Key Stats for Kinder Morgan Stock

- 52-Week Range: $23.9 to $34.7

- Current Price: $33

- Street High Target: $43

What Happened?

Kinder Morgan (KMI), the Houston-based pipeline operator that moves roughly 40% of all U.S. natural gas production daily, posted all-time record 2025 adjusted EBITDA of $8.4 billion while its project backlog surged to $10 billion, as the stock trades at $32.97 near its 52-week high of $34.73.

TD Cowen raised its price target to $35 from $34 on January 22 after KMI reported Q4 adjusted EPS of $0.39, beating the LSEG consensus of $0.37, with Q4 revenue of $4.51 billion clearing the $4.31 billion estimate by a 5% margin.

Natural gas transport volumes, the throughput KMI earns fee-based revenue on as gas moves through its 80,000-mile pipeline network, rose 9% in Q4 to 48.4 TBtu per day driven by surging liquefied natural gas (LNG) feed gas deliveries on the Tennessee Gas Pipeline, a critical artery connecting domestic supply to Gulf Coast export terminals.

The backlog expansion also triggered a credit upgrade: S&P lifted KMI to BBB+ on January 16, recognizing the balance sheet’s 3.8x net debt-to-EBITDA ratio, near the low end of management’s 3.5x to 4.5x target range.

CEO Kimberly Dang stated on the Q4 2025 earnings call that “we have a $10 billion approved project backlog and tremendous potential beyond that we are set up for a very exciting future,” anchoring confidence in the company’s ability to fund all growth from the $5.92 billion in annual operating cash flow without tapping equity markets.

KMI’s competitive position over the next three to five years rests on three reinforcing pillars: LNG feed gas demand forecast to nearly double from 19.8 Bcf per day in 2026 to over 34 Bcf per day by 2030, a shadow project opportunity set exceeding $10 billion beyond the sanctioned backlog, and three flagship pipeline projects including Mississippi Crossing and South System 4 already on budget and pulling forward their in-service dates to as early as Q2 2028.

Wall Street’s Take on KMI Stock

The record $10 billion backlog, funded entirely from KMI’s $5.92 billion in annual operating cash flow, positions the company to add over $500 million in annual EBITDA as projects enter service, driving TIKR’s forecast that normalized EBITDA reaches $10.24 billion by December 2030.

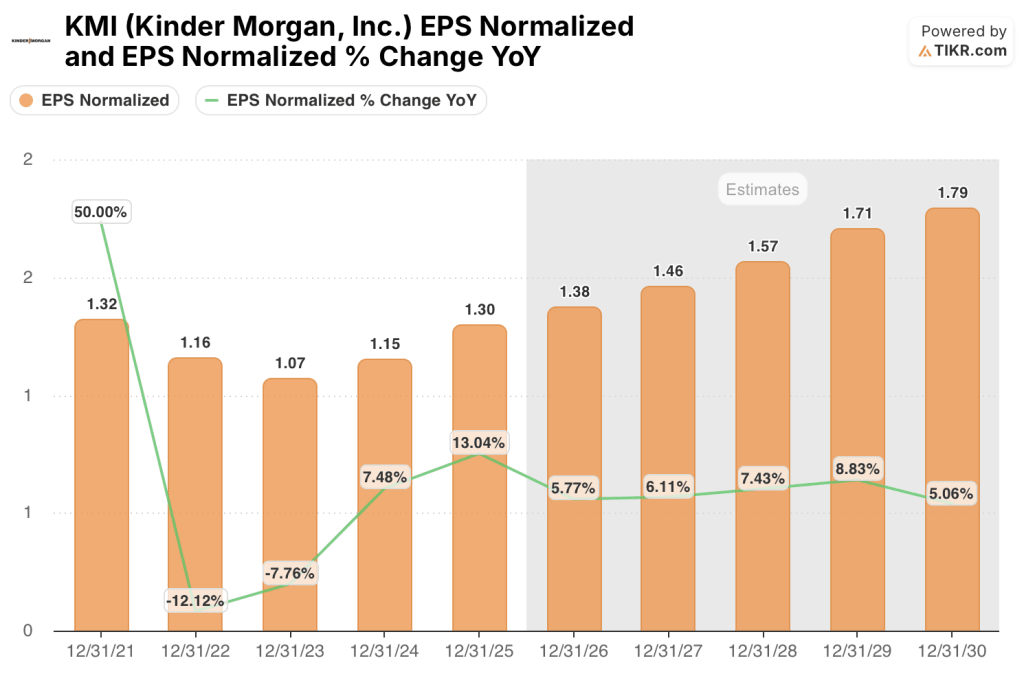

TIKR estimates 2026 normalized EPS at $1.38, rising to $1.46 in 2027, supported by higher transport volumes as LNG feed gas demand hits a projected record 19.8 Bcf per day average this year, up 19% from 2025’s 16.6 Bcf per day average.

Ten analysts rate KMI a buy or outperform against ten holds and one underperform, with a mean price target of $34.82 implying 5.6% upside from $32.97, as the street awaits proof that Mississippi Crossing and South System 4 translate backlog dollars into EBITDA on schedule.

The high target of $43.00 reflects full execution on the $10 billion backlog and continued LNG feed gas ramp, while the low of $26.00 prices in a scenario where project delays or a softening LNG sanction cycle stalls the EBITDA growth trajectory.

What Does the Valuation Model Say?

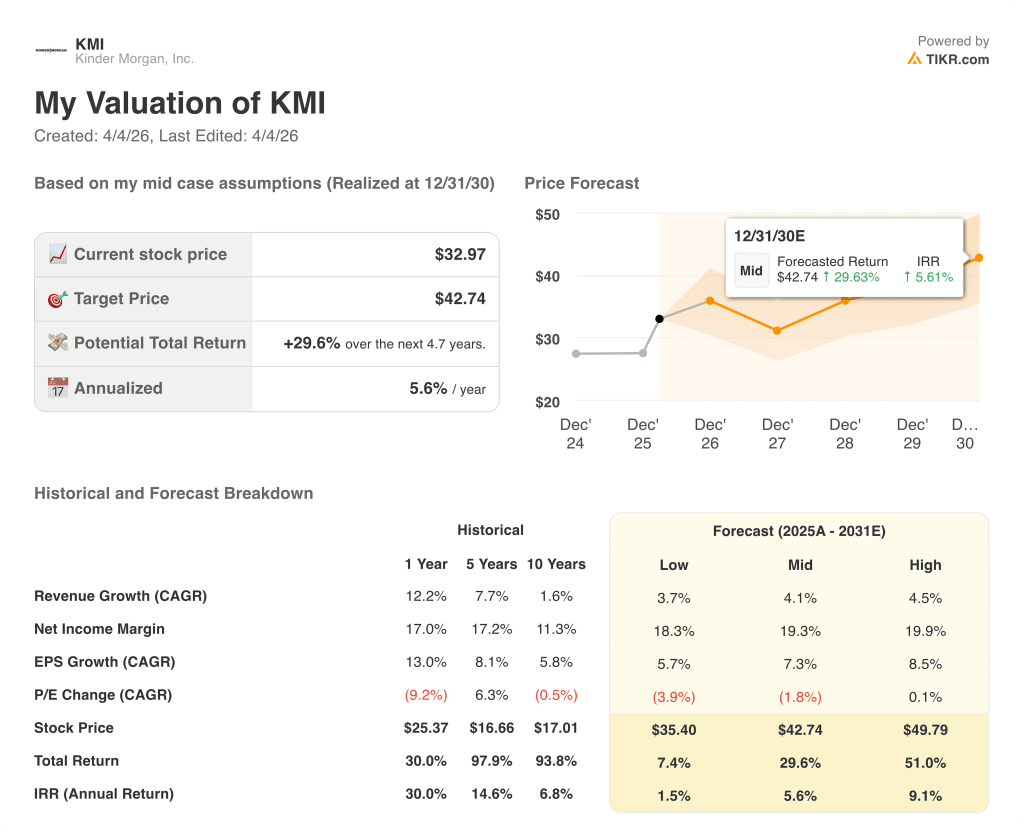

At the current price, KMI trades at roughly 11.4x 2026E EBITDA of $8.68 billion, a modest premium to its five-year historical range of 10x to 11x, yet the TIKR mid-case target of $42.74 reflects a 7.3% normalized EPS CAGR through 2030, making the stock fairly valued today with a skew toward upside if backlog execution holds.

At roughly 11.4x 2026E EBITDA of $8.68 billion, KMI trades at a modest premium to its five-year historical EV/EBITDA average of approximately 10x to 11x, yet the 7.3% normalized EPS CAGR through 2030, anchored by $500 million in annual EBITDA additions from the sanctioned backlog, makes KMI stock fairly valued with a credible path to re-rating higher as projects enter service.

The TIKR mid-case price target of $42.74 assumes the $10 billion sanctioned backlog converts at a 5.6x build multiple and LNG feed gas contracts, which are essentially take-or-pay in structure, underwrite the EBITDA growth from $8.68 billion in 2026 to $10.24 billion by 2030.

The strongest operational signal is pipeline utilization already at 90% across KMI’s five largest pipelines, versus 74% in 2016, as tightening capacity forces shippers to sign contracts averaging 7 to 8 years, up from 5 to 6 years previously.

The primary model risk is a slowdown in new LNG project sanctions on the U.S. Gulf Coast, which would compress the shadow backlog and cap the EBITDA growth trajectory beyond 2027.

Mississippi Crossing’s FERC final certificate, anticipated by July 31, is the near-term event to watch, as an on-time ruling would confirm the Q2 2028 in-service date and validate the backlog build cadence underpinning TIKR’s $42.74 target.

Should You Invest in Kinder Morgan, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up KMI stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Kinder Morgan, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze KMI stock on TIKR for Free →