Key Stats for Monolithic Power Stock

- 52-Week Range: $438.9 to $1,256.2

- Current Price: $1,180

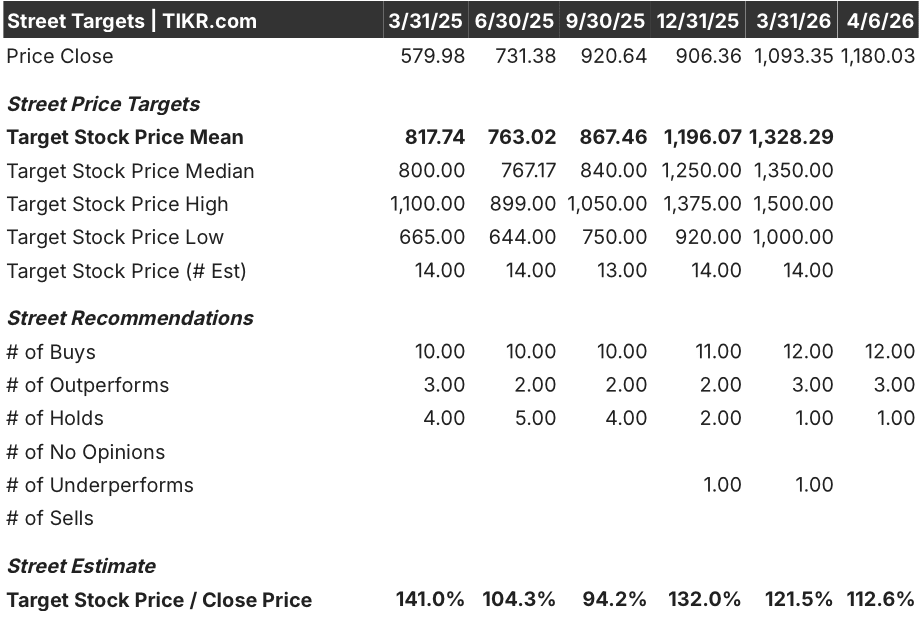

- Street Mean Target: $1,328.3

- Street High Target: $1,500

- Valuation Model Target: $2,325.6

What Happened?

Monolithic Power Systems (MPWR), a designer of high-efficiency power management semiconductors used in AI data centers, automotive, and industrial systems, posted $2.8 billion in full-year revenue for 2025, up 26.4%, while raising its Q1 2026 guidance to $770–$790 million against a Wall Street consensus of just $732 million.

The Q4 2025 earnings release on February 5 was the trigger, with quarterly revenue of $751.2 million beating the $739.9 million consensus, while management simultaneously raised the quarterly dividend 28% to $2.00 per share, the kind of capital allocation move that signals confidence in the durability of free cash flow.

The acceleration runs deeper than the top line: non-Enterprise Data end markets, which include automotive, communications, and storage — segments less exposed to single-customer AI concentration risk — grew by over 40% in 2025, demonstrating that the company’s diversified platform is firing on multiple cylinders, not just riding one wave.

Tony Balow, Vice President of Finance, stated on the Q4 2025 earnings call that “our quarterly dividend will increase 28% to $2 per share” and that “for the 3 years ending with December 2025, MPS has returned over 72% of free cash flow to stockholders through share repurchases and dividends,” anchoring the capital return story to a structural commitment rather than a one-time event.

CEO Michael Hsing’s push to migrate the product mix from silicon chips to power modules and full system solutions — where average selling prices are meaningfully higher — combined with an Enterprise Data growth floor management raised to at least 50% for 2026, positions Monolithic Power Systems stock to compound at a rate that its current $1,168 trading price does not appear to fully reflect.

Wall Street’s Take on MPWR Stock

The Q4 beat and guidance raise do more than confirm execution: they establish a new minimum growth floor for the segment that drives Monolithic Power Systems’ re-rating thesis, pulling forward the earnings trajectory that analysts had modeled as a second-half 2026 story.

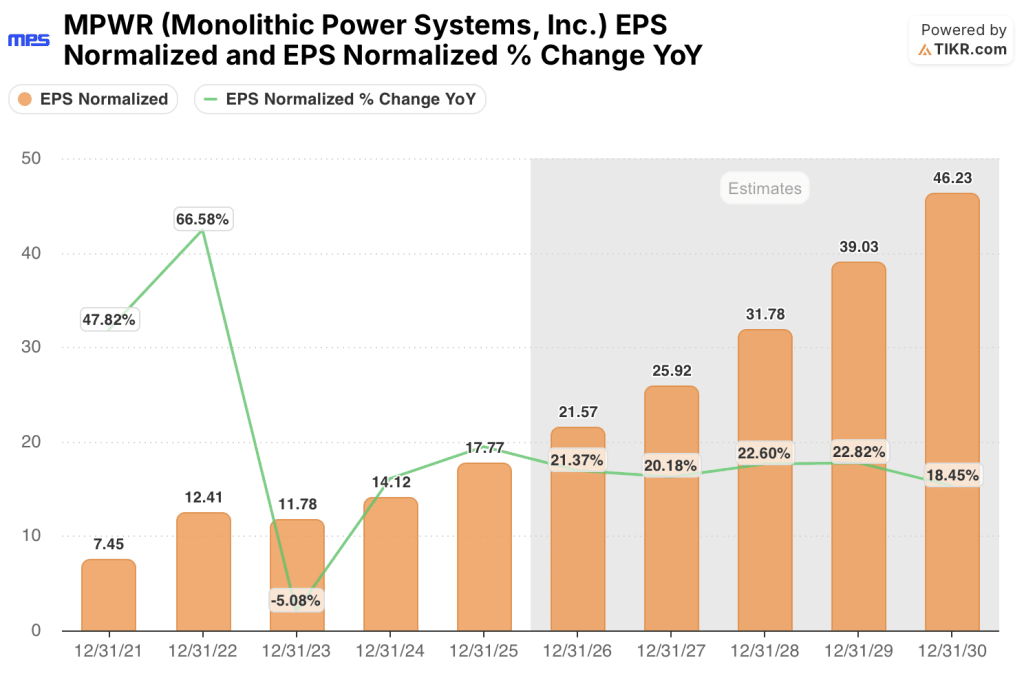

MPWR’s normalized EPS is expected to reach $21.57 in 2026 and $25.92 in 2027, growth of 21.4% and 20.2% respectively, anchored by the same Enterprise Data bookings acceleration that pushed management to raise the growth floor from 30%–40% to at least 50% for the current fiscal year.

Fifteen of 16 analysts covering MPWR currently rate the stock a buy or outperform, with one hold and one underperform, and the mean price target sits at $1,328.29, implying approximately 13.7% upside — though Wall Street is specifically waiting on Q1 2026 results in late April to validate whether the Enterprise Data booking surge is demand-driven or partially reflects customer double-ordering.

The spread between the $1,000 street low and $1,500 street high is not noise: the low reflects concern that AI capex could decelerate and expose Monolithic Power Systems’ Enterprise Data concentration, while the high prices in the full realization of the module and systems transition, where higher ASPs structurally expand margins toward the 55%–60% corporate target.

Priced at roughly 54x forward normalized EPS of $21.57 against a backdrop of reaccelerating Enterprise Data growth, a 40%+ non-Enterprise Data growth year in 2025, and a revenue CAGR consensus of 21.2% through 2026, MPWR stock appears undervalued relative to its own growth rate, particularly as the company transitions mix toward higher-ASP module and system solutions that should push margins toward the upper end of the 55%–60% model range.

The restatement of 2024 and 2025 financials — disclosed in the February 27 SEC filing — introduces an accounting overhang that could weigh on sentiment until the amended figures are cleared and audited.

Q1 2026 earnings in late April is the definitive catalyst: revenue guidance of $770–$790 million and an Enterprise Data revenue run-rate that annualizes to at least 50% growth from 2025’s $701.8 million base are the two numbers to watch.

MPWR Stock Income Statement

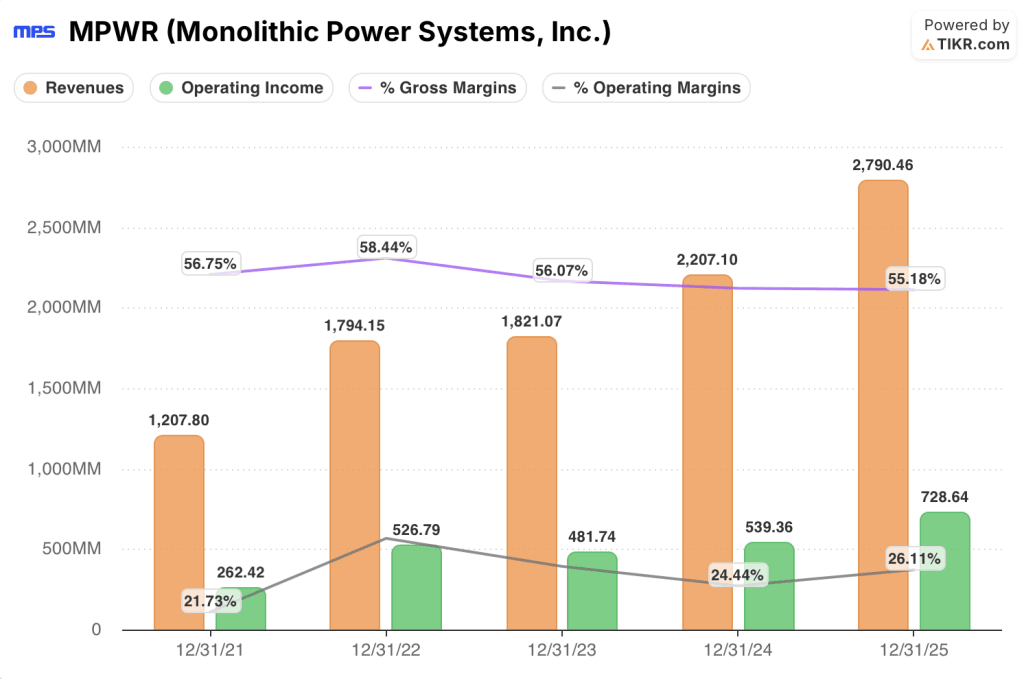

Monolithic Power Systems Stock delivered operating income of $730 million in 2025, up 35.1% year over year, representing the strongest operating income growth since fiscal 2022 and marking the second consecutive year of re-acceleration after a trough in 2023.

The driver is operating leverage: total operating expenses grew 19.0% to $810 million while revenue grew 26.4%, allowing MPWR’s operating margin to expand 170 basis points to 26.1% — the first meaningful improvement after two years of compression from 29.4% in 2022.

Gross margins have remained remarkably stable across the cycle, holding between 55.2% and 58.4% over the last five fiscal years, which reflects the pricing power of a proprietary power management architecture that is difficult for customers to design around.

The one tension in the income statement: gross margin ticked down to 55.2% in 2025 from 55.3% in 2024, the low end of the 55%–60% model, and management explicitly acknowledged that reaching the upper half requires longer-duration backlog visibility — which the current ordering pattern has only just begun to provide.

What Does the Valuation Model Say?

The TIKR model’s mid-case price target of $2,325.61 — implying 97.1% total return from current levels — is built on an 18.7% revenue CAGR through 2030 and a net income margin expanding to 32.1%, both of which are conservative relative to MPWR’s own 5-year and 10-year historical growth rates of 27% and 23.7% respectively, and are supported directly by the Enterprise Data growth floor raised on the Q4 call.

The numbers make MPWR look undervalued — trading near 54x forward earnings while posting reaccelerating growth across five end markets, a company compounding EPS at 21% annually rarely stays at this multiple for long.

The investment case hinges on a single question: does the Enterprise Data bookings surge that management cited in Q4 represent genuine structural demand, or does customer capacity anxiety inflate the backlog in ways that create a hangover in late 2026?

What Has to Go Right

- Enterprise Data revenue grows at least 50% in 2026 off a $701.8 million base, consistent with management’s floor guidance and Hsing’s open suggestion that 50% was conservative

- Gross margins begin the guided 10–20 basis point sequential expansion through 2026 as backlog extends into Q2 and Q3, confirming the mix shift toward modules is gaining traction

- Q1 2026 revenue lands at or above the $780 million midpoint, validating the guidance raise as demand-driven rather than channel-pull-forward

- The financial restatement for 2024 and 2025 resolves without material changes to core operating metrics, clearing the accounting overhang

What Could Go Wrong

- AI infrastructure capex moderates in the second half of 2026 as hyperscalers digest existing capacity, compressing the Enterprise Data growth rate below 50% and breaking the model’s core assumption

- Customer double-ordering, which management explicitly flagged as a risk on the Q4 call, inflates near-term backlog and produces a demand air pocket in Q3 or Q4 of 2026

- The financial restatement reveals a more substantive accounting issue than currently disclosed, triggering multiple compression and delaying the re-rating thesis

- Automotive demand softens from tariffs, EV subsidy rollbacks, or macroeconomic pressure, removing one of the 40%+ growth engines that offset Enterprise Data in 2025

Should You Invest in Monolithic Power Systems, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MPWR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Monolithic Power Systems, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MPWR stock on TIKR for Free →