Key Stats for Honeywell Stock

- 52-Week Range: $186.8 to $248.2

- Current Price: $232.5

- Street Mean Target: $252

- Street High Target: $296

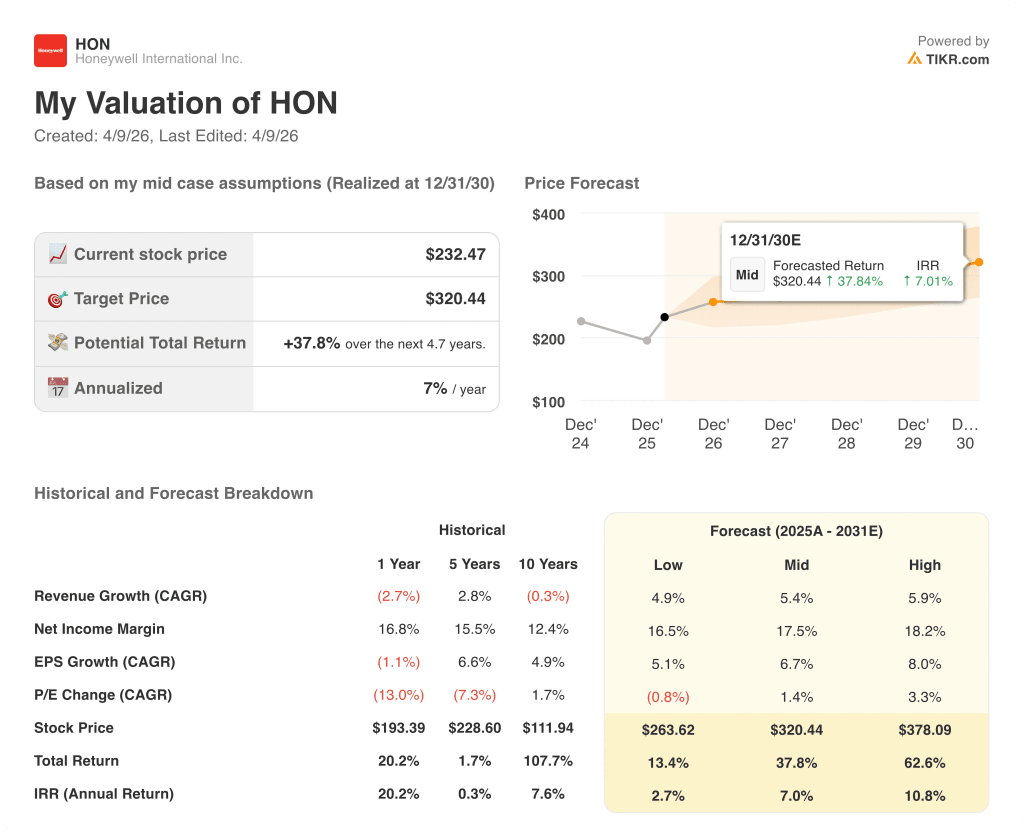

- TIKR Model Target (Dec. 2030): $320.4

What Happened?

Honeywell International (HON), a diversified industrial and aerospace manufacturer with operations spanning building controls, process automation, and defense technologies, is splitting into two independent public companies in 2026, and the market has yet to price the full value of either half.

On March 25, Honeywell Aerospace signed a supplier framework agreement with the U.S. Department of War, backed by a $500 million multi-year production capacity investment covering navigation systems, Assure actuators, and Electronic Warfare solutions.

The $500 million commitment arrives as Honeywell Aerospace, which makes up roughly 40% of total revenue and is set to trade on Nasdaq under the ticker HONA following a planned Q3 2026 separation, reported a 23% quarterly order surge in Q4 2025, pushing total backlog to a record $37 billion.

CEO Vimal Kapur stated at the Bank of America Global Industrials Conference on March 17 that “the heightened geopolitical concerns and conflicts that are happening around the world, and have been for quite some time, are fueling a substantial amount of investment in the defense sector,” reinforcing the durability of the order cycle.

Beyond the Aerospace spin, the RemainCo automation business serving buildings, process plants, and industrial facilities is on course to separate from a company whose 40% revenue portfolio churn over the past three years, $4 billion credit facility secured by Honeywell Aerospace in March, and June Investor Day catalysts set both entities up for a re-rating that the current HON stock price does not reflect.

Wall Street’s Take on HON Stock

The Aerospace spin completes Honeywell’s transformation from a sprawling conglomerate into two focused franchises, each commanding a structurally different multiple than the blended discount HON has traded at for years.

With consensus revenue estimates rising from $37.4 billion in 2025 to $39.5 billion in 2026 and EPS normalized growing from $9.78 to $10.53, anchored by the $500 million defense production ramp and Building Automation’s five consecutive quarters of high single-digit organic growth, the forward earnings picture is cleaner than it has been in over a decade.

Fifteen analysts rate HON a buy or outperform against nine holds and two underperforms, with a mean price target of $251.98 implying 8.4% upside from current levels; the Street is waiting on the Q3 Aerospace separation to close before committing to a meaningfully higher multiple.

The high-low target spread of $296 to $198 reflects a real debate: the $296 camp prices in successful spin execution and defense production expansion, while the $198 floor prices in Middle East revenue disruption and sustained petrochemical catalyst weakness into 2027.

HON trades at roughly 22x 2026 consensus EPS, a modest discount to the 24x to 25x peers like Emerson Electric command without a pending breakup catalyst, which leaves Honeywell stock undervalued given the re-rating potential as two pure-play companies replace the current conglomerate discount.

BMO’s March 27 initiation at outperform with a $273 target specifically cited that “HON’s strong aerospace and defence fundamentals remain underappreciated, with further upside through the decade,” a read that preceded the $500 million Department of War agreement by just days.

The single development that breaks the bull case is prolonged Middle East conflict forcing sustained Q2 and Q3 shipping delays beyond the high-single-digit revenue exposure CEO Kapur has characterized as tactical.

Q1 earnings on April 23 are the next confirming event: watch for the Aerospace segment margin figure relative to the 26% baseline and any update on the PSS and Warehouse Workflow Solutions sale expected in Q2.

Honeywell Stock’s Income Statement

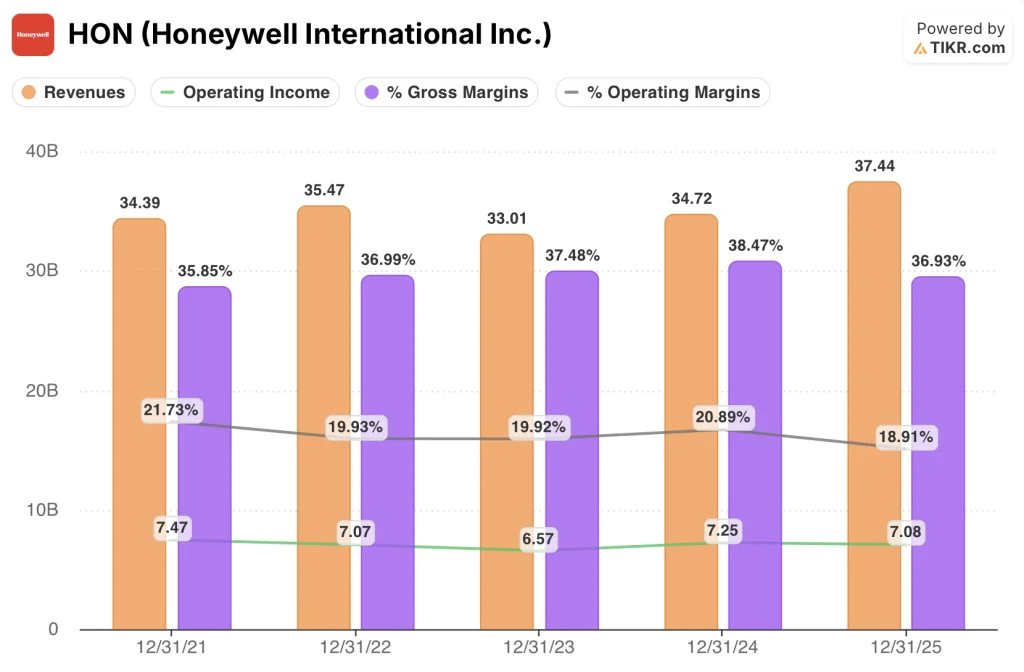

Honeywell grew revenue 7.8% to $37.4 billion in 2025, recovering from the 6.9% decline in 2023, as Aerospace order conversion and Building Automation volume gains offset persistent weakness in petrochemical catalyst demand within the Process segment.

The 2025 gross margin compression to 36.9% from the 38.5% peak in 2024 reflects a heavier mix of lower-margin defense OE shipments and the absence of high-margin catalyst volume that depressed Energy and Sustainability Solutions results across the second half.

HON’s operating income fell 2.4% to $7.1 billion in 2025 despite revenue growth, pulling the operating margin down to 18.9% from 20.9% in 2024, a combination of stepped-up R&D at approximately 4.8% of sales and $436 million in Industrial Automation goodwill impairment charges recorded during the year.

The tension in the income statement is that Honeywell’s operating leverage profile has deteriorated even as the backlog and order growth story has strengthened: the company enters 2026 with the largest backlog in its history and the lowest operating margin in four years.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $320 per share, realized over 4.7 years, is built on a 5.4% revenue CAGR and a net income margin recovery to 17.5%, both assumptions that look conservative against the $37 billion backlog, confirmed $500 million defense production ramp, and Building Automation’s five-quarter share gain trend.

At 22x 2026 earnings with two pure-play franchises separating inside of six months, Honeywell stock is undervalued — the conglomerate discount embedded in the current multiple does not survive the spin.

Whether the two-company structure delivers its full re-rating depends on execution speed across the Aerospace spin, automation margin recovery, and defense order conversion.

Low Case: If Middle East disruption persists into Q3, the Aerospace separation slips or incurs higher stand-up costs, and petrochemical catalysts remain depressed, revenue grows around 4.9% and net income margins stabilize near 16.5%, implying a $264 target price and a 2.7% annualized return.

Mid Case: With the Aerospace spin completing on schedule in Q3, defense production ramping per the $500 million framework agreement, and Building Automation holding mid-single-digit organic growth, revenue grows near 5.4% and margins improve toward 17.5%, pointing to $320 and a 7.0% annualized return.

High Case: If the Aerospace separation triggers a meaningful re-rating, LNG project backlog converts ahead of schedule in the second half, and industrial automation margin expansion reaches the top of guidance, revenue reaches around 5.9% CAGR and margins approach 18.2%, pointing to $378 and a 10.8% annualized return.

The mid case requires revenue growth near the midpoint of Honeywell’s own 3% to 6% organic guidance and operating margin expansion of 20 to 60 basis points, with no multiple expansion built in at current prices.

Right now, the observable evidence supports the mid case: Q1 orders were tracking mid-single-digit growth across the automation segments as of mid-March, the $37 billion backlog is firm purchase orders not estimates, and management’s 2026 EPS guide of $10.35 to $10.65 already accounts for Middle East shipping disruption as a transitory event.

Should You Invest in Honeywell International Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HON stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Honeywell International Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HON stock on TIKR for Free →