Key Takeaways:

- Verizon is in the middle of a turnaround under CEO Dan Schulman, and investors are focusing on subscriber growth, broadband expansion, and balance sheet discipline.

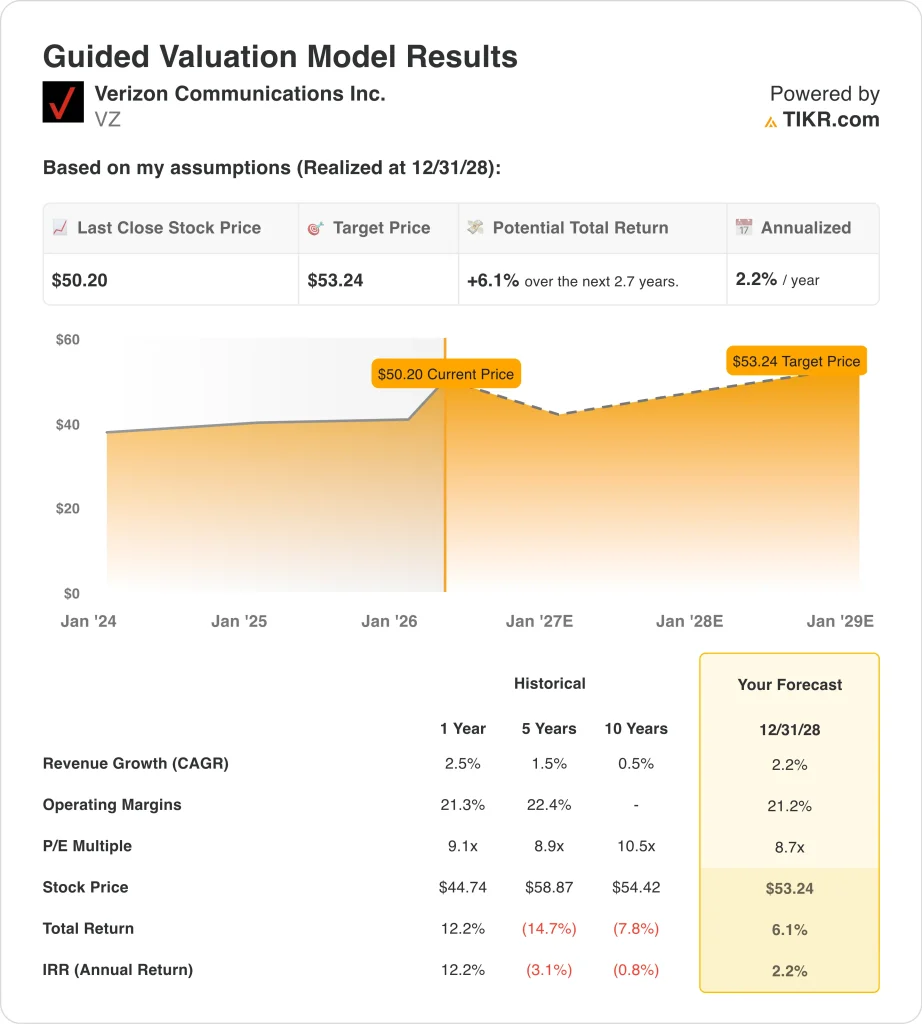

- Verizon stock could reasonably reach $53 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 6.1% from today’s price of $50, with an annualized return of 2.2% over the next 2.7 years.

What Happened?

Verizon Communications (VZ) has become more relevant this quarter because the market is reassessing its turnaround story. The stock is up 25.4% over the past three months, and that move has come as investors respond to better subscriber trends, stronger broadband adds, and a more optimistic tone from new management.

At the same time, the shares now trade much closer to Wall Street’s average target, so the debate has shifted from whether Verizon was cheap to whether most of the near-term improvement is already reflected in the price.

The fourth-quarter results helped drive that change in tone. Verizon reported 616,000 postpaid phone net additions, its best fourth quarter for that metric since 2019, along with 372,000 broadband net additions and 319,000 fixed wireless access net additions.

Wireless service revenue rose 1.1% to $21.0 billion, and management said 2026 should deliver a “step function improvement” in key metrics, with guidance for 750,000 to 1 million consolidated postpaid phone net adds.

Investors are also watching the leadership and strategic reset. Reuters reported in February that consumer chief Sowmyanarayan Sampath would step down as Verizon mounted a turnaround under Dan Schulman, and Schulman later said at Morgan Stanley that the company would focus on stronger customer value, disciplined growth, and deleveraging after the Frontier acquisition.

Here’s why Verizon stock could still move higher from here, but also why the valuation now looks much less compelling than it did before the recent rally.

What the Model Says for Verizon Stock

We analyzed the upside potential for Verizon stock using valuation assumptions based on its stable wireless franchise, improving broadband momentum, and mature telecom valuation profile.

Based on estimates of 2.2% annual revenue growth, 21.2% operating margins, and a normalized P/E multiple of 8.7x, the model projects Verizon stock could rise from $50 to $53 per share.

That would be a 6.1% total return, or a 2.2% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for VZ stock:

1. Revenue Growth: 2.2%

Verizon’s revenue outlook is steady, but it is not especially strong. Revenue rose 2.5% in 2025 to $138.2 billion, and management said Mobility and Broadband service revenues should grow 2% to 3% in 2026, even as the company laps prior price increases. That kind of forecast fits a mature telecom operator with recurring revenue, but it also limits how much valuation expansion investors can justify.

The growth story is really about the mix, not a dramatic acceleration. Fixed wireless access subscribers rose above 5.7 million by the end of the fourth quarter 2025, and Verizon said it now has more than 16.3 million fixed wireless and fiber broadband connections after closing Frontier.

Still, Verizon is not a high-growth telecom business. The company’s own long-term numbers show only limited top-line expansion, and the stock’s recent move has already priced in a better 2026 trajectory. Based on analysts’ consensus estimates, we use a 2.2% revenue growth forecast, which aligns with management’s service revenue outlook and the company’s mature position in U.S. telecom.

2. Operating Margins: 21.2%

Margins remain one of Verizon’s biggest strengths. Operating margin was 22.9% in 2025, and the guided valuation uses a 21.2% operating margin assumption through 2028, which is slightly below the latest level. That reflects a business with durable scale, but also one that still faces integration costs, ongoing network investment, and competitive pressure in wireless promotions.

The company continues to generate large cash flows despite its heavy capital needs. Verizon produced $37.1 billion of operating cash flow in 2025 and $20.1 billion of free cash flow, while management has emphasized efficiency and better capital allocation under the new leadership team. Schulman also said at Morgan Stanley that he intends to grow adjusted EPS and free cash flow over time through efficiency improvements and top-line growth.

There is still some margin risk from execution and integration. Verizon’s interest expense remains high, and the Frontier acquisition adds both opportunity and integration complexity. Based on analysts’ consensus estimates, we use a 21.2% operating margin assumption, which gives credit for Verizon’s scale and cash generation but does not assume a major jump from current profitability.

3. Exit P/E Multiple: 8.7x

Verizon’s valuation is the clearest reason the model looks restrained. The guided valuation uses an 8.7x exit P/E multiple, which is below the stock’s 1-year, 5-year, and 10-year historical multiples shown in the model. That makes sense for a slower-growth telecom name, but it also means there is less room for multiple expansion to drive returns from today’s price.

The market already values Verizon as a stable income stock more than a growth story. The shares offer a dividend yield of about 5.6%, and the payout ratio is 66.9%, which helps support the stock but also tells investors that much of the appeal is already tied to income rather than rapid earnings growth.

The recent rally reinforces that point. Verizon now trades very close to the current average street price target of about $51, so analysts broadly see limited near-term upside after the recent move.

Based on analysts’ consensus estimates, we maintain an 8.7x exit multiple because Verizon remains a mature telecom franchise with dependable cash flow, but not the kind of growth profile that typically commands a much richer multiple.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

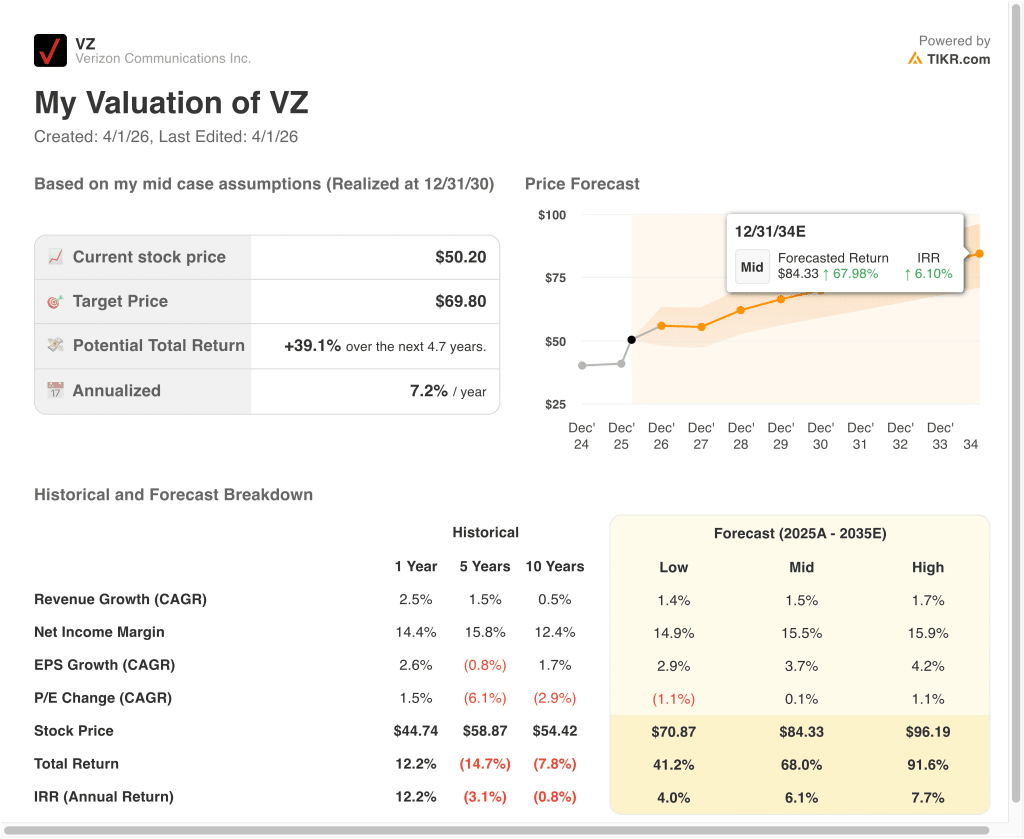

Different scenarios for Verizon stock through 2035 show varied outcomes based on wireless growth, broadband execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: Wireless competition stays intense, and growth remains sluggish → 4.0% annual returns

- Mid Case: Verizon steadily grows mobility and broadband while protecting margins → 6.1% annual returns

- High Case: Broadband, subscriber growth, and cash flow improve faster than expected → 7.7% annual returns

Even in the optimistic case, Verizon’s projected returns remain modest. That is an important signal because the stock has already rallied sharply, and the valuation model suggests the easy recovery may have already happened. In other words, Verizon still looks stable, but it does not look especially mispriced on these assumptions.

Looking ahead, Verizon stock will likely be focused on a few clear markers. Investors will want to hear on the April 21 earnings call whether postpaid phone adds, broadband growth, and Frontier integration are tracking management’s goals for 2026.

If Verizon keeps improving operations and reducing leverage, the stock can remain resilient, but the current model suggests future gains may depend more on execution than on simple rerating.

See what analysts think about VZ stock right now (Free with TIKR) >>>

Should You Invest in Verizon Communications Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VZ, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track VZ alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Verizon Communications stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!