Key Takeaways

- DoorDash stock is the higher-conviction growth bet; Uber stock is the scaled cash compounder, and the data draws a clean line between the two.

- TIKR’s valuation model targets DoorDash stock at a 39.0% IRR, with consensus revenue growth of 29.6% in 2026 more than doubling Uber’s 12.2%.

- Uber generated $9.8B in free cash flow in 2025, growing 41.6% year-on-year, a cash generation gap that no delivery-first platform can close in the near term.

DASH | DoorDash, Inc.

- Current Price: $154.55

- 52-Week Range: $143.30 – $285.50

- Market Cap: $69.8B

- Enterprise Value: $67.6B

- Analyst Mean Target: $253.70

- Analyst Consensus: 27 Buys, 9 Outperforms, 9 Holds

UBER | Uber Technologies, Inc.

- Current Price: $71.81

- 52-Week Range: $68.46 – $101.99

- Market Cap: $147.4B

- Enterprise Value: $148.5B

- Analyst Mean Target: $103.58

- Analyst Consensus: 36 Buys, 10 Outperforms, 8 Holds, 1 Sell

The Business Case

DoorDash (DASH) is the dominant U.S. food delivery platform that has spent the last two years methodically expanding beyond restaurants, now commanding the leading third-party position in U.S. grocery and retail delivery while simultaneously building an international footprint through the Wolt and Deliveroo acquisitions, a business in the early stages of becoming what CEO Tony Xu calls the operating system for local commerce.

Uber Technologies (UBER) operates a fundamentally different structure: a diversified platform spanning ride-hailing, food and grocery delivery through Uber Eats, and freight, serving over 202 million monthly active users across 75 countries in mobility and 32 in delivery, making it a cross-platform network where 40% of consumers already use more than one Uber product, generating 3x the gross bookings of single-service users.

The distinction matters for how each is valued. DoorDash is a purer, faster-growing delivery compounder with a cleaner balance sheet and wider gross margins. Uber is the scaled, diversified platform throwing off nearly $10 billion in annual free cash flow today, with structural advantages in cross-platform retention and international density that no pure-play delivery company can replicate.

Both companies are investing aggressively into autonomous delivery, grocery expansion, and advertising, but they are doing it from different starting points, with different margin profiles, and at different growth rates. That gap is precisely where Wall Street’s preferences diverge.

Wall Street’s Take: Who Does the Street Favor on Growth and Margin Trajectory?

The investment debate between DoorDash stock and Uber stock ultimately comes down to one question: which company is further from its earnings ceiling?

On that measure, the Street’s math points clearly toward DoorDash.

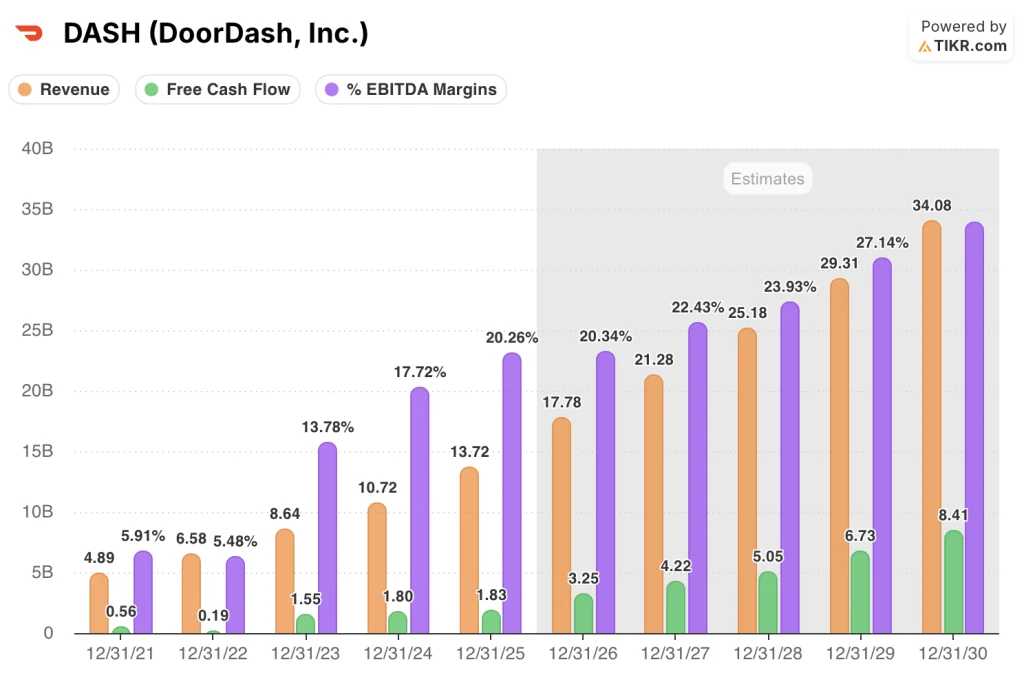

Consensus estimates show DoorDash revenue accelerating to $17.8B in 2026, representing 29.6% growth, and compounding toward $34.1B by 2030.

EBITDA margins are forecast to expand from 20.3% in 2025 to 29.7% by 2030, a trajectory anchored by the Deliveroo integration, the maturing new verticals business, and the global tech replatforming Ravi Inukonda confirmed is primarily completing in 2026.

Free cash flow, at $1.8B in 2025, is expected to more than double to $3.3B by 2026 as new verticals approach gross profit positive in the second half and international contribution profit turns positive.

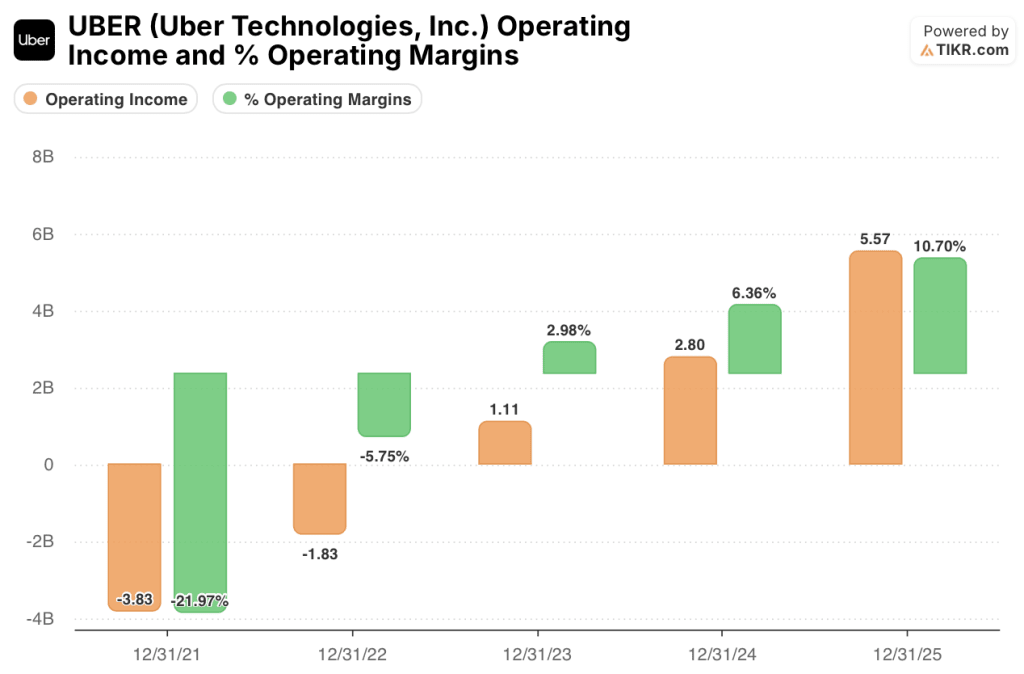

Uber stock tells a different but equally compelling story, one built at a more mature growth rate. Consensus expects UBER revenue of $58.4B in 2026, growing 12.2%, scaling to $89.1B by 2030.

EBITDA is forecast at $11.0B in 2026 (18.9% margin), rising to $20.0B by 2030 at a 22.5% margin.

The FCF profile is where Uber’s platform advantage shows up most clearly: $9.8B generated in 2025, growing 41.6% year-on-year, and expected to reach $17.7B by 2030.

Uber is already a free cash flow machine. DoorDash is on its way to becoming one.

The analyst community reflects this. Of 45 analysts covering DASH, 27 rate it a Buy and 9 Outperform, with a mean target of $253.70 implying 64.2% upside from the April 9 close of $154.55. The Street high sits at $340.00.

Meanwhile, of 56 analysts covering UBER, 36 rate it a Buy and 10 Outperform, with a mean target of $103.58 implying 44.2% upside from $71.81.

Both stocks carry strong conviction, but the implied upside differential is telling: analysts are pricing in structurally more room to run in DoorDash stock.

Trading at a meaningful discount to its consensus target, DASH offers the larger implied return precisely because the Street believes the Deliveroo acquisition, the new verticals profitability inflection, and the global tech consolidation are not yet reflected in the share price. UBER’s discount is narrower, consistent with a platform the market already recognizes as a free cash flow compounder but is still repricing after the 2025 multiple compression.

The risk in DoorDash stock is execution: three tech stacks being consolidated into one is expensive, with Ravi Inukonda guiding that the elevated spend will pressure Q1 EBITDA before the second-half ramp.

The risk in Uber stock is competitive displacement in top cities from first-party AV deployments, though Balaji Krishnamurthy noted that 75% of U.S. mobility profits already come from non-top-20 markets where AV penetration remains years away.

The catalyst to watch in DASH: new verticals gross profit contribution turning positive in the second half of 2026, which Ravi Inukonda flagged as a threshold event for demonstrating that the grocery and retail expansion is not just growing but durable.

In UBER: the rate at which Uber One membership (46 million strong and growing 55% year-on-year) converts single-product users into multi-service customers, which directly drives the 3x gross bookings multiplier CFO Balaji Krishnamurthy described.

Financials: The Profitability Race

The income statement comparison between DoorDash and Uber reveals two companies at very different stages of the same journey: both turned profitable, both expanding margins, but with a 13-point gross margin gap that explains much of the valuation divergence.

DoorDash gross margins expanded from 48.2% in 2023 to 51.8% in 2025, while operating income swung from a $(0.58)B loss in 2023 to $0.84B in 2025 at a 6.1% operating margin, a 1,517.3% improvement year-on-year that reflects the operating leverage finally emerging from years of platform investment. Revenue grew 27.9% in 2025 to $13.7B, with gross profit rising 34.2% to $7.1B, demonstrating that DoorDash is scaling revenue faster than costs.

Meanwhile, Uber’s income statement tells the story of a business that crossed the profitability threshold earlier but at structurally thinner gross margins.

Also, gross margins of 38.5% in 2025, against DoorDash’s 51.8%, reflect Uber’s diversified cost structure across mobility, delivery, and freight.

Operating income reached $5.57B in 2025 at a 10.7% margin, almost doubling year-on-year, with revenue of $52.0B growing 18.3%. The trajectory is strong, but the starting point in margins is lower.

The gap matters most in the long-term margin expansion story. DoorDash, beginning from higher gross margins, has more structural room to convert incremental revenue into EBITDA as fixed costs are absorbed across a growing order base.

Uber’s operating leverage is real, with operating income growing 98.8% in 2025, but the gross margin ceiling is lower, which is why consensus EBITDA margins converge in the high 20s for DoorDash and the low 20s for Uber by 2030.

What TIKR’s Valuation Model Says

TIKR’s model on DoorDash stock surfaces the most striking number in this comparison: a mid-case price target of $734.78 by December 2030, implying a 375.4% total return from the current price of $154.55 and an annualized IRR of 39.0%. That output is built on a 19.3% revenue CAGR assumption through 2031 and a net income margin of 30.1%, both grounded in the Deliveroo integration delivering on its $200M EBITDA 2026 contribution, new verticals turning gross profit positive, and the global tech stack consolidation removing the redundant cost of running three parallel systems.

DASH appears significantly undervalued at current levels, with even the low-case scenario at $532.83 representing a 244.8% return, implying the market has not yet priced in a base case where DoorDash simply executes on the operational roadmap it has already laid out.

TIKR’s model on Uber stock produces a mid-case target of $196.77 by December 2030, a 174.0% total return at a 23.7% IRR, on a 10.9% revenue CAGR and 15.8% net income margin assumption. The low case at $152.24 still implies a 112.0% return from today’s price.

UBER appears undervalued at current levels, but the model makes clear that Uber’s investment case is defined by scale and cash generation rather than growth rate. The IRR gap between DASH (39.0%) and UBER (23.7%) in the mid case is not a knock on Uber; it is a mathematical consequence of DoorDash’s faster growth assumption, wider margin expansion potential, and lower current valuation relative to its earnings trajectory.

The central tension in this comparison is this: DoorDash is the higher-conviction growth bet, where the margin and revenue expansion story is still early and the upside in the TIKR model is substantially larger. Uber is the lower-risk, already-scaled compounder, generating more absolute cash today than DoorDash will generate for several years, with a membership ecosystem and cross-platform advantage that gets more durable every quarter.

The Case for DoorDash Stock

- 29.6% consensus revenue growth in 2026 against Uber’s 12.2%, with EBITDA margins forecast to reach 29.7% by 2030 versus Uber’s 22.5%

- Deliveroo growing faster than pre-acquisition expectations at the same profit contribution, with Tony Xu confirming share gains in its largest markets and faster growth internationally than in the U.S.

- New verticals (grocery, retail) moving toward gross profit positive in 2H 2026, unlocking the next leg of margin expansion

- Net cash position of $2.2B versus Uber’s near-zero net debt, providing balance sheet optionality during the tech replatforming year

- TIKR mid-case IRR of 39.0% versus Uber’s 23.7%, with the largest implied upside gap in the Street target-to-price ratio (164.2% vs 144.2%)

The Case for Uber Stock

- $9.8B in 2025 free cash flow growing at 41.6% year-on-year, compared to DoorDash’s $1.8B; the absolute cash gap is a structural platform advantage, not a temporary one

- 202 million monthly active users across 75 mobility markets and 32 delivery markets, with 40% of consumers already cross-platform, generating 3x gross bookings per user versus single-service customers

- AV strategy diversified across Waymo, NVIDIA, Waabi, WeRide, Baidu and Pony, targeting 15 cities by end of 2026, with 75% of U.S. profits insulated in non-top-20 markets where AV displacement is years away

- Uber One membership at 46 million and growing 55%, the stickiest unit economics driver in the delivery sector, already approaching 50% of gross bookings from members

- $6B+ returned to shareholders in 2025, with Balaji Krishnamurthy confirming aggressive buybacks continue at current valuations

Should You Invest in DoorDash or Uber?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DASH stock and UBER stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down for both companies.

You can build a free watchlist to track DoorDash and Uber alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DASH stock or UBER stock on TIKR for Free →