Key Stats for Carrier Stock

- 52-Week Range: $50.2 to $81.1

- Current Price: $55.4

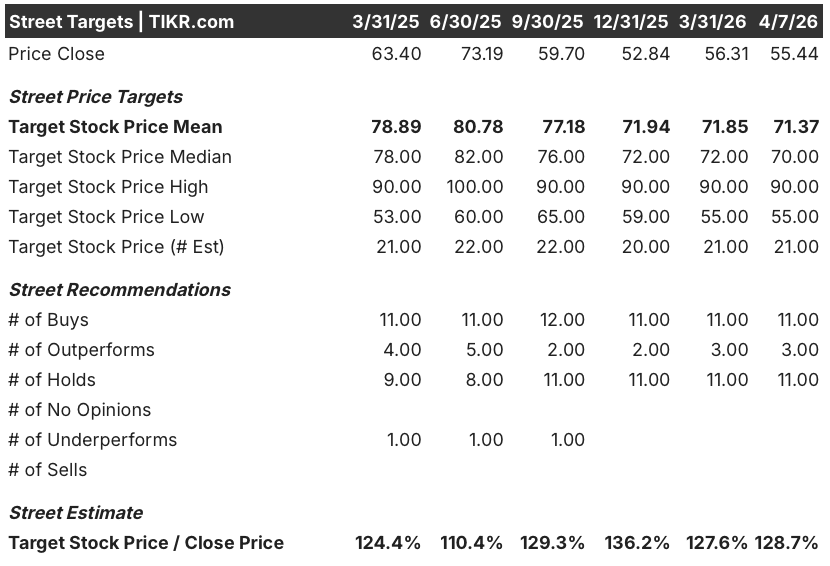

- Street Mean Target: $71.4

- Street High Target: $90

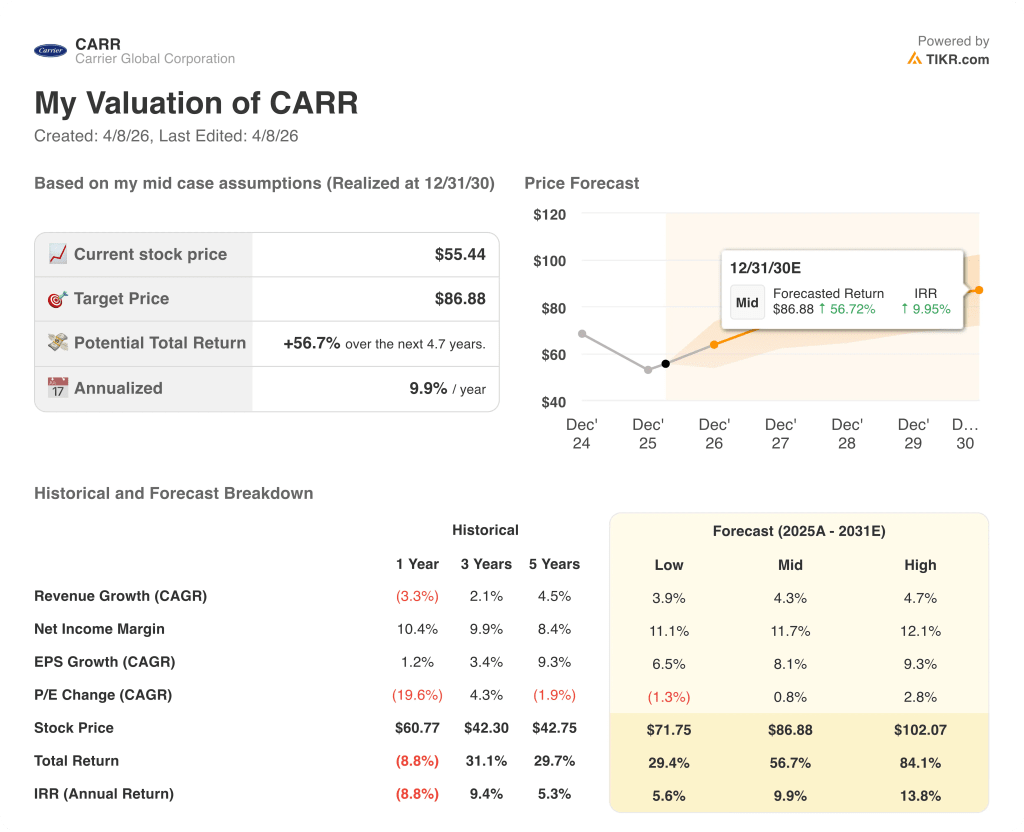

- TIKR Model Target (Dec. 2030): $86.9

What Happened?

Carrier Global (CARR), a maker of HVAC, refrigeration, and building controls systems, is trading near a 52-week low of $55.44 even as the commercial segment at the heart of its long-term thesis grew data center orders roughly 400% in Q4 2025.

The trigger was a February earnings miss: Q4 adjusted operating income came in at $455 million against a Wall Street estimate of $532.6 million, and full-year 2026 EPS guidance of $2.80 came in below the $2.91 consensus, sending CARR shares down nearly 7% in premarket trading on February 5.

The drag came almost entirely from the residential and light commercial businesses, which together represent over 50% of the portfolio, with CSA Residential sales falling nearly 40% in Q4 as distributor destocking and a housing market strained by 30-year mortgage rates starting with a 6 crushed near-term volumes to roughly 6.5 million industry units in 2026 against a long-run mean of 9 million.

David Gitlin, Chairman and CEO, stated on the Q4 2025 earnings call that “we are still in the early innings and our expanded portfolio now addresses essentially all major data center chiller applications,” tying the comment to a Q4 CSA applied order book that more than tripled year-over-year and a 2026 data center revenue target of $1.5 billion, up from approximately $1 billion in 2025.

A $1.5 billion share repurchase program, a sixth consecutive year of double-digit aftermarket growth targeted for 2026, a new Viessmann-branded mid-tier heat pump launching in Europe later this year, and the planned Riello divestiture expected to close in Q1 collectively position CARR to expand margins and accelerate earnings once the residential cycle inflects.

Wall Street’s Take on CARR Stock

The Q4 miss has pushed CARR to near-cycle lows while the data center engine powering the long-cycle thesis has never been stronger, making the current price a function of short-cycle fear rather than structural impairment.

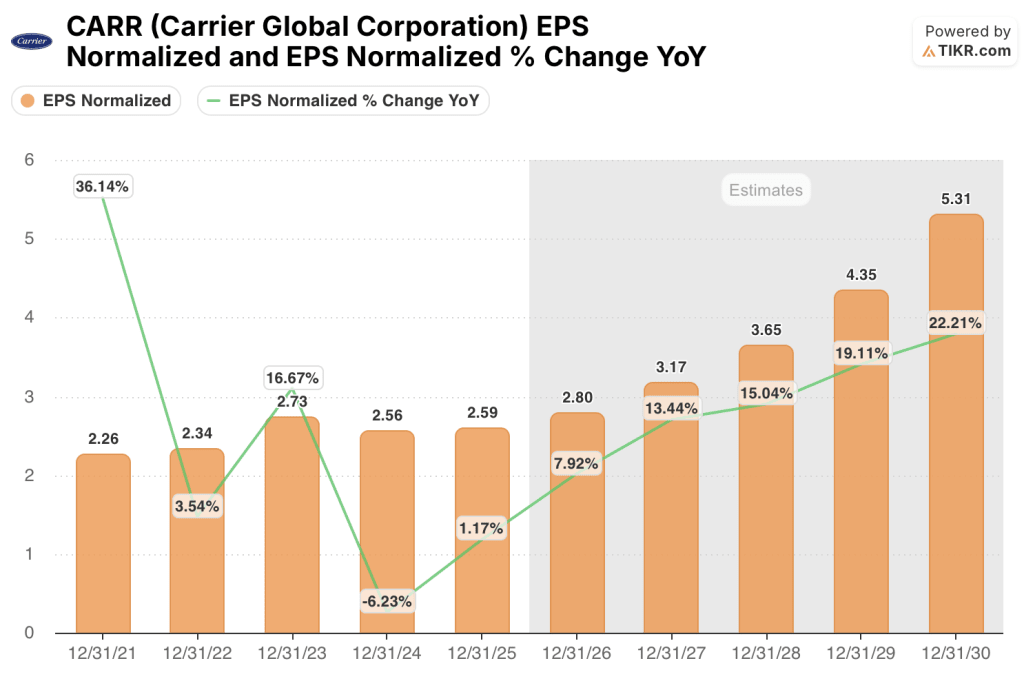

CARR’s consensus 2026 EPS estimate of $2.80 reflects only the beginning of a multi-year earnings ramp, with consensus estimates climbing to $3.17 in 2027 and $3.65 in 2028, all anchored to the data center backlog conversion and the $100 million in overhead savings Carrier executed in 2025 flowing through the P&L this year.

Fourteen of 25 analysts covering CARR carry a Buy or Outperform rating, with a mean price target of $71.37 implying roughly 28.7% upside from current levels, as analysts wait for the second-half 2026 data center shipment acceleration and the first signs of residential sell-through stabilization to confirm the recovery thesis.

The $55 low target and the $90 high target define the real debate: bears price in a prolonged residential downturn and structural demand impairment, while bulls anchor on the data center backlog converting into $1.5 billion of 2026 revenue and a residential market bottoming at 6.5 million units before reverting to the 9 million-unit mean.

CARR is undervalued at roughly 19.8x 2026 consensus EPS of $2.80, a discount to its two-year pre-downturn multiple in the low-to-mid 20s, against an EPS growth trajectory that reaches $3.65 by 2028 as data center deliveries accelerate and residential fixed costs deabsorb into a recovering volume base.

Gitlin’s March 19 JPMorgan conference confirmation that Q1 was “100% tracking to plan,” with data center orders set to be “very, very strong again” in Q1, meaningfully narrows the execution risk embedded in the current valuation.

The structural risk is a prolonged housing market freeze: if 30-year mortgage rates stay above 6.5% through 2027 and existing home sales remain at 20-year lows, the under-absorption in CSA Residential manufacturing will continue to suppress incremental margins and push EPS recovery further out.

Q2 2026 earnings, where residential year-over-year comps begin to ease and the first batch of second-half data center bookings flow into backlog disclosures, will confirm whether the 40%-plus incremental margins management guided for the CSA segment in the second half are tracking.

Carrier Global Income Statement

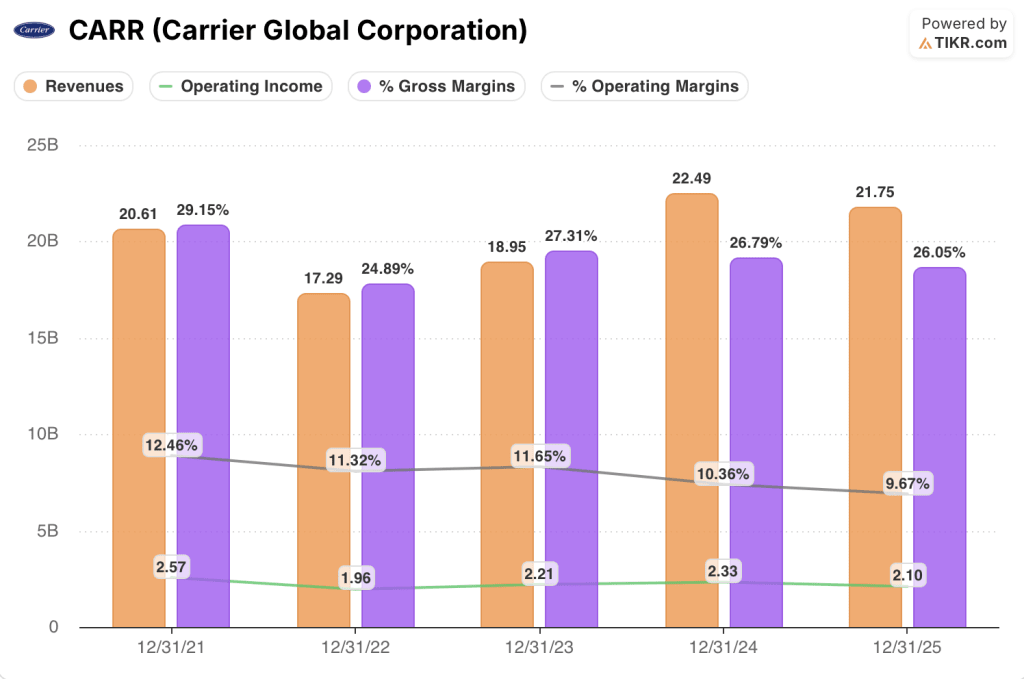

Carrier’s operating income fell 9.7% in 2025 to $2.10 billion, compressing the operating margin to 9.7%, the lowest in the five-year data set, as the company absorbed a sharp volume collapse in its highest-margin residential and light commercial manufacturing lines.

The compression came directly from the CSA Residential destocking cycle, which drove Q4 manufacturing output to less than half the prior-year level and created the under-absorption that Patrick Goris, CFO, confirmed on the Q4 call would begin to unwind as the seasonal ramp in Q2 rebuilds factory utilization.

What the margin trajectory reveals on a longer view is that CARR expanded operating income from $1.96 billion in 2022 to $2.33 billion in 2024 while building out the data center and aftermarket platforms, meaning the 2025 compression is a cyclical dip into a structurally improving cost base, not a trend reversal.

Gross margins have held in a narrower range, falling only from 26.8% in 2024 to 26.1% in 2025, which suggests the pricing power in commercial HVAC and aftermarket is partially offsetting the volume-driven gross profit contraction on the residential side.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $86.88 by December 2030, implying a 56.7% total return on a 9.9% IRR, is built on a 4.3% revenue CAGR and an 11.7% net income margin expansion from today’s 10.3%, both of which look conservative against a data center portfolio targeting $1.5 billion in 2026 alone and management’s long-run 6% to 8% organic growth algorithm.

A 56.7% model return priced at under 20x forward earnings makes the undervalued case for CARR — the multiple prices in residential impairment that a $1.5 billion data center backlog and record commercial orders do not support.

CARR stock results through December 2030 will be shaped by how fast the residential cycle normalizes, how much data center backlog converts into shipped revenue, and whether the overhead reductions taken in 2025 hold as volume returns.

Low Case: If residential volumes stay near trough levels and data center delivery slips past 2026, revenue grows around 3.9% and margins stabilize near 11.1% → 5.6% annualized return.

Mid Case: With data center shipments accelerating in the second half and aftermarket compounding steadily, revenue grows near 4.3% and margins improve toward 11.7% → 9.9% annualized return.

High Case: If residential sell-through recovers faster than guided and the air-cooled chiller share gains mirror the water-cooled playbook, revenue reaches around 4.7% and margins approach 12.1% → 13.8% annualized return.

The $87 mid-case target does not require a re-rating or a residential recovery miracle — it requires Carrier to deliver the $1.5 billion data center revenue already in backlog, hold the $100 million in overhead savings executed last year, and let aftermarket compound the way it has for five consecutive years.

What is actually happening right now: residential field inventory is down 32% year-over-year as of last March, destocking is largely behind the company, and Q1 is tracking exactly to plan — meaning the setup for the second-half earnings acceleration management guided is largely intact, and the stock is priced as though none of it arrives.

Should You Invest in Carrier Global Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CARR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Carrier Global Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CARR stock on TIKR for Free →