Key Stats for Alamo Stock

- 52-Week Range: $156.3 to $233.3

- Current Price: $176.9

- Street Mean Target: $207.4

- Street High Target: $225

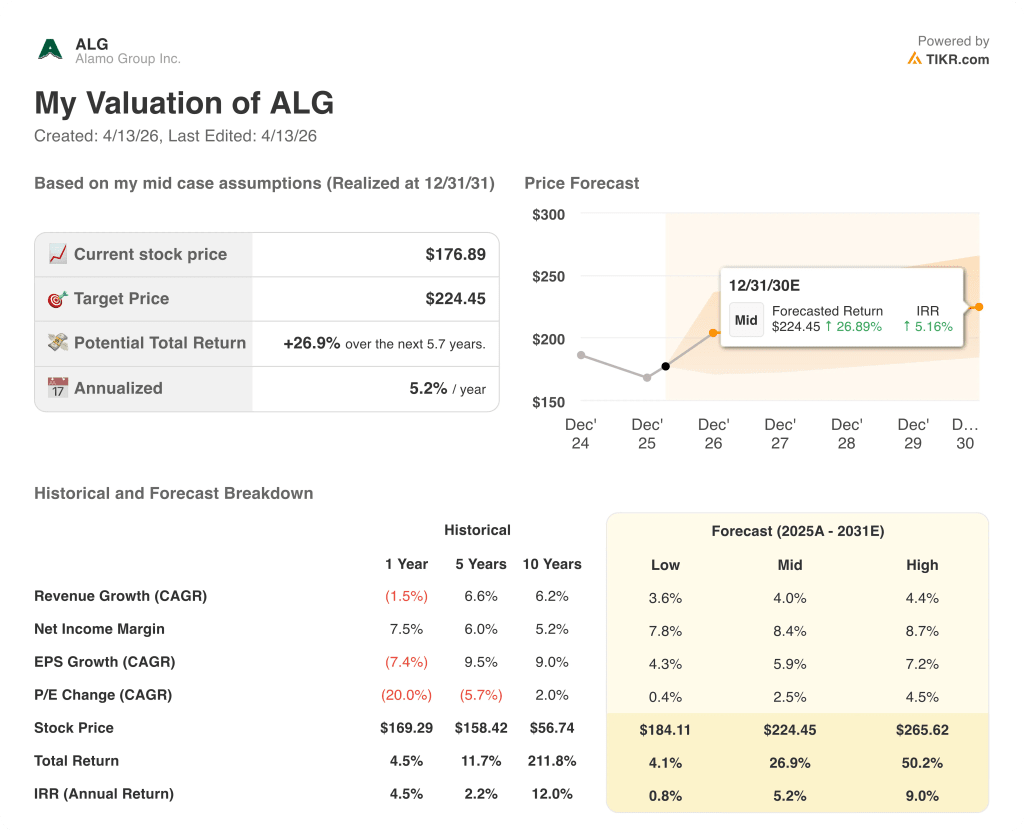

- TIKR Model Target (Dec. 2030): $224.5

What Happened?

Alamo Group stock (ALG), one of North America’s largest manufacturers of industrial and vegetation management equipment serving government infrastructure, utility, and agricultural markets, is rebuilding its margin story after two difficult years, with new CEO Robert Hureau outlining a long-term target of 15% adjusted operating margins tied to a four-pillar strategic overhaul.

Q4 2025 net sales came in at $373.7 million, down 3% year over year and below the $399.6 million analyst consensus, as weakness in tree care and municipal mowing dragged the Vegetation Management division’s revenue down 13.2% to $138.7 million.

The Industrial Equipment division told a different story: Q4 net sales grew 4.2% to $234.9 million, and adjusted EBITDA margins expanded to 17.7%, up from 15.7% in the prior year period, demonstrating what the business looks like when end markets cooperate.

Robert Hureau, President and CEO, stated on the Q4 2025 earnings call that “I am more confident and excited today about where we expect to take this company over the next 3 to 5 years than I was when I joined just a short time ago,” anchoring a strategic framework built on commercial excellence, operational efficiency, and targeted tuck-in acquisitions.

In January 2026, Alamo Group completed the acquisition of Petersen Industries, a manufacturer of truck-mounted grapple loader equipment for municipal waste customers, funded with a $120 million revolver draw and $50 million in cash, expanding the Industrial Equipment division’s footprint in a segment management described as a high-margin growth end market.

The path to 15% adjusted operating margins runs through two parallel tracks: stabilizing Vegetation Management volumes after eight consecutive quarters of double-digit declines, and extending Industrial Equipment’s margin leadership through procurement efficiencies, manufacturing consolidations, and next-generation product launches including a proprietary hybrid sweeper that can run on diesel, CNG, or electric chassis.

Wall Street’s Take on ALG Stock

Eight consecutive quarters of Vegetation Management declines have masked what Industrial Equipment is quietly delivering: 59% of total net sales, growing revenue, and a forward EPS recovery that Alamo Group stock at $176.89 has not yet priced in.

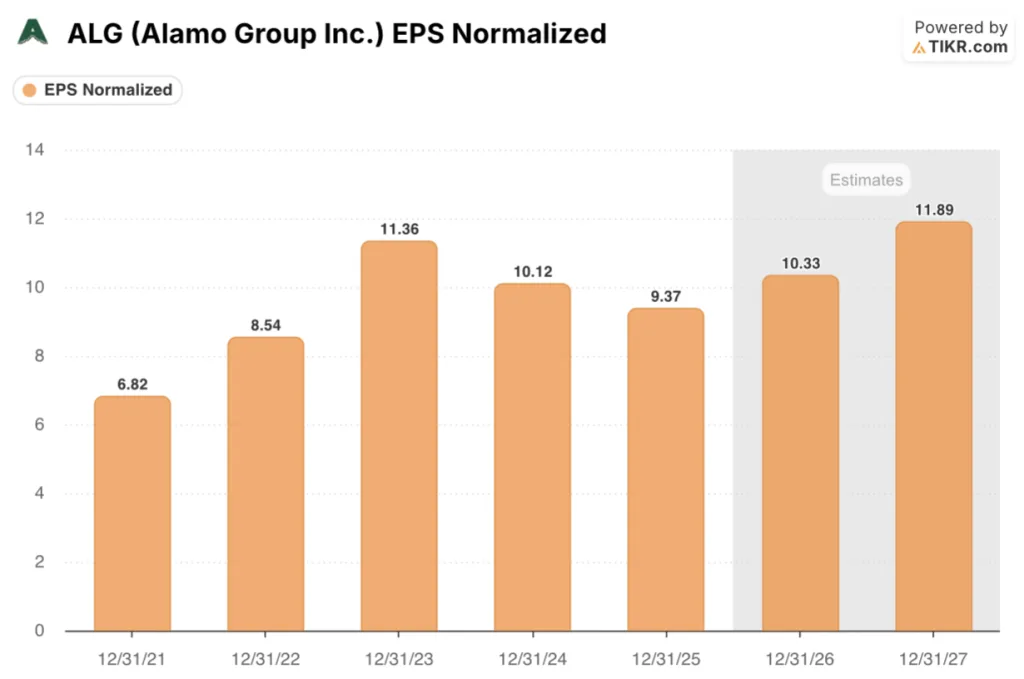

ALG’s normalized EPS is forecast to recover from $9.37 in FY25 to $10.33 in FY26 (up 10.3%) and $11.89 in FY27 (up 15.1%), supported by the Petersen Industries acquisition contributing roughly 11 months of revenue in 2026 and manufacturing consolidations already delivering results in the snow and sweeper businesses.

Five analysts cover Alamo Group stock, with 2 buys, 1 outperform, and 1 hold: the mean price target stands at $207.40, implying 17.2% upside from the current $176.89, and William Blair initiated with an outperform rating in March, the first new coverage initiation in at least a year.

The $190 to $225 target spread reflects a genuine debate about Vegetation Management recovery pace, with the bull case anchored to management’s 8% adjusted operating margin roadmap as a near-term floor and the bear case citing sustained weakness in tree care and municipal mowing into early 2026.

Priced at roughly 17.1x FY26E normalized EPS of $10.33, against a recent NTM P/E of 19x when the business was generating weaker earnings, and with the EPS growth trajectory accelerating to 15.1% in FY27, Alamo Group stock appears undervalued given the margin expansion potential that Vegetation Management’s two-year drag has temporarily concealed.

If tariffs escalate further and tree care or municipal mowing demand deteriorates beyond current expectations, the Vegetation Management recovery stalls and Hureau’s 15% operating margin target shifts from near-term milestone to multi-year stretch goal.

Q1 2026 Vegetation Management revenue is the specific number to watch: management guided for sequential top-line improvement from Q4’s $138.7 million, and whether orders in tree care and municipal mowing stabilize will confirm or deny whether the 8% adjusted operating margin floor is achievable by mid-2026.

Alamo Group Stock Financials

Alamo Group’s revenues peaked at $1.69 billion in FY23 and have contracted for two consecutive years, falling to $1.60 billion in FY25, a cumulative 5.3% pullback driven entirely by Vegetation Management’s end-market softness while Industrial Equipment continued to expand.

Gross margins compressed from a FY23 peak of 26.8% to 24.8% in FY25 as Vegetation Management’s volume decline created inverse leverage on fixed manufacturing costs, with Q4 charges for slow-moving inventory reserves in tree care and municipal mowing product lines accelerating the compression.

ALG’s operating income fell from $0.20 billion in FY23 to $0.15 billion in FY25, an 8.0% year-over-year decline in FY25, yet the operating margin held at 9.5% against a backdrop of meaningful revenue contraction, reflecting the cost discipline and fixed-cost reduction that manufacturing consolidations in the Industrial Equipment division have already contributed.

What Does the Valuation Model Say?

The TIKR model prices ALG at $224.45 on mid-case assumptions embedding 4.0% revenue CAGR through 2031 and a net income margin recovery to 8.4%, assumptions that directly reflect Hureau’s four-pillar strategy, Petersen Industries’ above-average margin contribution, and the procurement and manufacturing efficiencies already underway across both divisions.

ALG appears undervalued at current levels, with the TIKR mid case pointing to $224.45 by December 2030 and an annualized IRR of 5.2%, a return that rises to 9.0% on the high case as Vegetation Management margins recover and re-rating follows.

The entire investment case hinges on whether Vegetation Management stabilizes in 2026 while Industrial Equipment sustains its margin leadership, because those two things happening simultaneously is what unlocks Hureau’s 15% operating margin roadmap.

What Has to Go Right

- Vegetation Management adjusted operating margins recover toward the 8% level achieved in H1 2025, driven by manufacturing consolidation in two facilities expected to normalize by Q2 2026 as production inefficiencies resolve

- U.S. and European agriculture orders, which turned positive year over year in Q4 2025 for the first time in eight quarters, sustain through 2026 and reduce Vegetation Management’s reliance on the more cyclical tree care and municipal mowing segments

- Petersen Industries, acquired for roughly $170 million in January 2026, contributes above-Alamo-average adjusted EBITDA margins across a full year of revenue, with commercial synergies from Alamo’s channel network building through H2 2026

- The next-generation hybrid sweeper, in final testing as of March 2026, launches commercially and reinforces the Industrial Equipment division’s shift from fast follower to first mover, supporting its backlog of roughly $400 million entering 2026

What Could Go Wrong

- Municipal mowing end-market weakness persists beyond Q1 2026 as state DOTs delay capital orders in response to federal funding uncertainty tied to Infrastructure Investment Act renewal debates, directly suppressing Vegetation Management volumes and margins

- Tree care demand stays depressed as housing starts remain suppressed, keeping large-format land-clearing equipment below replacement cycle levels and triggering additional inventory reserves similar to the charges taken in Q4 2025

- Tariff-driven input cost escalation offsets the global procurement initiative savings, compressing gross margins further from FY25’s already multi-year low of 24.8%

- Industrial Equipment top-line growth slows to the guided flat-to-low-single-digit range as Alamo Group intentionally pulls back from low-margin snow business, narrowing the contribution that can offset Vegetation Management’s continued drag on consolidated earnings

Should You Invest in Alamo Group Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ALG stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Alamo Group Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ALG stock on TIKR for Free →