Key Stats for CoStar Stock

- 52-Week Range: $35.8 to $97.4

- Current Price: $36.5

- Street Mean Target: $64.9

- Street High Target: $100

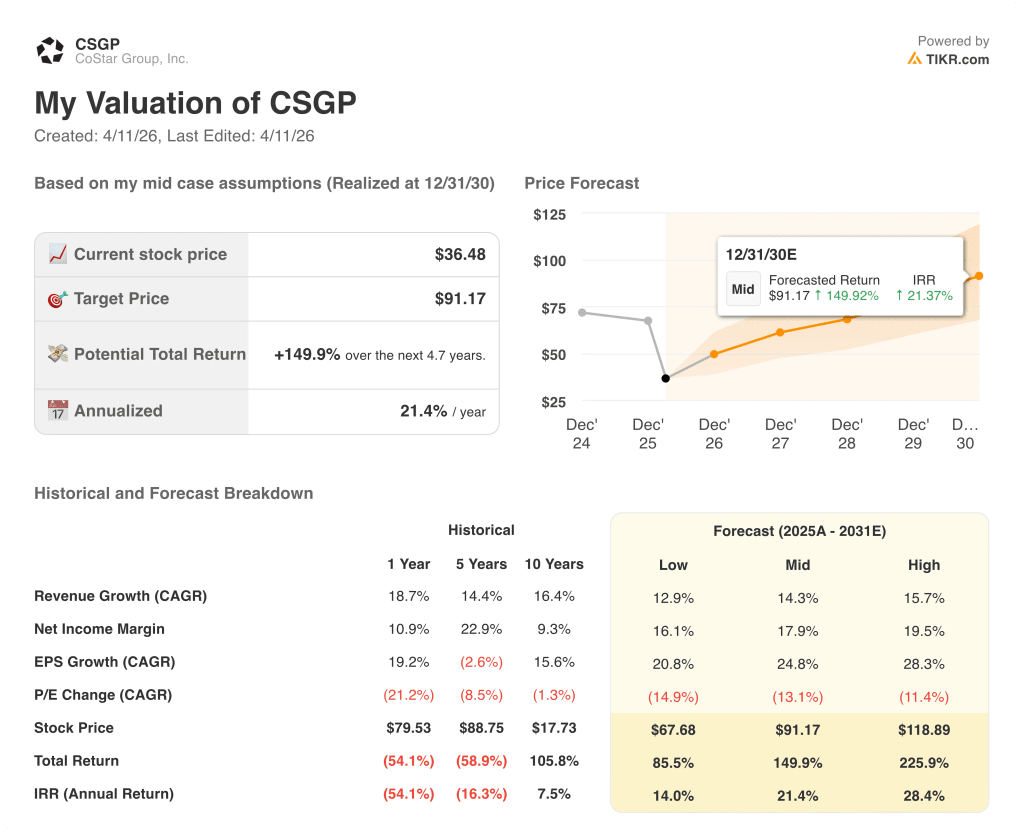

- TIKR Model Target (Dec. 2030): $91.2

What Happened?

CoStar Group (CSGP), the dominant provider of commercial real estate data and analytics that also operates Apartments.com and the fast-growing Homes.com residential marketplace, is trading near its 52-week low of $35.77 even as CoStar stock has delivered 59 consecutive quarters of double-digit revenue growth, most recently posting Q4 2025 revenue of $900 million, up 27% year-over-year.

The immediate catalyst for today’s pressure is billionaire activist Daniel Loeb’s Third Point hedge fund exiting its entire stake in CoStar, writing to investors that it “no longer believes that our original thesis holds true today” after concluding that CEO Andy Florance’s continued investment in Homes.com, the residential portal competing against Zillow, was a “reckless drain” on operating income.

Third Point’s exit follows a months-long proxy campaign that never materialized into a board fight: the fund had signaled plans to nominate directors in January 2026, watched CoStar stock fall from roughly $66 to $36.48, and ultimately walked away on April 10 without filing a single candidacy before the nomination deadline.

Andrew Florance, President and CEO, stated on the Q4 2025 earnings call that “with the heavy lifting of the Homes.com national brand launch behind us, we are entering a phase of significant EBITDA expansion,” pointing to full year 2026 adjusted EBITDA guidance of $740 million to $800 million, up from $442 million in 2025.

The data behind that expansion path is already visible: Homes.com reached 31,000 agent subscribers generating $100 million in annualized run-rate revenue as of Q4 2025, organic traffic jumped 134% year-over-year in January 2026, and the company launched Homes AI in February 2026, an AI-powered search interface that drove users to spend 16 minutes and 50 seconds on-site versus 4 minutes and 24 seconds for non-AI users, while generating 7x more email leads per session.

Wall Street’s Take on CSGP Stock

Third Point’s exit reframes the question investors need to answer: is Homes.com a value-destroying distraction that the data can no longer support, or is it a multi-year platform investment that the current price is catastrophically mispricing?

CSGP’s normalized EPS is estimated to reach $1.31 in 2026 and $1.78 in 2027, compounding at 35.5% year-over-year as EBITDA margins are guided to expand from 13.6% in 2025 to 20% to 21% in 2026 and toward 30%-plus by 2028 per consensus, all anchored in Florance’s explicit commitment to reduce Homes.com net investment by $300 million in 2026 and reach run-rate profitability by 2029.

Fifteen of 20 analysts covering CSGP carry a buy or outperform rating, with just 4 holds and 1 sell; the mean price target of $64.89 implies roughly 78% upside from the current price of $36.48, and the median target of $63.00 points to a consensus view that today’s stock price dramatically understates the value of the commercial data franchise alone.

The target spread from $40.00 to $100.00 maps the Homes.com debate precisely: the $40.00 low reflects a bear case where residential investment continues burning cash without achieving network effects, while the $100.00 high reflects a bull case where Homes.com replicates Apartments.com’s margin trajectory and scales toward Florance’s stated target of $4.75 billion in revenue and $2.85 billion in EBITDA within 13 years.

Trading at roughly 27.8x consensus 2026 normalized EPS of $1.31, with EPS expected to compound at 24.8% annually through 2030 per consensus, CoStar stock appears undervalued: the commercial segment alone, which generated $1.79 billion in revenue growing 18% in 2025 with peer-comparable margins, would justify a substantially higher multiple than the blended price the market is currently assigning to the combined business.

The commercial data franchise’s moat is independently durable: CoStar reached an all-time NPS of 70 in Q4 2025, its 94% renewal rate is the highest since 2022, CoStar Debt Solutions surpassed $100 million in annual run-rate revenue with a clear path to $1 billion, and a U.K. competitor, EG Radius, shut down entirely in December 2025 with CoStar onboarding 166 of their reported 150 clients.

The risk is direct: if Homes.com’s cash consumption extends beyond the 2029 run-rate profitability target that management has guided to, the credibility of the entire margin expansion thesis collapses, and CSGP could remain range-bound near current prices for years regardless of commercial segment performance.

Q1 2026 results on April 28 are the first real test of whether the EBITDA expansion glide path is on track: consensus expects Q1 adjusted EBITDA of $95 million to $115 million, and any shortfall after Third Point’s public exit would accelerate selling pressure.

CoStar Group’s Financials: What the Income Statement Reveals

CoStar Group’s revenue reached $3.25 billion in fiscal 2025, up 18.7% year-over-year, extending a decade-long compounding growth record even as operating income turned negative, swinging to a $(50) million loss versus $10 million in fiscal 2024 as SG&A expenses surged from $1.81 billion to $2.10 billion to fund the Homes.com national brand campaign and Matterport integration.

That operating loss is the number Third Point and D.E. Shaw seized on, and it is real: CSGP’s operating margin collapsed from 0.2% in fiscal 2024 to (1.7%) in fiscal 2025, but the compression is almost entirely driven by SG&A growth of $290 million in a single year, not by any deterioration in the gross margin structure of the underlying data business.

The gross margin story tells a different story from the operating line: CoStar Group maintained 78.9% gross margins in fiscal 2025, essentially flat with 79.6% in fiscal 2024, reflecting a business where the incremental cost of adding a new data subscriber remains structurally low and pricing power in commercial data has held despite competitive pressure.

The forward tension is clear from the trajectory: gross profit grew from $2.18 billion in fiscal 2024 to $2.56 billion in fiscal 2025, a 17.6% increase that outpaced revenue growth, yet that gross profit expansion was entirely consumed by the SG&A investment in Homes.com, meaning the thesis hinges entirely on whether that investment converts into the margin expansion management has guided for in 2026 and beyond.

What Does the Valuation Model Say?

The TIKR mid-case model prices CoStar Group at $91.17 by December 2030, embedding a 14.3% revenue CAGR from 2025 through 2031, a net income margin expanding to 17.9%, and an EPS CAGR of 24.8%, inputs that reflect the explicit guidance Florance provided for $740 million to $800 million in EBITDA in 2026 and the 5-percentage-point quarterly margin expansion the CFO committed to on the Q4 2025 earnings call

CSGP appears undervalued at current levels, trading at $36.48 against a mid-case model target of $91.17 that implies 149.9% total return and a 21.4% annualized IRR over 4.7 years, with the gap almost entirely explained by the market pricing Homes.com as a permanent drag rather than a time-limited investment.

The central tension in the CoStar Group investment case is straightforward: the stock is priced as if Homes.com spending never ends, while management’s own guidance says the investment glide path ends with full-year profitability in 2030 and run-rate profitability as early as 2029.

Bear Case ($67.68 by 2030 | 12.9% revenue CAGR | 85.5% total return)

- Homes.com fails to convert its 31,000 agent subscribers and 108 million monthly unique visitors into self-sustaining revenue growth, requiring continued heavy investment beyond 2026 and delaying run-rate profitability past 2029

- Third Point’s public exit accelerates institutional selling, compressing the forward multiple further as CSGP’s EBITDA expansion lags the 5-percentage-point quarterly improvement CFO Chris Lown committed to

- CoStar Group’s Q1 2026 EBITDA of $95 million to $115 million comes in at the low end or misses, validating activist concerns and reinforcing bearish sentiment through the proxy season

- Homes AI engagement metrics (16 minutes on-site, 7x email leads) fail to translate into subscriber growth at scale, and the traffic advantage over Zillow’s rental network narrows faster than expected

- CREXi antitrust counterclaims, allowed to proceed by the Supreme Court in March 2026, create legal overhang that distracts management and surfaces incremental litigation costs

Bull Case ($118.89 by 2030 | 15.7% revenue CAGP | 225.9% total return)

- Homes.com replicates Apartments.com’s growth trajectory: Apartments.com reached $1.25 billion in revenue at approximately 67% brand awareness after 13 years; Homes.com is tracking similar metrics in under 2 years, with January 2026 organic traffic up 134% year-over-year and session duration growing from 3 minutes 36 seconds to 4 minutes 33 seconds year-over-year

- The commercial segment accelerates independently: CoStar Debt Solutions, already above $100 million in annual run-rate revenue, grows toward the $1 billion opportunity management has outlined as origination workflow modules launch in Q1 2027 and lease benchmarking launches in Q2 2026

- LoopNet international expansion into Australia and Germany in 2026, combined with a 43% salesforce increase to 257 reps, drives LoopNet revenue well above its 17% Q4 2025 growth rate

- Homes AI converts its engagement advantage into accelerating agent subscriber growth well past the current 31,000 base, with the personalization capability the CFO described (remembering school zones, preferences, and buyer journeys) creating a switching cost that Zillow cannot replicate quickly

- The $700 million 2026 share repurchase program, executed at near-52-week-low prices, meaningfully reduces share count and lifts per-share EPS toward the high end of consensus estimates

Should You Invest in CoStar Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CoStar Group, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CSGP alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CSGP stock on TIKR for Free →