Key Takeaways:

- Adobe is still delivering strong growth, high margins, and large free cash flow, but the stock is priced more cautiously as investors want clearer evidence that Adobe’s AI products can defend its moat.

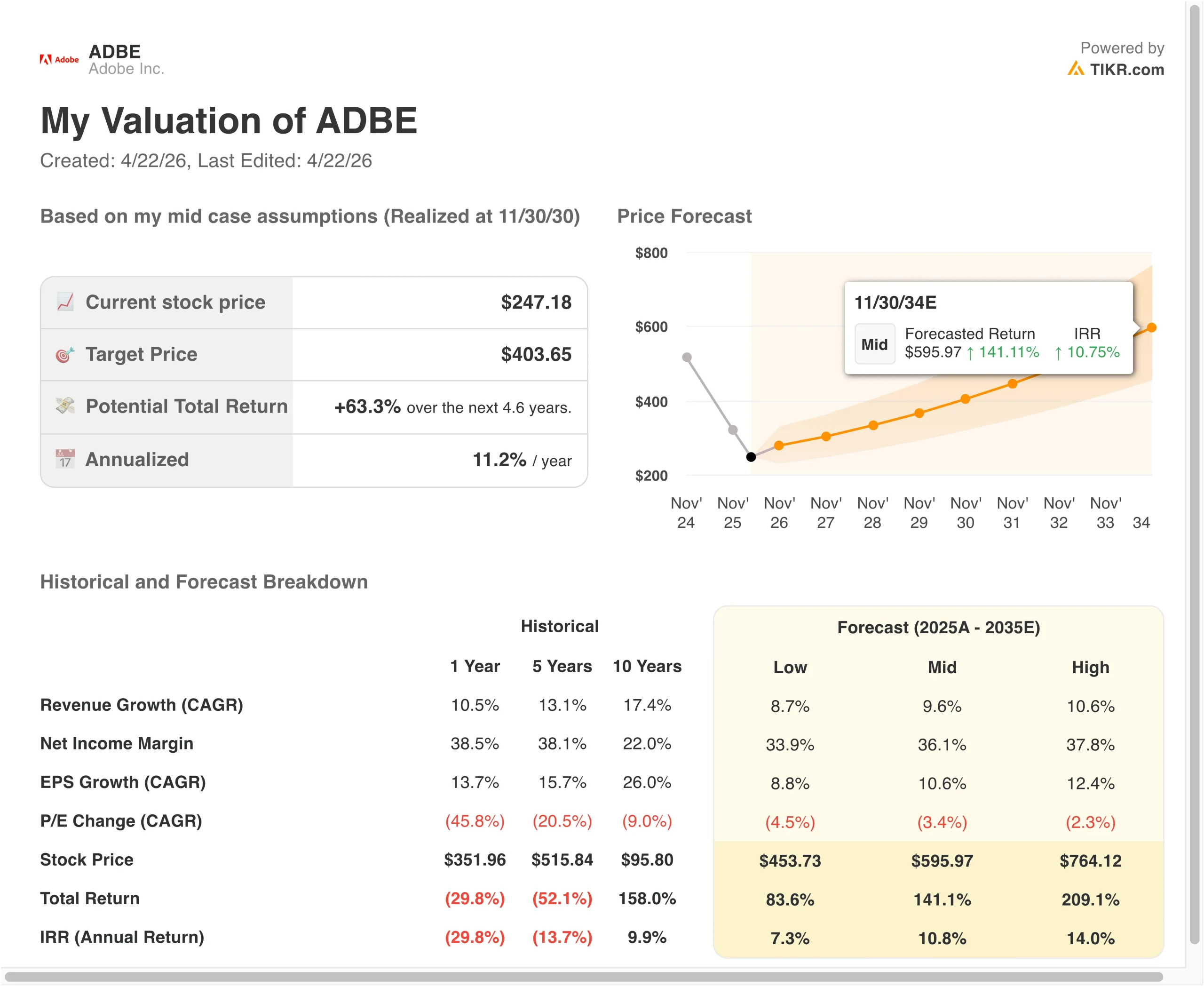

- Adobe stock could reasonably reach $325 per share by late 2028, based on the valuation model.

- That implies a 31.4% total return from today’s price of $247, or 11.0% annualized over the next 2.6 years.

What Happened?

Adobe Inc. (ADBE) is relevant right now because investors are trying to separate strong operating results from rising fears of AI disruption. On April 21, Adobe announced a new $25 billion stock repurchase program that runs through April 30, 2030, and Reuters said the move was meant to reassure investors about the company’s long-term value creation.

A day earlier, Adobe launched new AI products for enterprise customers at Adobe Summit. Reuters reported that Adobe introduced CX Enterprise, Brand Intelligence, and expanded GenStudio tools to help clients automate and personalize marketing work.

The company’s latest earnings report gave investors reasons to stay constructive on the business itself. Adobe reported record Q1 FY2026 revenue of $6.4 billion, non-GAAP EPS of $6.06, and record Q1 cash flow of $2.96 billion, while management guided Q2 revenue to $6.43 billion to $6.48 billion.

CFO Dan Durn said Adobe delivered “record Q1 cash flow of $2.96 billion,” which helps explain why management has been so aggressive with repurchases.

There is also a broader strategic backdrop behind the stock. Adobe announced in November 2025 that it would acquire Semrush for about $1.9 billion, and Germany’s Bundeskartellamt said in March 2026 that it had cleared the deal in the first phase of review.

Here’s why Adobe stock could keep moving sharply from here: investors are watching whether new AI tools, enterprise adoption, and capital returns can offset fears that design workflows are becoming more automated and more competitive.

What the Model Says for Adobe Stock

We analyzed the upside potential for Adobe stock using valuation assumptions tied to its recurring revenue base, strong profitability, and the lower multiple the market is now willing to pay.

Based on estimates of 9.3% annual revenue growth, 44.5% operating margins, and a normalized P/E multiple of 10.3x, the model projects Adobe stock could rise from $247 to $325 per share.

That would be a 31.4% total return, or an 11.0% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ADBE stock:

1. Revenue Growth: 9.3%

Adobe has expanded revenue from $15.8 billion in fiscal 2021 to $23.8 billion in fiscal 2025. That growth came while the company kept gross margin near 89%, which is rare at this scale. It tells us Adobe is still growing within a very high-quality software model.

The business mix also helps explain why revenue has remained durable. Adobe said fiscal 2025 Digital Media revenue rose 11% to $17.65 billion, while Digital Experience revenue rose 9% to $5.86 billion. That means growth is not coming from a single product cycle, but from a broader platform spanning creative tools, documents, and enterprise marketing software.

Q1 FY2026 showed that momentum continued into the new year. Revenue rose 12% year over year, subscription revenue rose 13%, and total ARR exited the quarter at $26.06 billion.

Based on analysts’ consensus estimates, we use a 9.3% revenue growth assumption because it lines up with Adobe’s recent growth pace, its recurring revenue base, and a more measured market view of software demand.

2. Operating Margins: 44.5%

Adobe is already operating from a position of strength. The company posted an operating margin of 36.6% in fiscal 2025, and its business model continues to benefit from digital delivery, pricing power, and a large installed base. That gives Adobe room to keep converting revenue growth into earnings even while it invests in AI.

Management’s near-term guidance also supports a high-margin view. In the Q1 FY2026 earnings call materials, Adobe said it was targeting a Q2 FY2026 non-GAAP operating margin of about 44.5%.

There is still a reason not to be too aggressive here. Adobe is spending to defend leadership across creativity, documents, and customer experience, and the company is moving quickly to launch new AI products as competition heats up.

Based on analysts’ consensus estimates, we use 44.5% operating margins because that matches management’s near-term framework and reflects Adobe’s software economics without assuming a major margin breakout.

3. Exit P/E Multiple: 10.3x

The exit multiple is the most conservative part of the model. Adobe currently trades at about 14.4x earnings, while the guided valuation uses a 10.3x normalized P/E. That means the model is not assuming investors suddenly return to paying a premium growth multiple for the stock.

That caution reflects the market narrative around Adobe today. Reuters reported that investors have pressed Adobe for clearer returns from its AI strategy, while new autonomous design tools and AI-native rivals have raised questions about how durable Adobe’s historical pricing power will be.

A lower exit multiple is a reasonable way to capture that uncertainty without assuming the business itself stops growing.

There is also support for staying disciplined because Adobe is using capital returns to offset dilution and reduce share count over time. Adobe’s new repurchase program authorizes up to $25 billion through April 2030, and the company repurchased roughly 8.1 million shares in Q1 alone.

Based on analysts’ consensus estimates, we maintain a 10.3x exit P/E because Adobe remains a strong franchise, but the market is clearly asking for more proof before assigning a higher multiple again.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for Adobe stock through 2035 show varied outcomes based on AI adoption, margin durability, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: AI monetization is slower, margins settle lower, and the multiple compresses faster -> 7.3% annual returns

- Mid Case: Adobe keeps compounding across Creative Cloud, Document Cloud, and Experience Cloud -> 10.8% annual returns

- High Case: AI products gain broader traction, growth stays stronger, and earnings compound faster -> 14.0% annual returns

Going forward, Adobe stock will probably move with a mix of earnings proof, AI product traction, and multiple disciplines. The business is still generating strong growth, high margins, and significant cash, but the market wants clearer evidence that Adobe’s AI investments can defend its leadership and create new revenue streams.

See what analysts think about ADBE stock right now (Free with TIKR) >>>

Should You Invest in Adobe Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ADBE, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ADBE alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Adobe stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!