Key Stats for Elastic Stock

- 52-Week Range: $42.3 to $96.1

- Current Price: $43.3

- Street Mean Target: $82.1

- Street High Target: $115

- TIKR Model Target (Dec. 2030): $67.8

What Happened?

Elastic N.V. (ESTC), a Search AI platform that helps enterprises feed accurate real-time context to large language models, is trading at $43.30 near a 52-week low of $42.05 despite sales-led subscription revenue accelerating to 21% year-over-year in Q3.

In the January quarter, Elastic posted revenue of $450 million, beating the $438.5 million consensus estimate, while non-GAAP EPS of $0.73 cleared the $0.65 estimate by 12.3% and lifted the full-year non-GAAP operating margin guide to 16.3%.

Current remaining performance obligations (CRPO, the revenue Elastic expects to recognize within the next 12 months) crossed $1 billion for the first time at $1.055 billion, up 19%, signaling durable enterprise commitment momentum across search, security, and observability.

On April 1, Elastic Cloud Hosted earned FedRAMP High authorization on AWS GovCloud (US), clearing ESTC to handle sensitive federal workloads including controlled unclassified information and expanding the footprint built through its existing CISA SIEM-as-a-service contract.

CEO Ash Kulkarni stated on the Q3 2026 earnings call that “the number of commitments for over $1 million in annual commitment value signed this quarter grew over 30% compared to the same period last year, driven by new logos and customer expansion,” directly linking record deal volume to the AI platform’s competitive displacement of legacy vendors.

A mid-calendar-year metrics data store launch, a $500 million buyback program 60% deployed, and a midterm target of 20%-plus sales-led subscription revenue growth by fiscal 2029 underpin Elastic’s case as the default context layer for enterprise AI infrastructure.

Wall Street’s Take on ESTC Stock

The Q3 earnings beat closed the book on lingering questions about Elastic’s go-to-market recovery: seven consecutive quarters of consistent field execution have now translated into accelerating sales-led subscription revenue, record large deal flow, and a current remaining performance obligation (CRPO, the revenue the company expects to recognize within the next 12 months) crossing $1 billion for the first time at $1.055 billion, up 19%.

ESTC’s normalized EPS is projected to reach $2.53 for the fiscal year ending April 2026, a 24% increase year-over-year, building on the 71.4% growth posted in FY2025, with the trajectory continuing to $2.83 in FY2027 (+11.9%) as the AI consumption uplift compounds across a widening base of $100,000 ACV customers now numbering more than 1,660.

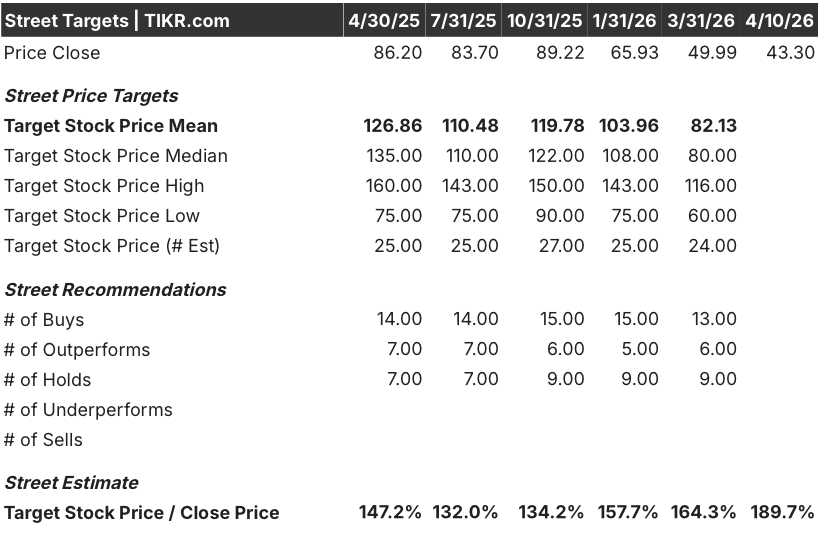

Nineteen analysts carry buy or outperform ratings on Elastic stock, against nine holds and zero sells, with a mean price target of $82.13, implying roughly 90% upside from the current $43.30 price — a spread that widened materially as the stock fell from $89 in October to near the 52-week floor, even as fundamentals improved.

The target range from $60 on the low end to $116 at the high reflects a real debate: bears anchor to decelerating constant-currency growth in Q4 guidance (guided at 13% versus Q3’s 16% print), while bulls point to RPO accelerating to 22% as evidence that consumption will catch up to commitments in the quarters ahead.

Trading at roughly 17x forward normalized EPS against a peer group of search and observability infrastructure players commanding 25x to 35x on similar or lower growth profiles, Elastic stock appears undervalued given accelerating sales-led subscription revenue, a record large-deal pipeline, and a FCF margin expanding toward 19% in FY2027.

The risk is Q4 consumption recognition: Elastic’s self-managed business generates large upfront commitments that convert to revenue over time, and three fewer billing days in the April quarter create a structural sequential headwind that, if compounded by slower-than-expected cloud consumption ramp, could keep the stock range-bound through the summer.

The catalyst is Q4 FY2026 earnings in late May, where the specific number to watch is sales-led subscription revenue versus the guided midpoint of $372 million; any print above $380 million would confirm that the AI consumption tailwind is running ahead of the company’s own risk-adjusted guidance.

Elastic Stock Financials

Elastic N.V.’s revenue grew from $0.6 billion in FY2021 to $1.7 billion LTM, with gross margins expanding from 73.8% to 76.1% over the same period, a 230-basis-point widening that reflects the platform mix shift toward higher-margin cloud and managed services.

The GAAP operating loss compressed from $(129.5) million in FY2021 to $(27.4) million LTM, with operating margin improving from -21.3% to -1.6%, as gross profit growth of 17.7% in FY2025 outpaced total operating expense growth of 9.3%.

R&D spending reached $421.8 million LTM, representing continued reinvestment in the vector search, inference, and agent-building capabilities behind ESTC’s competitive displacements of OpenSearch and legacy SIEM vendors referenced in Q3.

The tension in the income statement is real: SG&A of $870.2 million LTM keeps GAAP profitability out of reach this fiscal year, and any slowdown in revenue growth would compress the path to breakeven faster than the current trajectory implies.

What Does the Valuation Model Say?

The TIKR model prices Elastic stock at $67.77 on mid-case assumptions, a 12.7% revenue CAGR through April 2030 and net income margin expanding from 9.8% today to 15.3% at exit, a scenario grounded in the AI consumption uplift already visible in the $100,000 ACV cohort and the platform’s documented 6% revenue premium over non-AI customers.

ESTC appears undervalued at current levels, trading at $43.30 against a model-implied target of $67.77 representing a 56.5% total return, with even the bear case of 11.5% revenue CAGR producing a $52.96 price target, 22.3% above today’s price.

The central question in the Elastic investment case is not whether AI is a tailwind (28% of the $100,000 ACV cohort already uses ESTC for AI workloads, producing measurable consumption upside) but whether the pace of AI penetration among the remaining 72% accelerates fast enough to offset the deceleration in constant-currency growth visible in the Q4 guide.

What Has to Go Right:

- Sales-led subscription revenue holds at or above 18% constant currency through FY2027, consistent with four consecutive years of compounding at that level, as more of the 1,660+ enterprise customers adopt vector search and Agent Builder into production workflows

- The FedRAMP High authorization converts to material federal pipeline, building on the CISA SIEM-as-a-service contract that was pulling additional civilian agencies onto the platform in Q3

- The mid-year metrics data store launch closes the observability gap that Kulkarni explicitly called out as the one product-line headwind weighing on ESTC’s observability growth versus search and security

- FCF margin reaches 19.3% in FY2027 as consensus projects, supporting continued buyback activity from the remaining 40% of the $500 million repurchase program

What Could Go Wrong:

- Q4’s three-fewer-days headwind proves stickier than guided: if cloud consumption ramps slower than the $1.055 billion CRPO implies, FY2027 revenue growth could land closer to the bear case 11.5% CAGR rather than the mid case 12.7%

- The vector search efficiency gains Kulkarni acknowledged (two orders of magnitude RAM reduction over 18 months) continue acting as a revenue headwind as existing workloads cost customers less to run, keeping net expansion rate near the current 112% rather than accelerating

- The P/E multiple re-rating required to close the gap to the $82.13 mean analyst target demands 30x+ forward earnings assigned to a company still posting GAAP operating losses, a multiple contingent on execution consistency Elastic has delivered but the market has not yet rewarded

- Self-managed revenue strength, while operationally positive, complicates comparisons for investors using cloud revenue as their primary growth proxy, keeping ESTC misread relative to actual go-to-market momentum

Should You Invest in Elastic N.V.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ESTC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Elastic N.V. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ESTC stock on TIKR for Free →