Key Stats for American Express Stock

- Past-Week Performance: +2.2%

- 52-Week Range: $220.4 to $387.5

- Current Price: $297.5

What Happened?

American Express (AXP) secured the NFL’s official payments partnership on March 30, replacing Visa after its three-decade sponsorship ended, as the payments network trades at $299.11 with a 52-week range of $220.43 to $387.49 that frames how much ground the stock has already traveled.

The NFL deal, announced March 31 and effective with the 2026 season, immediately unlocks presale access for Amex cardholders to the September 10 Rams-49ers game in Melbourne, while the company simultaneously launched the $295-annual-fee Graphite Business Card on March 25, expanding its commercial card lineup with 2% cashback on eligible purchases and 5% on travel booked through its platform.

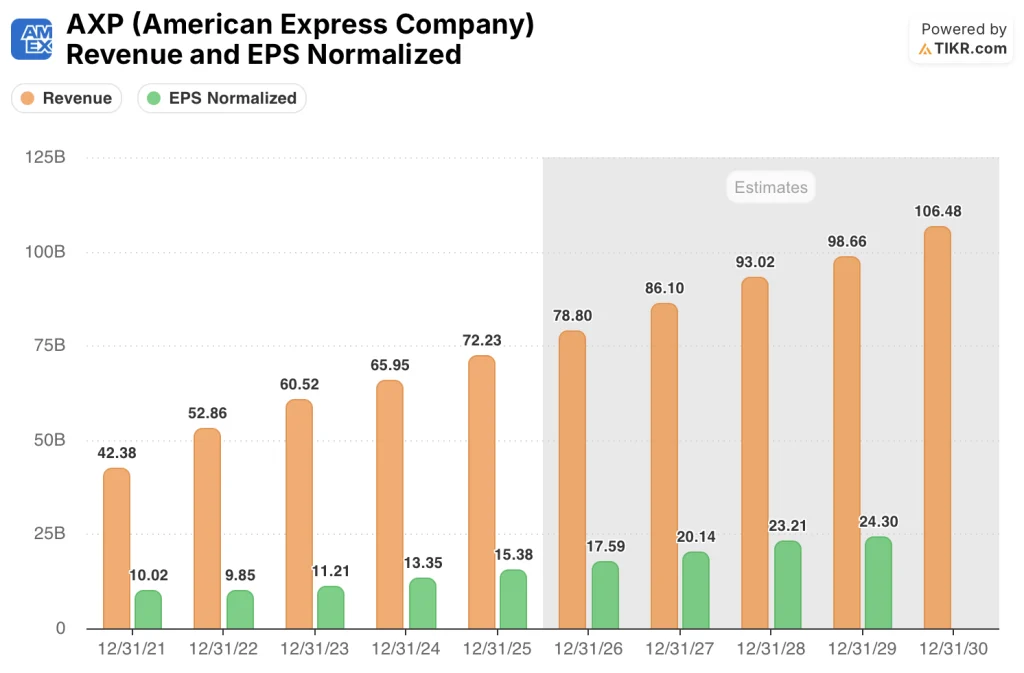

The NFL partnership lands on top of a business already generating $72.2 billion in full-year 2025 revenue, up 10%, with net card fees hitting a record $10 billion after 30 consecutive quarters of double-digit growth, a streak no major U.S. card issuer has matched.

On January 30, CFO Christophe Le Caillec stated on the Q4 2025 earnings call that “the Platinum card, this refresh, is more successful than what we saw with Gold or what we saw with Delta,” tying directly to travel bookings surging 30% in Q4 and Resy restaurant spend rising 20% as cardholders engaged with the relaunched value proposition.

A planned NFL Extra Points credit card, the ACE agentic commerce developer kit launching in April, the Center expense management platform rolling out by mid-2026, and $17.30 to $17.90 in guided 2026 EPS together form the clearest multi-year compounding case in the large-cap payments sector.

Wall Street’s Take on AXP Stock

The NFL deal, which replaces Visa’s three-decade sponsorship and takes effect with the 2026 season, immediately extends the Platinum value proposition — the card’s core spend-driving engine — into the world’s most valuable sports property, reinforcing the card fee growth trajectory already running at 16% as of Q4.

As TIKR estimates, revenue grows from $72.2 billion in 2025 to $78.8 billion in 2026 and $86.1 billion in 2027, with the Platinum back-book repricing, NFL presale access, and Center’s expense management launch providing the specific business-level support behind those numbers.

Normalized EPS rises from $15.38 in 2025 to $17.59 in 2026 and $20.14 in 2027 as TIKR estimates, a 14.4% two-year CAGR driven by the card fee acceleration Squeri guided toward high teens by year-end.

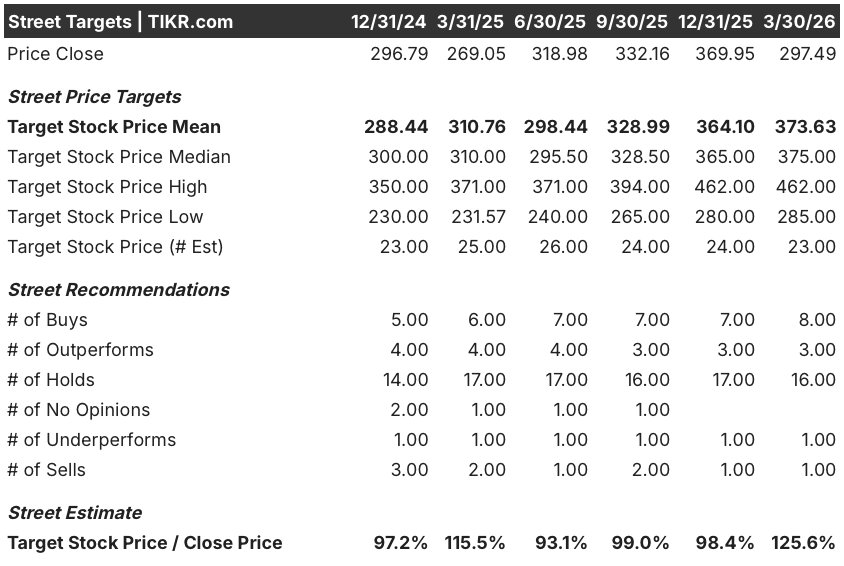

Conviction among analysts has quietly shifted: 8 buys and 3 outperforms now outnumber 1 underperform and 1 sell across 23 tracked estimates, with a mean price target of $373.63 implying 25.6% upside from the March 30 close of $297.49.

The gap between the $285.00 analyst floor, which prices in macro softness and VCE ratio pressure from Platinum benefits uptake, and the $462.00 ceiling, which rewards sustained EPS compounding above 14%, hinges on whether card fee growth exits 2026 in the high teens as guided.

What Does the Valuation Model Say?

At $297.49, AXP trades at roughly 16.9x TIKR’s 2026E normalized EPS of $17.59, a meaningful discount to its own 5-year EPS CAGR of 32.5% and well below the premium the network’s closed-loop economics have historically commanded.

The TIKR mid-case target of $495.31 implies a 66.5% total return and 11.3% annualized IRR through December 2030, driven by a 7.7% revenue CAGR and 10.5% EPS CAGR anchored to the Platinum refresh, NFL partnership monetization, and Center commercial launch, yet AXP trades at just 16.9x forward earnings despite EBITDA margins expanding from 28.8% to 34.7%, making the stock undervalued at current levels.

Moreover, Caillec’s confirmation on the Q4 call that Platinum retention is running at 99% for consumer and 98% for small business as repricing begins signals the earnings model’s most vulnerable assumption — fee revenue attrition — is holding.

The single largest risk to the model is a deterioration in middle-market commercial spend, which Squeri flagged as already softer, threatening the Center-driven commercial revenue contribution the 2026 estimate assumes.

April 23 Q1 2026 earnings is the first hard data point confirming whether card fee growth is tracking toward high teens and whether the NFL partnership is converting to measurable presale and spend engagement.

Should You Invest in American Express Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AXP stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track American Express Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AXP stock on TIKR for Free →