Key Stats for New Corp Stock

- 52-Week Range: $22.2 to $31.6

- Current Price: $24.6

- Street Mean Target: $34.1

- Street High Target: $41

- TIKR Model Target (Dec. 2030): $30.3

What Happened?

News Corporation (NWSA), the diversified media and information company behind The Wall Street Journal, Dow Jones, and Realtor.com, is trading near its 52-week low at $24.59 even as its highest-value business posts the strongest quarterly revenue growth in nearly three years.

News Corp stock has fallen roughly 16% over the past year despite the company reporting accelerating earnings momentum, a contradiction that defines the investment case today.

The February earnings report delivered the clearest evidence of that gap. News Corp posted Q2 fiscal 2026 revenue of $2.36 billion, beating analyst estimates of $2.29 billion, with adjusted EPS of $0.40 clearing the $0.34 consensus by nearly 18%.

The Dow Jones segment, which houses The Wall Street Journal, Barron’s, and MarketWatch alongside its B2B risk and energy data businesses, drove the beat with revenue up 8% and segment EBITDA up 10% to a record quarterly margin of nearly 30%. That marked the fourth consecutive quarter of double-digit EBITDA growth for the segment.

The engine behind that margin expansion is the Professional Information Business, Dow Jones’s B2B division serving financial institutions and corporations with compliance data, energy pricing benchmarks, and geopolitical intelligence.

Professional Information revenue grew 12% year over year in Q2, with Risk and Compliance revenues surging 20% to $96 million on new customer additions, new products, and higher yields. This is the business the market feared AI would disintermediate. The Q2 data argues the opposite.

On the Q2 earnings call, CEO Robert Thomson stated: “The Dow Jones team has successfully secured a significant increase in enterprise customers, where we are incorporating WSJ content into the workstreams of companies.” That shift matters because enterprise deals carry lower churn, minimal acquisition costs, and margin profiles that Thomson called “accretive” relative to direct consumer subscriptions.

Three concurrent developments extend the runway significantly. News Corp signed an AI content licensing deal with Meta worth up to $50 million per year, running for at least three years, following its earlier partnership with OpenAI.

Separately, Anthropic agreed to pay $1.5 billion to settle a lawsuit over illicit use of publishers’ books, with HarperCollins management expecting to receive a “sizable chunk” of that payout later in calendar 2026.

And at the March 16 Dow Jones Investor Briefing, management laid out a specific five-year target: $1 billion in annual Dow Jones segment EBITDA, a roughly 70% increase from the $588 million posted in fiscal 2025.

Wall Street’s Take on NWSA Stock

The Q2 beat and the Dow Jones Investor Day reframe the AI narrative for NWSA from threat to accelerant, and that reframing has direct consequences for how the company’s earnings trajectory should be valued.

NWSA’s consensus revenue estimate for fiscal 2026 sits at $8.81 billion, up 4.2%, with EBIT expected to reach $1.09 billion, a 13.9% increase driven by margin expansion at Dow Jones rather than volume growth at the more cyclical segments.

Six of eight analysts covering News Corp stock are bullish, with four outright buys and two outperforms, while the mean target of $34.05 implies 38.5% upside from the April 9 close of $24.59, a spread uncommon for a company with 11 consecutive quarters of EBITDA growth. Wall Street is waiting for the AI licensing revenue stream to become material and recurring rather than episodic.

The target range from $27.00 to $41.00 reflects genuine disagreement about timing: the low end prices in a scenario where AI deal momentum stalls, while the high end assumes Dow Jones reaches its $1 billion EBITDA target ahead of schedule, pulling forward multiple expansion.

At roughly 23x fiscal 2026 consensus EPS of $1.06, NWSA trades at a meaningful discount to its own P/E of 26x three months ago and well below what a pure-play B2B data compounder with 17%-plus EBITDA margins would command.

With Dow Jones generating 80% recurring revenue, a 90% retention rate in Risk and Compliance, and an explicit path to $1 billion in segment EBITDA, News Corp stock is undervalued against a business that has been structurally misread as a legacy media company throughout its transformation.

The risk is that the housing market, the primary driver of Realtor.com revenue, remains suppressed. Existing home sales have been running near 4 million annually versus the 2021 peak above 6 million, and any further deterioration in transaction volumes would pressure the Digital Real Estate segment and trim the earnings growth trajectory.

Dow Jones’s Q3 fiscal 2026 results, expected in May, will be the first data point that shows whether the Anthropic payout timing and the Meta deal are beginning to show up in licensing revenues, and whether Risk and Compliance revenue sustains the 20% growth rate into the second half.

News Corp Financials

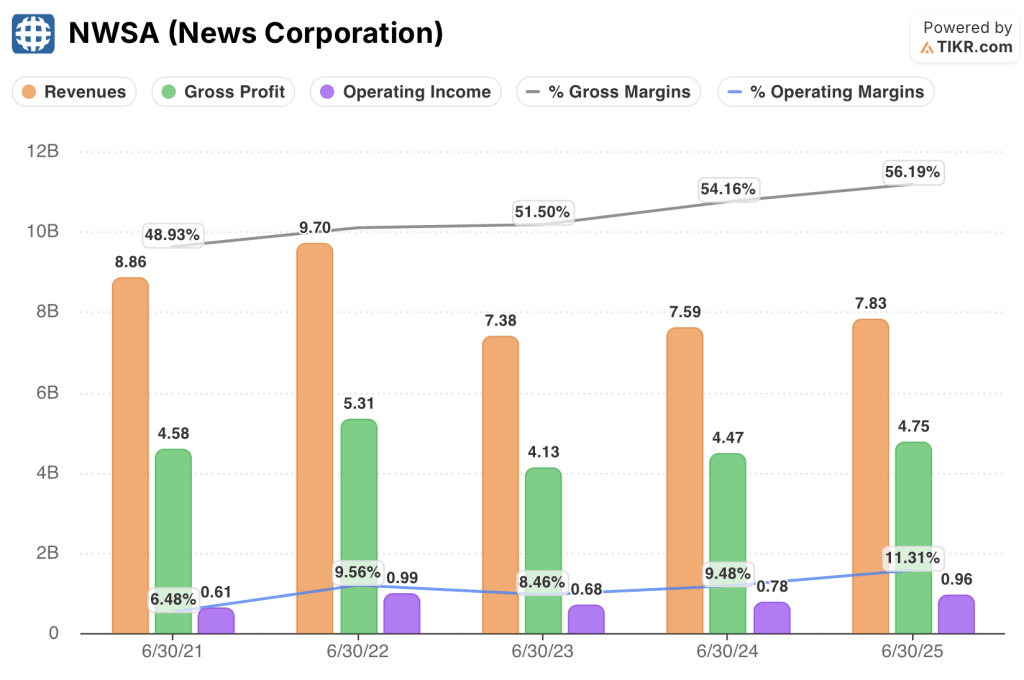

News Corporation’s operating income grew 22.3% in fiscal 2025 to $0.96 billion, pushing operating margins to 11.3%, the highest level in the five-year window shown and up from 9.5% in fiscal 2024. Total revenues reached $8.45 billion in fiscal 2025, up 2.4%, with that modest top-line growth masking a more meaningful margin story.

NWSA’s gross profit expanded to $4.75 billion in fiscal 2025, representing a gross margin of 56.2%, up from 54.2% the prior year, as the revenue mix shifted further toward Dow Jones’s high-margin subscription and data products and away from lower-margin print and advertising.

The operating margin trajectory tells the structural story directly: margins ran at 6.5% in fiscal 2021, reached 9.6% in fiscal 2022 during a strong advertising cycle, compressed to 8.5% in fiscal 2023 during the post-pandemic normalization, and have since expanded sequentially in each of the two most recent fiscal years. The company is not recovering to a prior peak; it is building to a new one.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $30.29 over 4.2 years assumes a revenue CAGR of just 3.4% and a net income margin expanding to 8.0%, both conservative relative to the 13.9% EBIT growth Wall Street already embeds in its fiscal 2026 estimates, and to the Dow Jones segment’s own stated path to $1 billion in EBITDA from $588 million today.

At a 5.1% annualized return to $30, News Corporation stock is fairly valued if the only thing that goes right is operating leverage.

The AI licensing pipeline, the Anthropic settlement payout, and a housing market recovery are not in the model, and any one of them materially changes the math.

The divergence between NWSA’s three model cases comes down to a single question: how quickly does the revenue mix shift toward Dow Jones’s high-margin B2B businesses, and how much incremental licensing revenue from AI deals flows through to earnings.

Low Case: If housing stays suppressed and AI licensing revenue proves episodic rather than recurring, revenue grows around 3.1% annually and net income margins stabilize near 7.3%, delivering a stock price of $24.20 and a negative 0.4% annualized return.

Mid Case: With Dow Jones executing on its $1 billion EBITDA roadmap and AI deals contributing modestly, revenue grows near 3.4% and margins improve toward 8.0%, reaching $30 with a 5.1% annualized return.

High Case: If the Meta and OpenAI licensing deals scale, the Anthropic settlement flows through, and Realtor.com benefits from a housing market recovery, revenue reaches around 3.8% CAGR with margins approaching 8.4%, pushing the stock to $35.82 and a 9.3% annualized return.

The mid-case requires no multiple expansion: it simply demands that Dow Jones sustains the revenue growth rate it has already demonstrated for four consecutive quarters and that margin expansion continues along the trajectory visible in the last two fiscal years. What is observable today is that Risk and Compliance grew 20% in Q2, digital Dow Jones subscriptions hit 6 million and grew 12%, and management has already secured at least two major AI content deals with more described as at an advanced negotiation stage.

Should You Invest in News Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NWSA stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track News Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NWSA stock on TIKR for Free →