Key Stats

- Current Price: ~$112 (May 1, 2026)

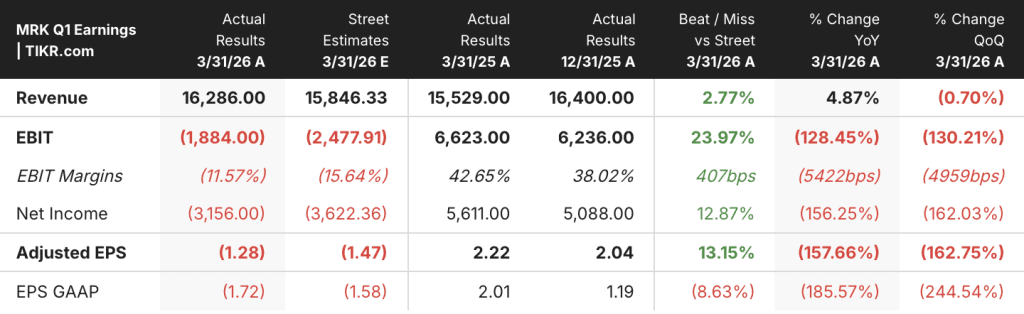

- Q1 2026 Revenue: $16.3B, up ~5% YoY

- Q1 2026 Adjusted EPS: ($1.28), includes ($3.62) one-time Cidara charge; underlying non-GAAP result positive before charge

- KEYTRUDA + KEYTRUDA SC Family Sales: $8B, up 8% YoY

- WINREVAIR Q1 Sales: $525M

- Full-Year 2026 Revenue Guidance: $65.8B to $67B (raised midpoint, 1% to 3% growth)

- Full-Year 2026 Non-GAAP EPS Guidance: $5.04 to $5.16 (raised midpoint; excludes ~$2.35/share Terns charge)

- Gross Margin (Q1 2026): ~82% (non-GAAP)

Merck Stock Q1 2026 Earnings: KEYTRUDA Hits $8B as New Products Gain Ground

Merck stock (MRK) delivered Q1 2026 revenue of $16.3B, a 5% increase year-over-year, driven by continued strength in oncology, a breakout quarter for WINREVAIR, and growing early contributions from over 20 new product launches now underway across the portfolio.

The KEYTRUDA family, which now includes KEYTRUDA SC (subcutaneous), generated $8B in quarterly sales, up 8% on an ex-exchange basis, according to Caroline Litchfield, CFO, on the Q1 2026 earnings call.

Litchfield noted that U.S. KEYTRUDA growth benefited from approximately $250M in timing-related wholesaler purchases, a tailwind that will reverse as a corresponding headwind in Q3 2026.

KEYTRUDA SC, launched as KEYTRUDA QLEX, posted $128M in first-quarter sales following its recent U.S. launch, and received its permanent J-code on April 1, a reimbursement milestone expected to accelerate uptake through the remainder of the year.

WINREVAIR, Merck’s pulmonary arterial hypertension therapy, recorded $525M in global sales, reflecting continued strong demand with more than 1,600 new U.S. patients receiving prescriptions in the quarter, according to Litchfield on the earnings call.

WELIREG, the company’s HIF-2-alpha inhibitor for renal cell carcinoma, grew 43% to $199M, supported by international uptake and expanded U.S. use in certain previously treated advanced RCC patients.

GARDASIL sales declined 22% to $1.1B, driven by lower demand in China and Japan, consistent with management’s expectations, and a 10% U.S. decline tied to the timing of CDC purchases.

OHTUVAYRE, Merck’s novel COPD maintenance therapy, reported $131M in Q1 sales, with Litchfield noting the quarter was adversely impacted by a CMS reimbursement change and Medicare deductible resets, though prescription trends began recovering in March.

The reported adjusted EPS of ($1.28) includes a ($3.62) per-share one-time charge related to the acquisition of Cidara Therapeutics, which triggered a non-tax-deductible pretax loss and a resulting effective tax rate of negative 43.5% for the quarter.

Merck raised and narrowed its full-year 2026 guidance: revenue is now expected between $65.8B and $67B, representing 1% to 3% growth, with roughly 1 percentage point of positive foreign exchange impact at mid-April rates.

Full-year non-GAAP EPS guidance was raised to $5.04 to $5.16, including approximately $0.10 of FX benefit, but excluding the proposed Terns Pharmaceuticals acquisition, which is expected to add a one-time R&D charge of approximately $5.8B (~$2.35/share) upon close.

Merck is on pace for approximately $3B in share repurchases in 2026 and remains committed to growing its dividend over time, with business development continuing as a high capital allocation priority.

On the pipeline, FDA approval of IDVYNSO, a once-daily two-drug HIV regimen of doravirine and islatravir, marked a regulatory milestone in infectious diseases, representing the first approved two-drug regimen that does not include an integrase strand transfer inhibitor.

Priority review was granted for ifinatamab deruxtecan (I-DXd), Merck’s ADC developed with Daiichi Sankyo for extensive-stage small cell lung cancer, with a PDUFA date of October 10, according to Dr. Dean Li, President of Research Labs, on the earnings call.

CEO Rob Davis highlighted the company’s reorganization into a new business unit model organized around products and therapeutic areas, designed to sharpen focus and increase commercial agility as Merck executes across its 20-plus new product launch cycle.

What Does the Valuation Model Say?

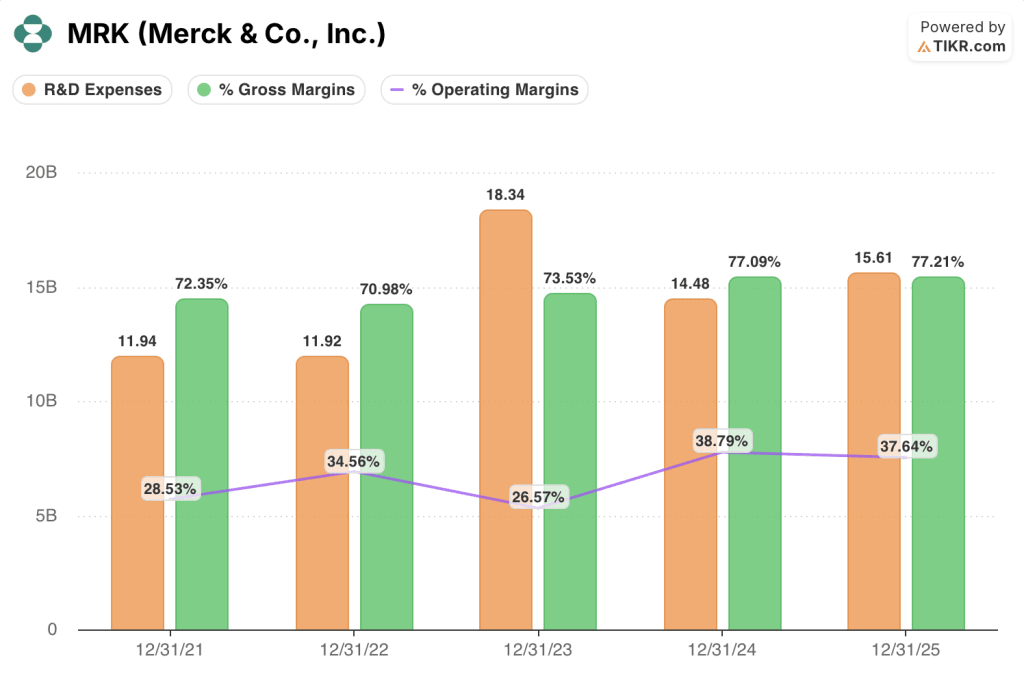

The annual income statement reflects a business running at structurally high gross margins while operating income absorbed significant step-up investment in R&D over the past two years.

Gross margin held near 77% for fiscal years 2024 and 2025, up from 72% in 2021, reflecting the mix shift toward higher-margin oncology products over the period.

Operating margin contracted to 38% in fiscal 2024 before declining to 38% in 2025, compared to a peak of 35% in 2022, though R&D expense increased from $11.9B in 2022 to $15.6B in 2025, reflecting pipeline investment including LaNova and multiple ADC programs.

Also, MRK’s Q1 2026 EBIT loss of $1.9B is entirely attributable to the $9B one-time Cidara charge, which is excluded from non-GAAP results and does not reflect the underlying operating performance of the business.

Excluding the Cidara charge, total non-GAAP operating expenses grew approximately 2% in Q1 2026, with SG&A expected to increase over the remainder of the year as launch investment behind new products accelerates.

Merck Stock Valuation: Modest Upside, Pipeline-Dependent

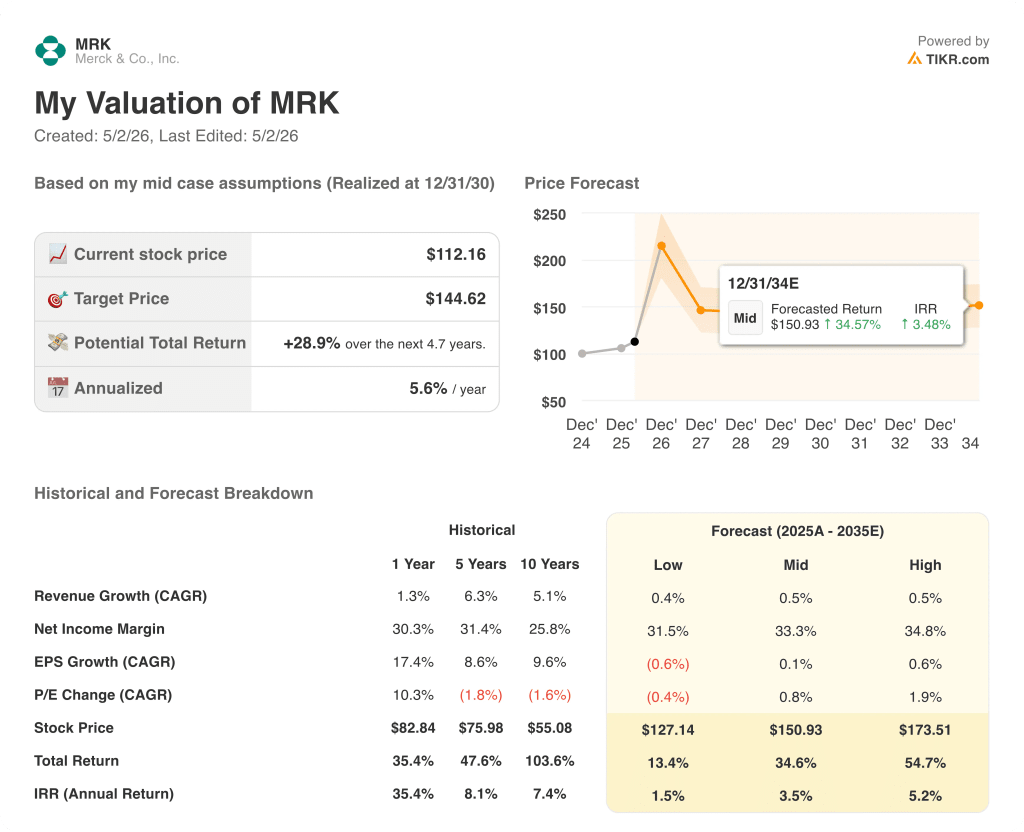

TIKR’s model prices Merck stock at $145 against a current price of ~$112, implying ~29% total return over 4.7 years at an annualized 5.6%.

The mid-case assumes a net income margin of 33%, modest expansion from the 30% posted over the past year, with revenue growth essentially flat at 0.5% CAGR through 2035.

That flat revenue assumption is the tension point: the model’s upside is built almost entirely on margin expansion, not top-line growth, which means the 20-plus product launch cycle has to convert into sustained profitability rather than just revenue diversification.

Pipeline Execution or Margin Disappointment: That’s the Real Debate for Merck Stock. The investment case hinges on whether new product contributions can offset KEYTRUDA biosimilar pressure in the early 2030s while margins hold or expand.

Thesis Intact

- WINREVAIR at a $525M quarterly run rate with Phase III expansion potential into a new pulmonary hypertension indication that currently has no approved therapies

- I-DXd priority review with a PDUFA date of October 10; WELIREG PDUFA dates of June 19 and October 4 represent near-term binary catalysts

- Mid-case net income margin of 33% is achievable if SG&A leverage materializes as the launch cycle matures past peak investment

Thesis at Risk

- Revenue CAGR of 0.5% in the mid-case reflects near-zero growth expectations, leaving no room for GARDASIL to deteriorate further or KEYTRUDA timing headwinds to compound

- The low-case scenario prices Merck stock at $127, just 13% above current levels over 4.7 years, a 1.5% annualized return that makes the risk/reward unattractive if pipeline execution slips

- Terns acquisition adds ~$2.35/share in one-time charges with TERN-701 still in early-phase development, diluting near-term EPS before any commercial contribution

Should You Invest in Merck & Co., Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MRK stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Merck & Co., Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MRK stock on TIKR for Free →