Key Stats for Elevance Stock

- 52-Week Range: $273.7 to $458.8

- Current Price: $300.7

- Street High Target: $

What Happened?

Elevance Health (ELV), one of the largest U.S. health insurers and an independent Blue Cross Blue Shield licensee, is navigating a government-mandated enrollment freeze that threatens its Medicare Advantage business while trading at $300.74, more than 34% below its 52-week high of $458.75.

On February 27, the Centers for Medicare and Medicaid Services notified Elevance of its intent to impose intermediate sanctions suspending new enrollment in its Medicare Advantage prescription drug plans, citing non-compliant risk-adjustment data submissions for dates of service prior to April 3, 2023, with the original March 31 effective date later extended to May 30.

Elevance’s Q4 2025 adjusted EPS of $3.33 beat the $3.10 consensus estimate, but the company guided 2026 adjusted EPS to at least $25.50, below the $26.90 analyst estimate, as Medicare Advantage membership is expected to decline in the high teens percentage range and Medicaid operating margins compress to approximately -1.75% amid cost trends running roughly twice historical averages.

The company executed a broad senior leadership overhaul on April 1, appointing Aimée Dailey as president of Government Business, Kristy Duffey as president of Carelon Health, and William Fleming as Carelon chief growth and strategy officer, following CFO Mark Kaye’s February 26 expansion into oversight of Carelon, the company’s health services and pharmacy benefits arm that grew Services revenue nearly 60% and CarelonRx over 20% in 2025.

Moreover, CFO Mark Kaye stated at the Barclays 28th Annual Global Healthcare Conference on March 10 that “our outlook for at least $5.5 billion of operating cash flow gives us the capacity to fully fund dividends and share repurchase activities while continuing to invest in the business,” reaffirming that the CMS matter would not alter capital deployment priorities in 2026.

Elevance’s path to recovery over the next three to five years rests on CEO Gail Boudreaux’s commitment to at least 12% adjusted EPS growth in 2027, $2.3 billion in planned 2026 buybacks, Carelon’s expanding external revenue pipeline, and a Q1 2026 earnings update scheduled for April 22 that management says is already tracking modestly above guidance.

Wall Street’s Take on ELV Stock

The CMS sanctions overhang, which threatens to suspend new Medicare Advantage enrollment through May 30, has accelerated ELV’s selloff to levels that ignore the deliberate repositioning already underway across Medicaid, Medicare, and the individual insurance market.

Carelon, Elevance’s health services and pharmacy benefits arm that grew nearly 60% in services revenue in 2025, supports the TIKR estimate of 13.2% normalized EPS growth in 2027 as affiliated membership headwinds ease and external client momentum compounds.

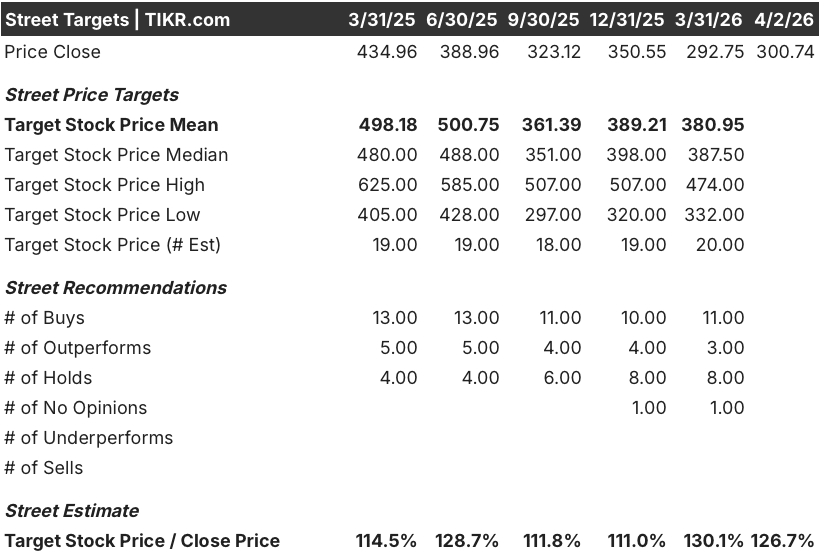

Wall Street has not abandoned the name: 11 buys, 3 outperforms, and 8 holds across 20 analysts point to a mean price target of $380.95, implying 26.7% upside from the April 2 close of $300.74, reflecting confidence in the 2027 recovery thesis.

The $332.00 low target reflects a scenario where CMS sanctions persist beyond May 30 and Medicaid margins remain structurally impaired, while the $474.00 high target prices in a clean regulatory resolution and full execution of the 2027 adjusted EPS growth target of at least 12%.

What Does the Valuation Model Say?

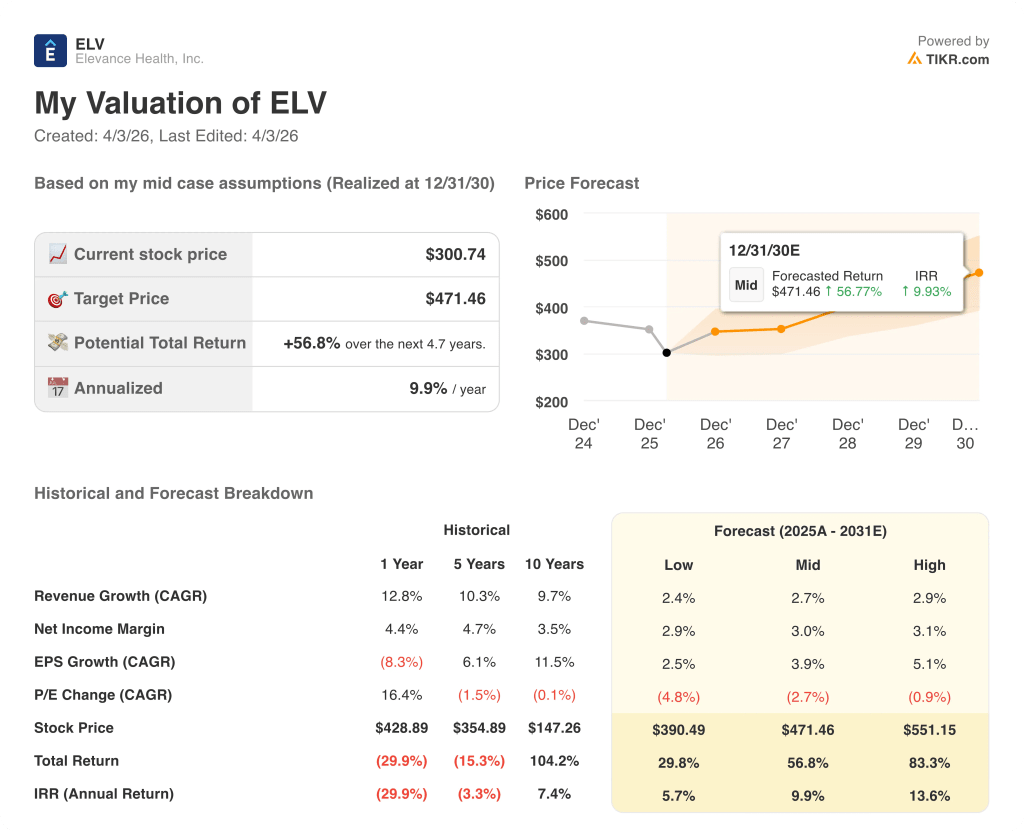

The TIKR mid-case target of $471.46 by December 31, 2030, carrying a 9.9% annualized return, is anchored to a 2.7% revenue CAGR assumption that the $5.5 billion 2026 operating cash flow commitment and Carelon’s expanding external pipeline make credible at current levels.

At 11.6x 2026 estimated normalized EPS of $26.00, ELV trades at a meaningful discount to its own 5-year historical forward P/E of roughly 15x, even as the company guides to at least 12% adjusted EPS growth in 2027, making the ELV stock undervalued relative to its earnings recovery trajectory.

The TIKR model’s $471.46 target depends on EPS rebounding from $26.00 in 2026 to $29.44 in 2027, a move management has already anchored to pricing discipline, Medicare margin improvement to at least 2%, and Carelon’s external growth pipeline.

Kaye’s March 10 reaffirmation that Q1 2026 earnings are tracking modestly above guidance, with Medicare and Medicaid running slightly favorable to initial expectations, confirms the trough narrative is not simply aspirational.

A prolonged CMS sanctions period extending beyond May 30, or a deterioration in Medicaid rate-to-trend alignment, directly breaks the 2027 margin recovery assumption and unwinds the 12% EPS growth target.

The April 22 Q1 2026 earnings release is the first hard test of management’s guidance, with the medical loss ratio, currently targeted at 90.2%, and ACA effectuation rates as the specific numbers to watch.

Should You Invest in Elevance Health, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ELV stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Elevance Health, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ELV stock on TIKR for Free →