Key Stats for CRH Stock

- 52-Week Range: $81.6 to $131.6

- Current Price: $101.7

- Street Mean Target: $143.1

- Street High Target: $163

- TIKR Model Target (Dec. 2030): $179.4

What Happened?

CRH plc (CRH), the world’s largest building materials company by revenue, delivered its 12th consecutive year of margin expansion in 2025, with adjusted EBITDA reaching $7.7 billion even as CRH stock trades 12% below its 52-week high of $131.55.

The catalyst was a strong Q4 2025 earnings report released February 19, with quarterly net income of $1.04 billion rising 46% year over year and full-year diluted EPS reaching $5.51, up 9.8% and ahead of the prior year on an adjusted basis.

The undeniable number is the operating leverage: CRH’s adjusted EBITDA margin expanded another 100 basis points in 2025 to roughly 20.6%, marking a 1,200-basis-point cumulative improvement since 2013 and cementing CRH’s position as the compounding infrastructure play in North America.

Jim Mintern, Chief Executive Officer, stated on the Q4 2025 earnings call that “2025 was our 12th consecutive year of margin expansion, representing an average annual increase of approximately 100 basis points since 2013,” tying directly to CRH’s stated medium-term target of reaching an adjusted EBITDA margin of 22% to 24% by 2030.

The company enters 2026 with $40 billion of projected financial capacity over five years, the Eco Material integration already outpacing early commercial synergy targets, state DOT budgets up 6%, and an active $300 million share buyback running through April 28, all pointing toward a multi-year compounding story that the current price has yet to fully price in.

Wall Street’s Take on CRH Stock

CRH’s Q4 earnings beat flips the narrative from “a slow-growth infrastructure company” to a cash-compounding machine with $2.9 billion in annual free cash flow growing at 20.8% year over year and a credible path to 100%+ FCF conversion through 2030.

CRH’s normalized EPS is forecast to reach $5.97 in 2026 and $6.63 in 2027, backed by the $200 million in net incremental EBITDA expected from CRH’s 2025 acquisition program, headlined by the $2.1 billion Eco Material Technologies deal that closed in September.

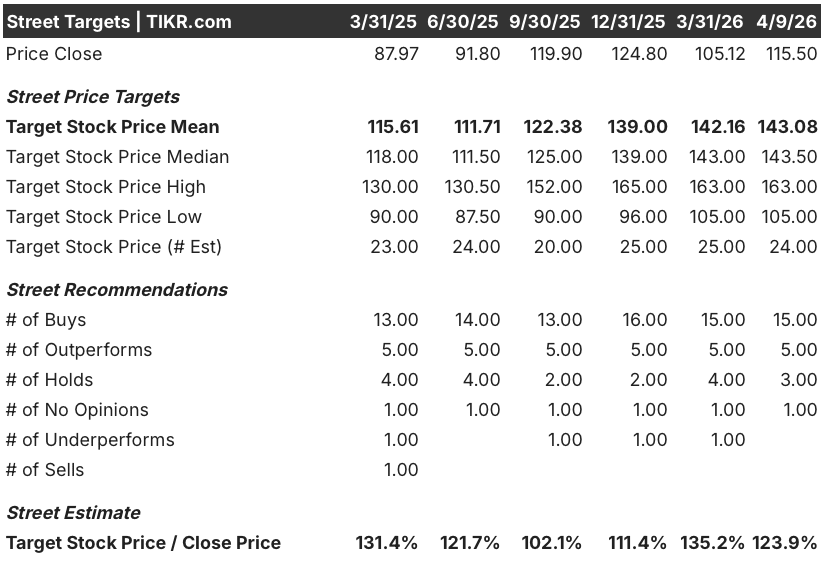

Twenty of 24 analysts covering CRH stock hold a buy or outperform rating, with a mean 12-month price target of $143.08, implying 23.9% upside from the current price; what Wall Street is waiting to see is whether the 2026 construction season confirms the record DOT-budget tailwind Randy Lake described in guidance.

The high target of $163 versus the low of $105 reflects a genuine debate: bears anchor to subdued new-build residential and tariff uncertainty, while bulls point to the IIJA runway and data center demand driving over 100 active CRH project sites across the U.S.

Priced at roughly 19.3x 2026 normalized EPS against a consensus EPS CAGR of approximately 10% through 2027, and trading below where the stock sat at mid-2025 despite a meaningfully stronger earnings trajectory, CRH stock appears undervalued as the market assigns a multiple consistent with a slow-growth materials company to a business expanding EBITDA margins toward 22% by 2030.

Macro-driven construction delays or a deterioration in the IIJA spending cadence would directly compress CRH’s most predictable revenue stream and break the margin expansion thesis.

Watch Q1 2026 results in April for aggregates volume and pricing data: low-single-digit volume growth with mid-single-digit pricing, as management guided, confirms the thesis is tracking on schedule.

CRH Stock Financials

CRH’s operating income reached $5.34 billion in 2025, up from $4.93 billion in 2024, pushing operating margins to 14.3%, a level the company has now improved in every single year since 2021’s 11.3%.

Gross profit expanded to $13.53 billion at a 36.1% gross margin in 2025, driven by disciplined commercial execution, positive pricing across aggregates and cement, and contributions from the Eco Material Technologies acquisition completed in the third quarter.

The trajectory over four years tells the cleaner story: CRH’s operating margins have moved from 11.3% in 2021 to 14.3% in 2025, a 300-basis-point structural improvement that reflects a business systematically reducing cost intensity rather than relying on volume.

What Does the Valuation Model Say?

The TIKR model assigns a mid-case target price of $179.36, implying 55.3% total return over 4.7 years at a 9.7% annualized IRR, anchored to a 6.4% revenue CAGR and 11.5% net income margins supported by CRH’s 38-acquisition M&A engine and the IIJA construction runway still ahead.

Twelve consecutive years of margin expansion and a 9.7% IRR priced at 19.3x forward earnings makes CRH undervalued against a business compounding EPS at 10% annually with $40 billion of capital capacity still ahead.

The divergence between CRH’s three model cases comes down to the pace of infrastructure spending conversion and whether the Eco Material integration delivers synergies on the front half of the runway or the back.

Low Case: If IIJA spending conversion slows and Eco synergies trail initial estimates, revenue grows around 5.7% and net income margins stabilize near 10.9%, producing a target of $147 and 5.2% annualized return.

Mid Case: With DOT budgets tracking 6% higher, data center demand sustaining over 100 active project sites, and Eco delivering the guided $200 million incremental EBITDA, revenue grows near 6.4% and margins improve toward 11.5%, producing a target of $179 and 9.7% annualized return.

High Case: If residential repair and remodel demand recovers alongside reindustrialization momentum, revenue reaches around 7.0% growth and margins approach 12.0%, producing a target of $213 and 13.8% annualized return.

The mid case requires no multiple expansion, just sustained execution of CRH’s existing M&A playbook and the IIJA drawdown the company already has line-of-sight on, with the target rounding to $179.

CRH’s bidding activity and backlogs are confirmed ahead of the prior year as of Q4, aggregates pricing is running at 6% on a mix-adjusted basis, and management has already confirmed the Eco Material integration is outpacing early commercial synergy targets.

Should You Invest in CRH plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CRH stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CRH plc alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CRH stock on TIKR for Free →