valuation Model Say?

TIKR’s model prices Eli Lilly stock at a target of ~$1,736, implying roughly 86% upside from the current price of ~$935.

The mid-case model assumes a revenue CAGR of 11.5% and a net income margin of 42%, reaching a forecasted price of ~$2,473 by December 2034, according to the TIKR valuation model.

The annualized return in the mid case is 11.9% per year over approximately 4.7 years, a strong return profile for a company that just posted 56% revenue growth and raised guidance twice in the same report.

Q1 reinforces the credibility of that revenue CAGR assumption: the trailing 1-year revenue CAGR is already 45%, and the trailing 5-year CAGR is 22%, both comfortably above the 11.5% the model requires going forward.

The investment case for Eli Lilly stock is stronger after this quarter, not weaker: operating margin is expanding toward the 42% net income margin the model prices in, guidance has been raised, and the Foundayo launch adds a new volume driver that wasn’t fully priced into the original guidance range.

The central question for Eli Lilly stock is whether the 11.5% revenue CAGR assumption holds as the business scales past $80B in annual revenue and new products move from launch to baseline.

What Has to Go Right

- Foundayo must convert its early 20,000-patient base into a sustained commercial ramp, with commercial PBM access confirmed at 2 of 3 major PBMs by mid-May and Medicare Bridge access beginning July 1, 2026

- International Mounjaro must sustain above-50% share across 55+ launched countries and expand patient activation in penetration-early markets, with Brazil and Korea already demonstrating 60% share as a proof point

- Retatrutide Phase III data (TRIUMPH-1, due later in Q2) must confirm the weight loss profile seen in TRANSCEND-T2D-1, where participants lost 25 to 37 pounds on average, validating the next leg of the incretin portfolio

- Operating margin must hold near 49% or expand further, which Q1’s 7 percentage point YoY non-GAAP margin improvement suggests is achievable as revenue scales faster than SG&A and R&D

What Could Still Go Wrong

- U.S. price declined approximately 10% in Q1 on an underlying basis, and management guided for a low-to-mid-teens price headwind for the full year, meaning sustained volume growth must fully offset an ongoing pricing drag

- Medicaid access losses already suppressed Zepbound prescription growth by high single digits in Q1, and any further coverage rollbacks could weigh on volume in a channel that had been a meaningful growth contributor

- Foundayo is a new molecule and a new brand starting from zero consumer awareness, with full-scale DTC TV advertising not planned until Q3, creating execution risk during a critical launch window

- The TIKR model’s low-case scenario of 10.4% revenue CAGR yields a stock price of ~$1,884 by December 2034, a 101% total return over 4.7 years but at an 8.4% IRR that assumes meaningful underperformance relative to the current trajectory

Should You Invest in Eli Lilly and Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LLY stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Eli Lilly and Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LLY stock on TIKR for Free →