Key Stats for Accenture Stock

- 52-Week Range: $177.5 to $325.7

- Current Price: $179.53

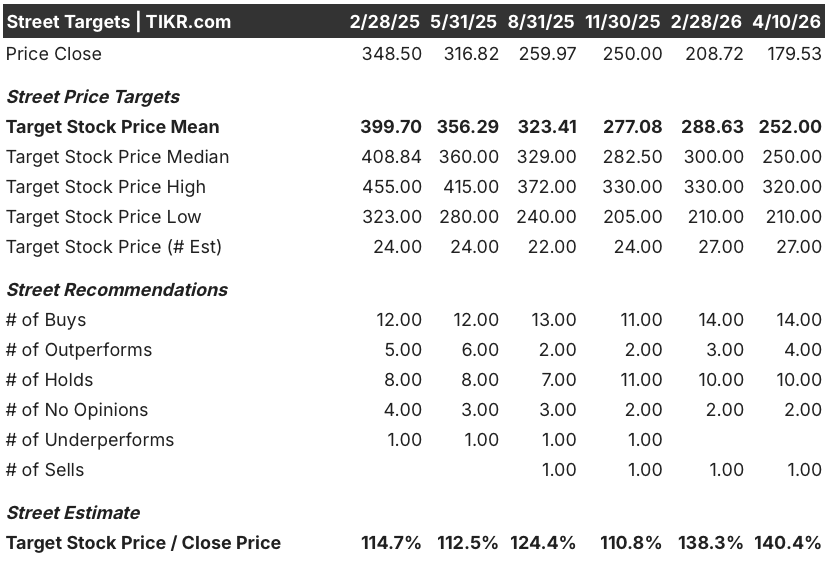

- Street Mean Target: $252

- Street High Target: $320

- TIKR Model Target (Dec. 2030): $276.1

What Happened?

Accenture plc (ACN), the world’s largest IT consulting firm helping companies redesign their operations around artificial intelligence, posted record quarterly bookings of $22.1 billion in its Q2 fiscal 2026 earnings, even as Accenture stock trades near its lowest price in years on fears that AI will displace the very services it sells.

On March 19, the company reported Q2 revenue of $18.0 billion, up 8.3% year-over-year, beating analyst estimates of $17.84 billion, and raised its full-year free cash flow outlook to $10.8 billion to $11.5 billion, a $1 billion increase from prior guidance.

The record bookings included 41 clients with individual quarterly bookings exceeding $100 million each, 12 more than the same period last year, a figure that signals enterprise demand for large-scale AI transformation is accelerating rather than stalling despite the stock’s decline.

Julie Sweet, Chair and CEO, stated on the Q2 earnings call that “AI is permeating everything we do,” and that AI and data are “now central, sometimes as the destination and increasingly as part of the work from day 1,” linking the record bookings directly to clients building out foundational AI infrastructure with Accenture as the primary execution partner.

Over the next three to five years, Accenture’s competitive position rests on three named drivers: a $5 billion acquisition deployment plan targeting AI-native firms and data assets in fiscal 2026, a talent base already exceeding 85,000 AI and data professionals, and an ERP modernization wave across hundreds of enterprise clients whose systems were built before advanced AI existed, all of which management identified on the Q2 call as an expanding multi-year funnel of work.

Wall Street’s Take on ACN Stock

The Q2 results reframe the debate around Accenture stock from “will AI hurt its business” to “how fast will AI-driven reinvention become its largest revenue driver,” with record bookings and a $10.8 billion FCF floor suggesting the demand signal is already answering that question.

Accenture’s normalized EPS is projected at $13.88 for fiscal 2026, up 7.3% year-over-year, before accelerating to $14.93 in 2027 (+7.6%), with free cash flow expected to reach $11.27 billion in fiscal 2026 against the company’s commitment to return at least $9.3 billion to shareholders through dividends and buybacks, backed by record H1 bookings of $43 billion.

With 20 buys, 9 holds, and 1 sell among covering analysts, the Street is overwhelmingly constructive on Accenture stock, and the median price target of $275 implies 53% upside from current levels as Wall Street waits for the AI revenue acceleration thesis to show in consecutive quarters of double-digit growth.

The target spread from roughly $224 on the low end to above $325 captures a real debate: the bull case prices in ACN re-rating as an AI infrastructure layer at a multiple closer to its historical 18x forward earnings, while the low case reflects a scenario where AI efficiency tools compress project timelines faster than new work volume can replace the lost hours.

Priced at just 12.9x fiscal 2026 normalized EPS against a historical forward P/E of approximately 18x and with bookings growth accelerating for three consecutive quarters, Accenture stock appears undervalued relative to the strength of its current demand signal and the scale of the AI transformation opportunity ahead.

Wells Fargo upgraded Accenture to overweight on February 17, citing “increased confidence in fiscal H2 revenue growth acceleration” and noting shares had been “excessively punished” due to AI disruption fears spilling over from broader software sector sentiment.

If enterprise AI spending stalls or if AI coding tools compress systems integration project timelines materially faster than new work volumes can offset, Accenture’s revenue growth trajectory from its current 4% to 6% local currency guide faces real downside.

The Q3 fiscal 2026 earnings report is the event to watch: revenue in the $18.35 billion to $19.0 billion range confirms H2 acceleration and validates the bull case, while a miss against the midpoint of $18.68 billion would reignite AI disruption fears at a stock already trading near 52-week lows.

Accenture Stock Financials

Accenture’s revenue has compounded at a steady pace across five fiscal years, growing from $50.5 billion in fiscal 2021 to $69.7 billion in fiscal 2025, with the most recent year delivering 7.4% growth as AI-driven consulting demand outpaced prior years’ 1.2% growth in fiscal 2024.

Gross profit grew from $16.4 billion to $22.2 billion over the same period, with gross margins holding remarkably stable in the 31.9% to 32.6% band, reflecting the pricing discipline of a firm that has consistently passed content and talent cost increases through to clients without margin erosion.

Operating income reached $10.85 billion in fiscal 2025, up 8.9% year-over-year, with operating margins expanding from 15.1% in fiscal 2021 to 15.6% last year, a trajectory that the LTM figure of 15.7% confirms is continuing into the current fiscal year as AI-related engagements carry higher fixed-price contract structures.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $276.06 is built on a 6.8% EPS CAGR through fiscal 2030 and a net income margin expansion from 11.7% today to 12.0%, assumptions anchored to Accenture’s current trajectory of record bookings, $5 billion in annual acquisition investment targeting higher-margin AI-native capabilities, and an enterprise ERP modernization cycle that management called “still very early” on the Q2 call.

ACN appears undervalued at current levels, trading at 12.9x fiscal 2026 normalized EPS against a historical forward multiple closer to 18x, with the TIKR mid-case implying 53.8% total return to $276.06 at a 10.3% annualized IRR over the next 4.4 years.

The question is not whether Accenture’s AI opportunity is real: $22.1 billion in quarterly bookings and 85,000 AI professionals on staff answer that. The question is whether multiple compression from AI disruption fears is temporary or structural.

Low Case: $224.08 (24.8% total return, 5.2% IRR)

- Revenue CAGR of 4.9% through fiscal 2030, below ACN’s 5-year historical average of 9.5%, reflecting a scenario where AI coding tools and automation compress consulting project scope faster than new AI transformation work can replace it

- Net income margin holds at 11.2%, slightly below the current 11.7%, as pricing pressure on legacy managed services offsets gains in higher-margin AI advisory work

- EPS CAGR of 4.9% with P/E multiple contracting 10.3% annually, implying the market re-rates Accenture as a slower-growth, labor-intensive business rather than an AI infrastructure enabler

- Even in this scenario, the stock generates 24.8% total return from current levels, indicating the downside is well-contained at a starting valuation of 12.9x earnings

Mid Case: $276.06 (53.8% total return, 10.3% IRR)

- Revenue CAGR of 5.5%, consistent with Accenture’s current fiscal 2026 guidance of 4% to 6% in local currency and the expectation that AI transformation engagements expand in scope as enterprise clients move from proof of concept to full production deployment

- Net income margin expands to 12.0%, driven by a rising mix of fixed-price AI contracts (already over 60% of bookings in fiscal 2025) and higher-margin acquisitions like Faculty and Ookla that contribute subscription and licensing revenue outside the traditional FTE billing model

- EPS CAGR of 6.8% with P/E multiple contracting 8.4% annually, a conservative assumption that still prices in meaningful re-rating as the AI thesis converts to visible earnings growth

- The $5 billion acquisition budget, if deployed into assets with Ookla-style economics (431 employees, $231 million revenue, subscription-based), accelerates the non-FTE revenue mix shift that underpins margin expansion

High Case: $328.13 (82.8% total return, 14.7% IRR)

- Revenue CAGR of 6.0% paired with net income margin reaching 12.6%, driven by the Agentic commerce opportunity Julie Sweet flagged as surging demand, the mainframe modernization wave AI is now making economically viable, and the ERP re-modernization cycle across hundreds of existing enterprise clients

- EPS CAGR of 8.3% with multiple contraction of only 6.6% annually, implying the market re-rates ACN closer to its historical 18x earnings multiple as AI revenues become a visibly distinct and faster-growing segment

- The high case essentially asks: what if record bookings keep compounding? Three consecutive quarters of $20 billion or more in bookings, rising to $22.1 billion in Q2, suggest the answer is already taking shape

Should You Invest in Accenture plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ACN stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Accenture plc alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ACN stock on TIKR for Free →