Key Stats for Expedia Stock

- 52-Week Range: $144.2 to $303.8

- Current Price: $228.1

- Street Mean Target: $283

- Street High Target: $387

- TIKR Model Target (Dec. 2030): $464.4

What Happened?

Expedia Group (EXPE), the online travel platform operating Expedia.com, Hotels.com, and Vrbo across more than 200 countries, has fallen roughly 25% from its 52-week high even as the underlying business delivered its strongest operating results in years, with Expedia stock currently trading at $228.09 against a street mean target of $283.00.

The Q4 2025 earnings beat drove the most recent re-rating catalyst: adjusted EPS of $3.78 came in 12.5% above the $3.36 consensus estimate while revenue of $3.55 billion beat the $3.42 billion estimate, and adjusted EBITDA of $848 million outpaced expectations by 11.6%.

The engine behind that beat was B2B: Expedia’s business-to-business segment, which provides travel booking infrastructure to airlines, banks, and travel agencies, grew gross bookings 24% in Q4 versus just 5% in the direct-to-consumer unit, with B2B recording double-digit growth across all regions for the 18th consecutive quarter.

CEO Ariane Gorin stated on the Q4 2025 earnings call that “we accelerated both bookings and revenue growth and expanded margins by over 2 points,” adding that the company grew its lodging property count by more than 10% and saw “nearly 70% more properties participate in our Black Friday sale than ever before.”

Expedia’s path to sustained margin expansion over the next three to five years runs through three compounding forces: continued B2B growth powered by supply and partner flywheel dynamics, ongoing B2C marketing efficiency gains that CFO Scott Schenkel publicly committed to extending into 2026, and the company’s aggressive moves into AI-driven personalization and agentic browser integration that management believes will deepen direct traffic advantages rather than erode them.

Wall Street’s Take on EXPE Stock

The Q4 beat reframes the investment case for Expedia stock from a turnaround story into a margin compounding story: a business guiding 22% normalized EPS growth for 2026 on 7.6% revenue growth in 2025 is beginning to demonstrate the earnings acceleration that was once only visible on paper.

Expedia’s normalized EPS hit $15.86 in 2025, up 31.0% year over year, and consensus projects $19.35 for 2026 (up 22.0%) and $22.96 for 2027 (up 18.6%), each estimate grounded in the company’s publicly guided full-year gross bookings range of $127 billion to $129 billion and revenue of $15.6 billion to $16.0 billion, both above prior street consensus.

Fifteen of 39 analysts covering Expedia stock carry buy or outperform ratings, with a mean price target of $283.00 implying roughly 24% upside from current levels, while the hold-heavy consensus (23 holds) reflects an investor base that is waiting to see whether the geopolitical macro backdrop suppresses leisure travel demand before committing to a full re-rating.

The target spread is wide: $225 on the low end to $387 on the high end, a gap that maps directly to the AI disruption debate, specifically whether generative AI search experiences gradually disintermediate OTAs from travel discovery or become a new demand channel that Expedia captures through its early platform integrations with ChatGPT, Google AI overviews, and agentic browsers.

Priced at roughly 11.8x forward normalized EPS against a backdrop of 22% projected EPS growth and a three-year share count reduction of 22%, Expedia stock appears undervalued relative to the quality of its earnings growth trajectory, particularly given that Booking Holdings trades at a material premium for a lower near-term EPS growth rate.

The risk is specific: Jefferies and Truist have both flagged that the Iran-related geopolitical conflict and softening macro visibility could suppress leisure travel bookings, with Truist cutting its price target on April 6 and noting that the conflict could tilt summer demand toward domestic or shorter-haul trips rather than higher-value international bookings where Expedia is growing fastest.

The number to watch on May 7 is Q1 2026 gross bookings growth, specifically whether the company’s guided range of 10% to 12% holds as the booking window for summer travel reaches its peak in the face of macro uncertainty.

Expedia Stock Financials

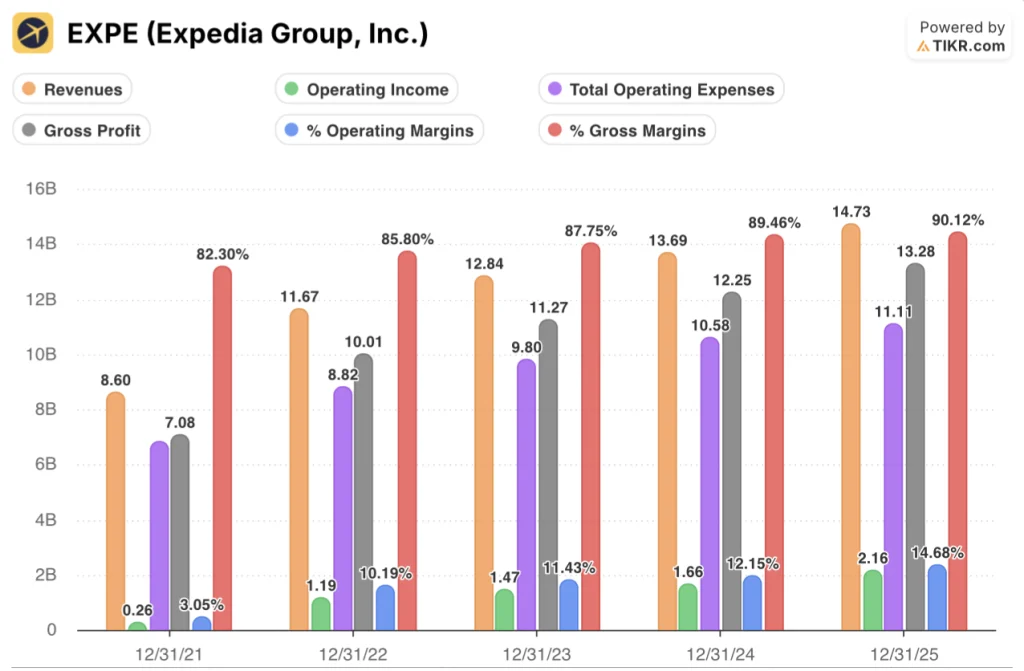

Expedia posted total revenues of $14.73 billion in 2025, up 7.6% year over year, but the headline growth rate understates the real story: operating income surged 30.0% to $2.16 billion, the fastest operating income growth rate since 2022, as the company stripped out cost while volumes grew.

Also, the operating leverage is mechanical and now structural: total operating expenses fell to $11.11 billion in 2025 from $10.58 billion in 2024, a 5% increase against 7.6% revenue growth, pushing the operating margin to 14.7%, up from 12.2% the prior year and nearly five times the 3.0% operating margin EXPE posted in 2021.

Gross profit also reached $13.28 billion in 2025, up 8.4% year over year, with gross margins expanding to 90.1% as Schenkel’s cloud cost discipline and the shift toward higher-margin B2B and advertising revenues reduced cost of goods sold for the second consecutive year despite total revenue growing by over $1 billion.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $464.43 by December 31, 2030 is built on a 6.4% revenue CAGR and a net income margin expanding to 18.2%, a combination that looks conservative against 2025 actuals: EXPE already delivered 13.8% net income margins that year while growing EPS 31%, and management has publicly committed to further margin expansion through 2026 and beyond.

EXPE appears undervalued at current levels, trading at roughly 11.8x forward EPS against a 22% near-term EPS growth rate, a multiple-to-growth discount that the TIKR model’s 16.2% annualized IRR to the mid-case target makes concrete.

The investment case hinges on a single question: does AI reshape the OTA demand funnel as a threat or as an opportunity, and if the answer is “opportunity,” how fast does EXPE’s direct traffic advantage compound against a backdrop of 22% EPS growth and aggressive buybacks?

What Has to Go Right:

- Q1 2026 gross bookings growth holds at 10% to 12% despite geopolitical headwinds, confirming the B2B flywheel is insulated from leisure travel softness

- B2B sustains double-digit growth through 2026, powered by the 18-consecutive-quarter streak of partner additions and new lines of business including the Tiqets acquisition (experiences) and the recently launched assurance products

- Agentic browser integrations with ChatGPT and Google convert into new demand rather than disintermediation, consistent with the March 5 report that OpenAI scaled back direct checkout ambitions

- Gross margins hold above 90% as cloud optimization and AI-driven customer service efficiency offset any marketing reinvestment, sustaining operating leverage toward the company’s unguided but implicit Booking Holdings-level margin target

What Could Go Wrong:

- Full-year gross bookings grow at the low end of guidance (6%), with the $127 billion floor reflecting continued macro softness in international bookings where EXPE grows fastest

- The Iran-related geopolitical disruption expands, pushing summer 2026 travelers toward short-haul domestic trips and structurally reducing average booking value

- Google AI Overview travel integrations or a competitive hotel chain AI booking push (Accor, Hyatt, and Best Western launched ChatGPT apps in February) materially erode Expedia’s metasearch and organic traffic share

- EBITDA margin expansion slows to the guided 100 to 125 basis point range for the full year, below investor expectations primed by Q1’s guided 300 to 400 basis point expansion, resetting multiples lower into May 7

Should You Invest in Expedia Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up EXPE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Expedia Group, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze EXPE stock on TIKR for Free →