Key Stats for Doximity Stock

- 52-Week Range: $21.8 to $76.5

- Current Price: $22.8

- Street High Target: $56

What Happened?

Doximity (DOCS), the digital platform connecting more than 85% of U.S. physicians, entered 2026 as the dominant medical AI network after surpassing 300,000 quarterly active users on its AI suite in a single quarter, even as shares trade near their 52-week low of $21.82 against a high of $76.51.

Doximity’s fiscal Q3 2026 results, reported February 5, showed revenue of $185.1 million, a 10% year-over-year gain that beat the LSEG consensus of $182.2 million, while adjusted EBITDA of $111.4 million topped estimates of $104.7 million by 6.4%.

Driving that outperformance was a record 720,000 quarterly active prescribers on its workflow tools, which include telehealth, digital fax, and AI-assisted documentation, representing the largest sequential gain in the metric’s history and cementing Doximity’s lead over rivals including Microsoft Teams and Zoom in physician-facing telehealth.

Jeffrey Tangney, Co-Founder and CEO, stated on the Q3 2026 earnings call that “in our first full quarter since acquiring Pathway AI in August, we’ve already become one of the most used AI tools by physicians,” directly underpinning the platform’s record AI engagement of 300,000 active prescribers within one quarter of the deal closing.

A $500 million open-ended share repurchase program authorized February 5, a confirmed commercial AI product launch expected later in calendar 2026, and management’s explicit target of exiting calendar 2026 as a double-digit revenue grower collectively position Doximity to convert its physician network dominance into a new monetizable search and engagement revenue stream over the next three to five years.

Wall Street’s Take on DOCS Stock

The record Q3 engagement across Doximity’s newsfeed, workflow tools, and AI suite signals that the platform’s physician retention is accelerating precisely as the stock trades near multi-year lows, creating a direct disconnect between operating momentum and market price.

Doximity’s 2026 revenue is estimated at $640M, growing 12.8% year-over-year on the back of 112% net revenue retention and record pharma bookings in January, while normalized EPS of $1.62 reflects a platform that converts physician engagement into earnings with structural consistency.

The AI product suite, which reached 300,000 active prescribers in its first full quarter post-Pathway acquisition, provides a second revenue vector not yet reflected in estimates, giving DOCS an organic growth driver that could meaningfully lift 2027’s estimated $700M revenue base.

Analyst conviction has sharpened materially, with 13 buys, 5 outperforms, 5 holds, 1 underperform, and 1 sell on record; the mean price target of $39.55 implies 73.7% upside from the current $22.77, anchored to AI commercialization and pharma budget normalization.

The spread between the $25.00 floor and $56.00 ceiling targets reflects two distinct outcomes: the low assumes persistent pharma budget headwinds and delayed AI monetization, while the high prices in full commercial AI launch and a double-digit revenue exit rate by calendar year-end.

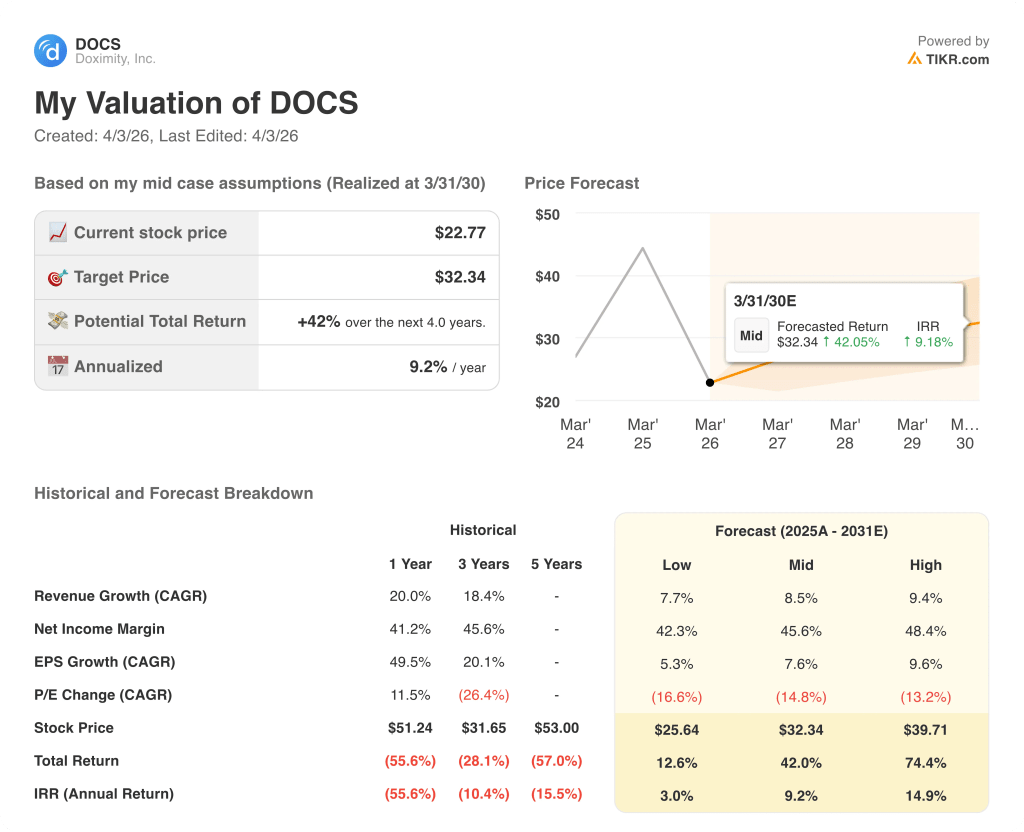

What Does the Valuation Model Say?

The TIKR mid-case model prices DOCS at $32.34 by March 2030, embedding an 8.5% revenue CAGR and 45.6% net income margin, both supported by the record 720,000 workflow users and the 100-plus health system AI contracts already signed.

At roughly 14x forward normalized EPS of $1.62, DOCS trades at a steep discount to its own historical premium multiple while sustaining 50%-plus EBITDA margins and 12.8% revenue growth, making DOCS stock deeply undervalued relative to both its earnings quality and its AI optionality.

The $500M open-ended buyback authorized February 5, layered on top of $735M in cash and securities on the balance sheet, confirms management is deploying capital at what it views as a historically mispriced entry point.

January pharma bookings hitting the highest growth rate since the IPO signals the MFN-driven budget delay was timing-related, not structural, directly supporting the model’s assumption of a double-digit revenue exit rate for calendar 2026.

If pharma budgets tighten further or AI commercialization slips beyond calendar 2026, the model’s 9% revenue growth assumption breaks and the path to $39.55 extends materially.

The Q4 FY2026 earnings report, covering the March 31 quarter-end, is the first hard data point to confirm whether delayed pharma deals converted and whether the commercial AI product timeline is on track.

Should You Invest in Doximity, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DOCS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Doximity, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DOCS stock on TIKR for Free →