Key Stats for Cisco Stock

- 52-Week Range: $52.1 to $88.2

- Current Price: $77.9

- Street High Target: $100

What Happened?

Cisco Systems (CSCO) booked $2.1 billion in AI infrastructure orders from hyperscalers in Q2 FY2026 alone, matching its entire fiscal 2025 total in a single 90-day period, while the stock trades at $77.83.

Cisco reported Q2 revenue of $15.35 billion, beating the IBES estimate of $15.115 billion, with non-GAAP EPS of $1.04 beating the $1.02 consensus, as networking revenue, which covers the routers, switches, and silicon that move data across enterprise and cloud networks, surged 21% to $8.29 billion.

Driving that networking outperformance was Silicon One, Cisco’s proprietary programmable chip architecture that powers both switching and routing in a single platform, with the company shipping its 1-millionth Silicon One chip in Q2 and winning three new hyperscaler use cases during the quarter.

Chuck Robbins, Chair and CEO, stated on the Q2 FY2026 earnings call that “Q2 was a very strong quarter with revenue and earnings per share both growing double digits and coming in above the high end of our guidance ranges,” anchoring a full-year guidance raise to $61.2 billion to $61.7 billion in revenue and non-GAAP EPS of $4.13 to $4.17.

Cisco’s target to take more than $5 billion in AI orders and recognize over $3 billion in AI revenue in FY2026, combined with a campus networking refresh the company calls the top of the first inning, a $10.8 billion remaining buyback authorization, and $43.4 billion in remaining performance obligations, positions the company for compounding revenue and earnings growth well into fiscal 2028 and beyond.

Wall Street’s Take on CSCO Stock

The $2.1 billion in hyperscaler AI orders Cisco booked in a single quarter converts directly into a FY2026 revenue estimate of $61.57 billion, an 8.7% jump that breaks Cisco’s decade-long pattern of low single-digit top-line growth.

Silicon One’s programmable architecture, which lets Cisco adapt its chips to new AI workloads without redesigning hardware, underpins TIKR’s estimate of normalized EPS rising from $4.16 in FY2026 to $4.51 in FY2027, with the $5 billion AI order target and campus refresh cycle providing the two concrete demand drivers behind both numbers.

Fourteen analysts rate CSCO a buy and four rate it outperform, against nine holds and one underperform, with a mean price target of $89.04 implying roughly 14.2% upside from current levels, as the Street prices in accelerating hyperscaler orders and the early innings of a multibillion-dollar campus networking refresh.

The gap between the $75 low target and $100 high target reflects a binary read on gross margin recovery: the low end assumes memory cost inflation persists and the security segment’s Splunk-driven accounting headwind lingers, while the high end prices in price increases taking effect and organic security approaching double-digit revenue growth by Q4 FY2026.

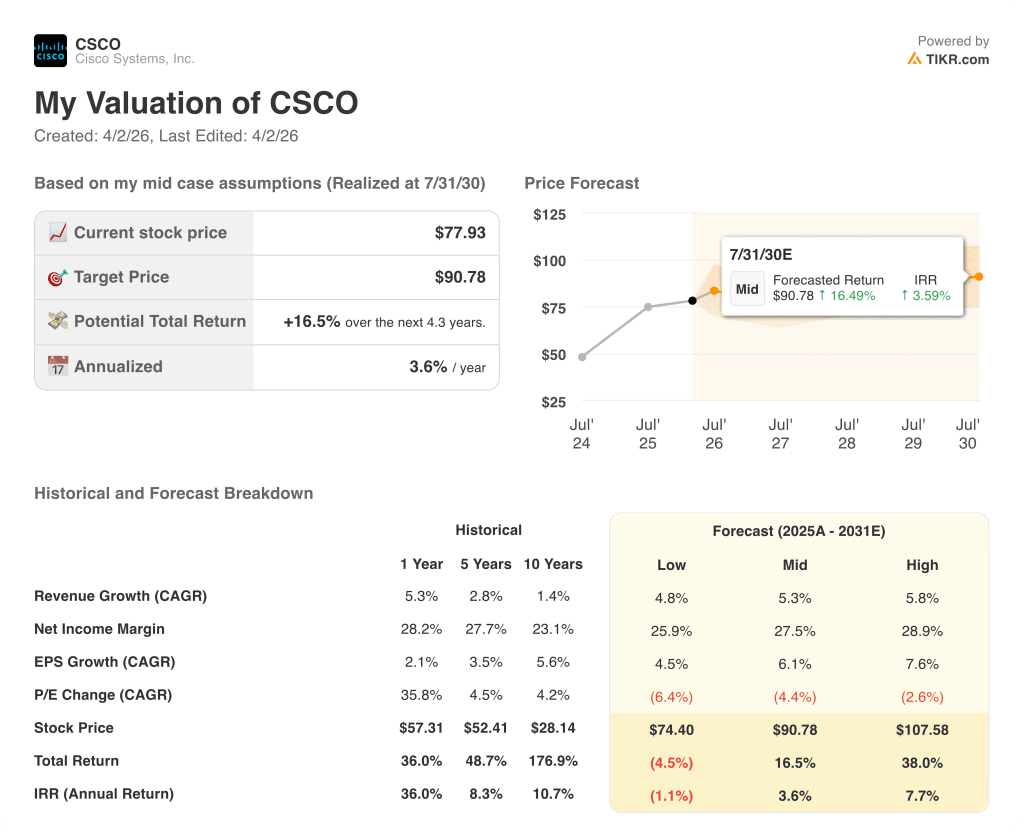

What Does the Valuation Model Say?

TIKR’s mid-case model targets $90.78 by July 2030, anchored to a 5.3% revenue CAGR and a net income margin recovery to 27.5%, both supported by Silicon One gross margin improvements as hyperscaler volumes scale and the campus switching base migrates to higher-margin next-generation platforms.

At 18.7x forward normalized earnings on FY2026E EPS of $4.16, Cisco trades below its five-year historical average forward P/E of roughly 22x, even as its earnings growth rate has accelerated to 9.1% for FY2026, making the CSCO undervalued against its own history at a moment when the underlying business has structurally improved.

The TIKR model’s core growth assumption rests on AI infrastructure revenue exceeding $3 billion in FY2026 and the campus refresh sustaining double-digit order growth, which the Q2 data already confirms, supporting the $90.78 mid-case price target.

Management’s signal that AI orders won’t include G300 or P200 contributions in the current $5 billion FY2026 target means the estimate already carries meaningful upside optionality from new silicon platforms.

If non-GAAP gross margin fails to recover from 67.5% as memory costs persist and security revenue stays negative, the EPS trajectory toward $4.51 in FY2027 breaks.

The Q3 FY2026 earnings call on May 13 is the confirmation event: watch for AI order run rate against the $5 billion annual target and whether the organic security business reaches the guided near-double-digit exit rate.

Should You Invest in Cisco Systems, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CSCO stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cisco Systems, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CSCO stock on TIKR for Free →