Key Stats for Amgen Stock

- 52-Week Range: $261.4 to $391.3

- Current Price: $347.9

- Street High Target: $432

What Happened?

Amgen (AMGN), a global biotechnology company with 14 products each generating over $1 billion in annual sales, reported Q4 2025 revenue of $9.87 billion against a $9.47 billion consensus estimate, a beat that validated management’s claim of durable broad-based growth at a stock price of $347.94.

On February 4, Amgen issued full-year 2026 guidance of $37.0 billion to $38.4 billion in total revenue and non-GAAP EPS of $21.60 to $23.00, bracketing the Street’s $22.09 EPS estimate and signaling that biosimilar erosion in Prolia and Enbrel will not derail top-line momentum.

Three products, Repatha (a cholesterol-lowering PCSK9 inhibitor), EVENITY (a bone-building therapy for postmenopausal women), and TEZSPIRE (a severe asthma biologic targeting the TSLP inflammatory pathway), each grew over 30% in 2025, collectively demonstrating that Amgen’s growth engine now extends well beyond any single franchise.

On March 28, Phase III VESALIUS-CV subgroup data presented at the ACC showed Repatha cut the risk of a first major cardiovascular event by 31% in high-risk diabetic patients without prior atherosclerosis, reinforcing a primary prevention label position no competing PCSK9 inhibitor currently holds.

Robert Bradway, Chairman and CEO, stated on the Q4 2025 earnings call that “Repatha, olpasiran and MariTide together would represent a very compelling set of cardiometabolic medicines to expand our leadership in the treatment of serious chronic diseases well into the next decade,” anchoring a multi-year growth narrative around three distinct mechanisms in one of medicine’s largest addressable markets.

Amgen’s six Phase III MariTide obesity studies, $2.6 billion in 2026 capital expenditure committed largely to manufacturing scale-up, and UPLIZNA’s 73% sales growth in 2025 across three approved indications position the company to sustain double-digit revenue expansion through the decade, backed by up to $3 billion in share repurchases in 2026.

Wall Street’s Take on AMGN Stock

The Q4 2025 revenue beat of $9.87 billion against a $9.47 billion estimate reframes Amgen as a broad-based compounder, not a single-product story, confirming that the Repatha primary prevention data, UPLIZNA’s 73% sales growth, and IMDELLTRA’s rapid SCLC adoption are already translating into financials.

AMGN’s revenue is estimated to climb from $36.75 billion in 2025 to $37.83 billion in 2026 and $38.76 billion in 2027, supported by Repatha’s expanding primary prevention label following the March 28 VESALIUS-CV subgroup readout and UPLIZNA’s new generalized myasthenia gravis indication launched in December.

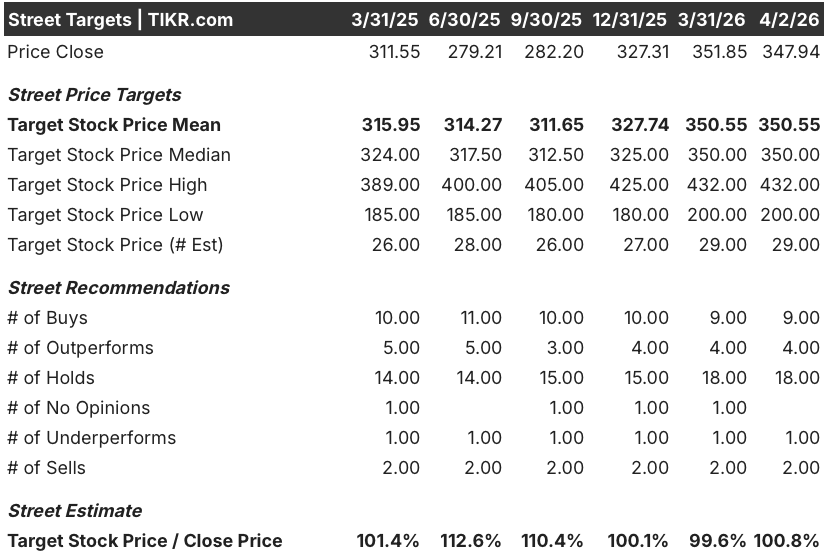

The 29 analysts covering AMGN include 9 buys, 4 outperforms, 18 holds, 1 underperform, and 2 sells, with a mean price target of $350.55, implying roughly 0.8% upside from $347.94 and reflecting a Street divided between near-term biosimilar headwinds and the MariTide option value.

The analyst price target range of $200 to $432 captures the full binary: the low reflects an outcome where Prolia erosion and Tavneos regulatory pressure compound simultaneously, while $432 prices in a clean MariTide Phase III readout from the two fully enrolled chronic weight management studies.

What Does the Valuation Model Say?

TIKR’s mid-case model prices AMGN at $459.52 by December 2030, a 32.1% total return at a 6% annualized IRR, anchored by a 2.9% revenue CAGR and net income margin expansion from 32.1% in 2025 to 34.7% by 2030, driven by Repatha and UPLIZNA scaling into underpenetrated patient populations.

At approximately 15.5x 2026E normalized EPS of $22.38, AMGN trades below its five-year historical forward P/E of roughly 18x to 20x, despite delivering 10.1% EPS growth in 2025 and consensus projecting normalized EPS reaching $24.23 by 2028 — AMGN stock is undervalued relative to the earnings trajectory already in motion.

TIKR’s $459.52 mid-case target is grounded in free cash flow inflecting from $8.1 billion in 2025 to an estimated $13.41 billion in 2026, a 65.6% step-up driven by the $6 billion debt retirement completed in 2025 and $2.6 billion in capital already committed to MariTide manufacturing.

Management confirmed six active MariTide Phase III studies alongside a Phase I for second obesity asset AMG 513, signaling that the pipeline depth behind the 2026 revenue guidance is broader than the Street’s hold-heavy consensus acknowledges.

The FDA’s March 31 safety warning on Tavneos, which generated $459 million in 2025 sales, represents the single development that could compress near-term rare disease portfolio growth if it escalates toward a mandated withdrawal.

The two fully enrolled MariTide chronic weight management Phase III studies, expected to read out in early 2027, are the primary event to watch, with Phase III weight loss magnitude at monthly dosing the number that confirms or breaks the obesity bull case.

Should You Invest in Amgen Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMGN stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amgen Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AMGN stock on TIKR for Free →