Key Stats for Sherwin-Williams Stock

- Past-Week Performance: -5.8%

- 52-Week Range: $301.6 to $379.7

- Current Price: $315.4

What Happened?

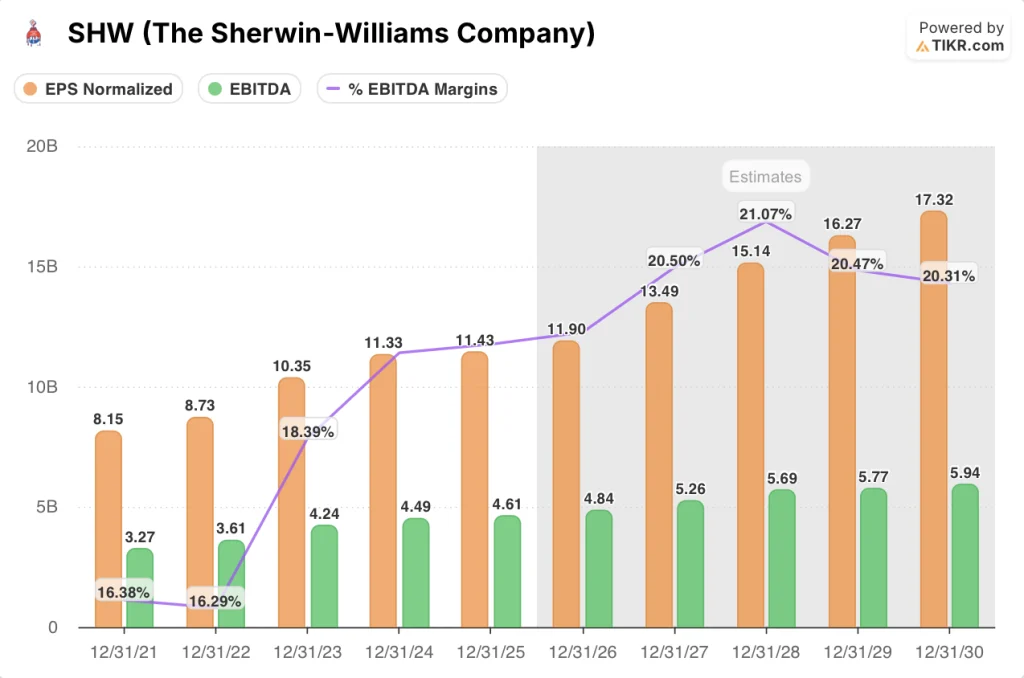

Sherwin-Williams (SHW), the U.S. paint and coatings giant with 4,853 retail stores serving professional contractors and DIY customers, delivered record adjusted diluted earnings per share of $11.43 in FY 2025 even as housing demand stayed frozen, with shares trading at $315.37 against a 52-week high of $379.65.

The Q4 2025 earnings call confirmed full-year net sales of $23.57B, up 2.1%, anchored by Paint Stores Group revenue of $13.61B, up 3.2%, while a 7% price increase took effect January 1 across the company’s professional paint retail network.

Operating cash flow reached $3.45B, up 9.4% and equal to 14.6% of net sales, as Q4 adjusted EBITDA margin expanded 120 basis points to 17.7%, outpacing peers in a coatings sector where volume growth remained broadly negative through year-end.

Heidi Petz, Chair, President and CEO, stated on the Q4 2025 earnings call that “for the third year in a row, the market is not going to give us much help, and for the third year in a row, we expect to outperform the market and grow sales and earnings per share,” underscoring the company’s share-gain strategy amid persistent housing softness.

The October 2025 acquisition of Suvinil, Brazil’s leading paint brand, added $164.5M in Consumer Brands revenue immediately, while a pending board-approved dividend increase to $3.20 per share would mark the 48th consecutive annual raise, and FY 2026 adjusted EPS guidance of $11.50 to $11.90 signals continued earnings growth even as management targets 80 to 100 net new U.S. stores and a $46M cost savings program.

Wall Street’s Take on SHW Stock

The record $11.43 adjusted EPS SHW posted in FY 2025 gains further weight when mapped against the revenue trajectory: sales grew only 2.1% that year, yet TIKR estimates EPS accelerates to $11.90 in FY 2026 and $13.49 in FY 2027, as pricing and cost leverage do the work volume refuses to do.

Underpinning that earnings ramp, EBITDA is forecast to grow from $4.61B in FY 2025 to $5.26B in FY 2027, with EBITDA margin expanding from 19.6% to 20.5%, a structural shift reflecting the 7% January price increase and the $46M cost savings program.

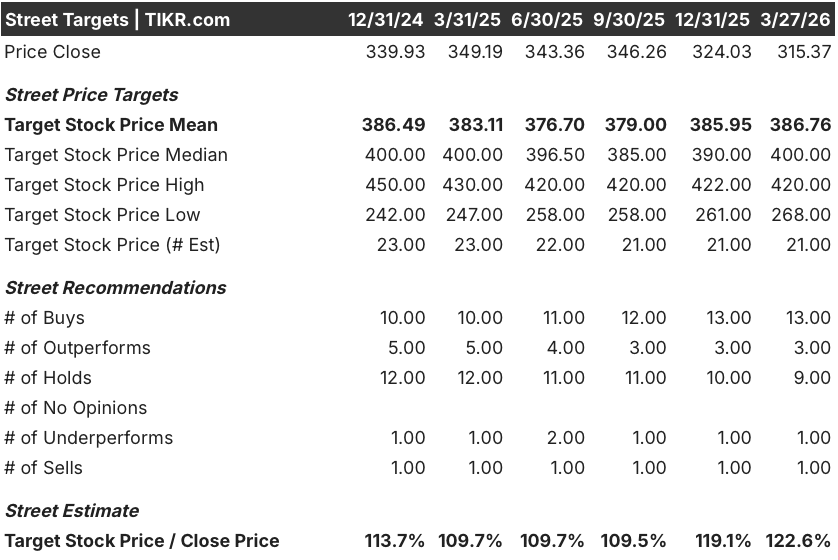

Sixteen analysts carry buy or outperform ratings on SHW against just nine holds and two negatives, with a mean price target of $386.76, implying 22.6% upside from the March 27 close of $315.37, reflecting growing conviction that the share-gain cycle has further to run even without a housing recovery.

The spread between the $268.00 analyst low and the $420.00 high captures precisely the fork in the road: the bear case rests on prolonged mortgage-rate lock-in suppressing existing home sales, while the bull case prices in the Suvinil acquisition’s Brazil footprint and the January 7% price increase delivering low single-digit full-year realization.

What Does the Valuation Model Say?

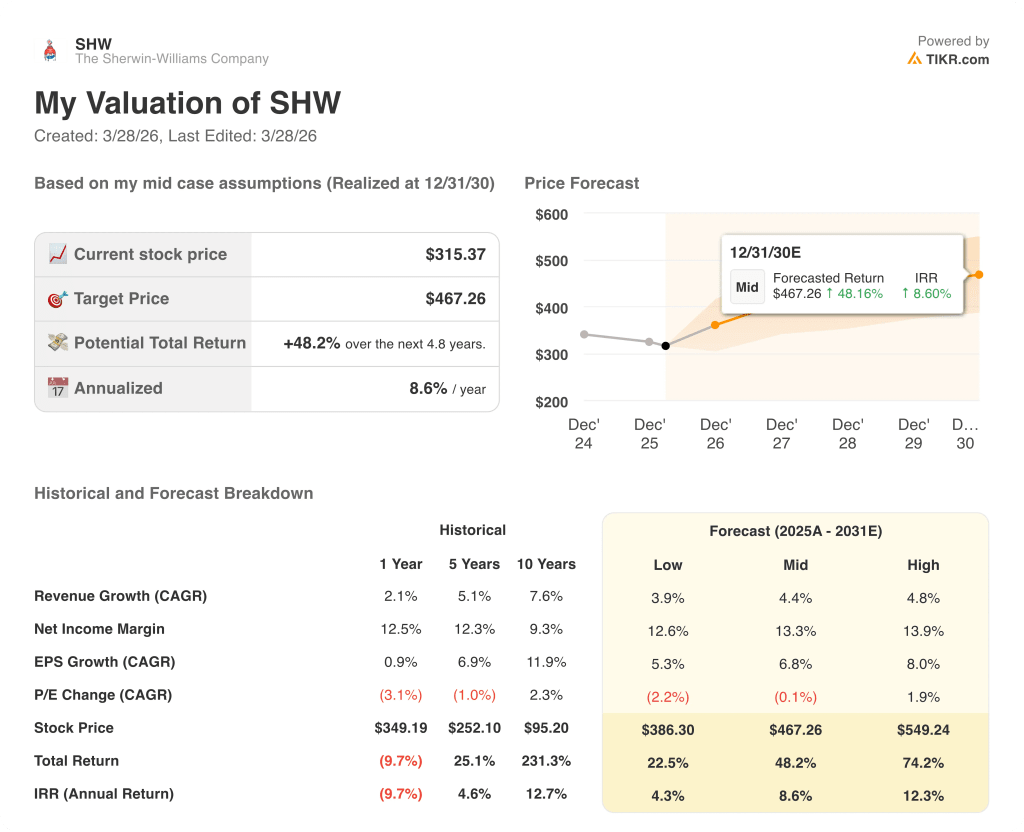

TIKR’s mid-case model targets $467.26 by December 2030, implying a 48.2% total return and an 8.6% IRR, driven by a 4.4% revenue CAGR and net income margin expansion from 12.1% to 13.3%, assumptions grounded directly in SHW’s 80-to-100 annual new store program and accelerating Packaging division non-BPA coating conversions.

The market prices SHW as a housing-cycle stock; the FY 2025 free cash flow of $2.65B, up 27.4% in a year of flat volume, suggests the business compounds regardless of when existing home sales recover.

Meanwhile, four straight years of 80-plus net new stores, a $46M cost savings program, and Suvinil’s $164.5M revenue contribution directly support TIKR’s 4.4% revenue CAGR; TIKR’s mid-case target of $467.26 reflects that compounding, not a housing recovery.

Moreover, Petz’s January 29 commitment to outperform the market for a third consecutive year, backed by 87 net new sales territories added in FY 2025 alone, confirms execution, not narrative.

Persistent mortgage-rate lock-in suppressing existing home sales remains the single input that breaks TIKR’s 4.4% revenue CAGR assumption; if turnover stalls further, the Paint Stores Group’s flat-to-down single-digit Q1 guidance becomes the full-year ceiling.

The September 24 Financial Community Presentation in Cleveland is the next hard date to watch; the number to track is full-year price realization against the 7% January increase, the lever that determines whether FY 2026 adjusted EPS hits the $11.70 midpoint or stalls near the $11.50 floor.

Should You Invest in The Sherwin-Williams Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SHW stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Sherwin-Williams Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze X stock on TIKR for Free →