Key Stats for Boston Scientific Stock

- 52-Week Range: $59 to $110

- Current Price: $60

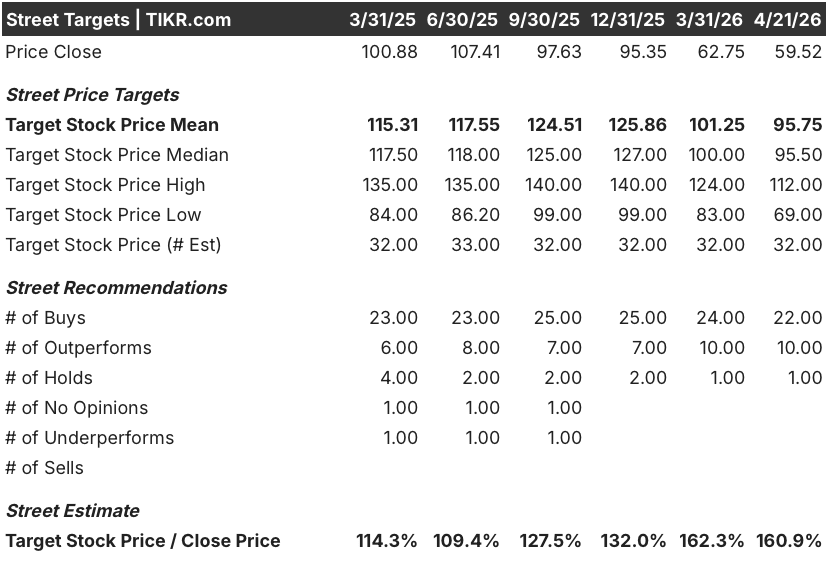

- Street Mean Target: $96

- Street High Target: $112

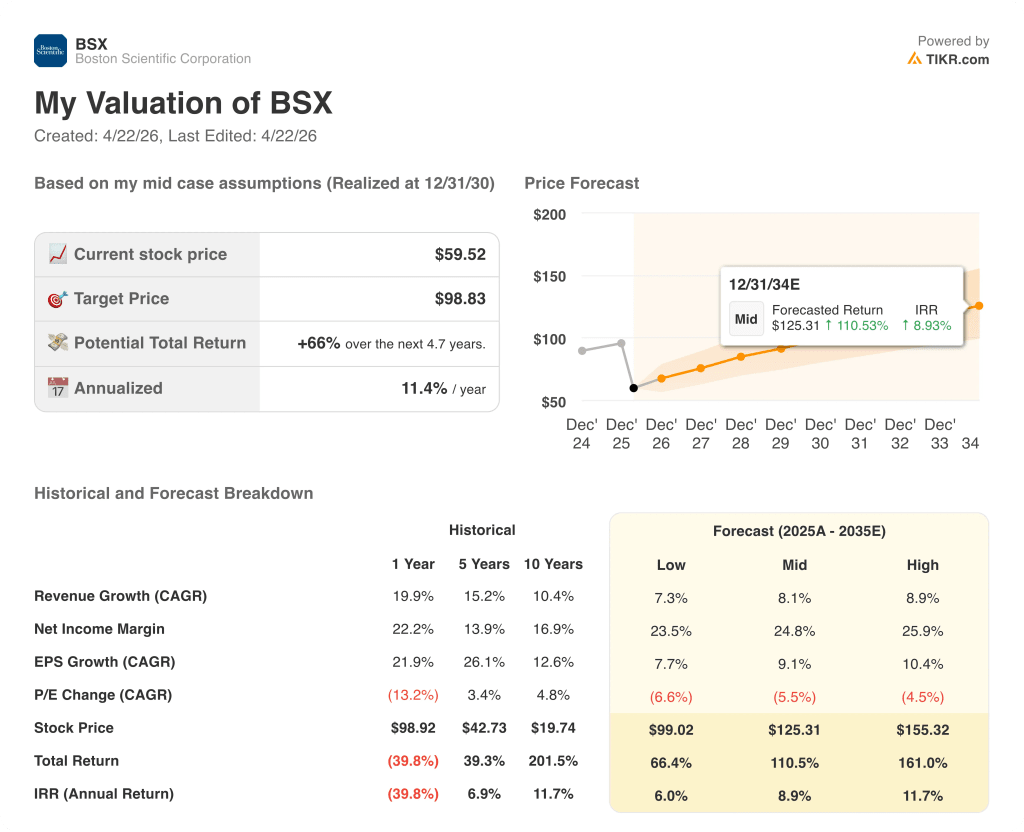

- TIKR Model Target (Dec. 2030): $100

What Happened?

Boston Scientific (BSX), the Marlborough, Massachusetts-based medical device company whose portfolio spans cardiac electrophysiology, structural heart, interventional oncology, and neuromodulation, delivered full-year 2025 revenue of $20.07 billion and adjusted EPS of $3.06, marking the third consecutive year of 20%-plus earnings growth.

The stock fell roughly 17.5% on February 4 after Q4 results revealed that U.S. electrophysiology sales, the segment that houses FARAPULSE, its market-leading pulse field ablation catheter used to treat atrial fibrillation, grew slower than the Street had modeled, and 2026 guidance of 10% to 11% organic growth came in well below the 25% EP growth rate some analysts had assumed.

What the selloff obscured is that 32 of 33 covering analysts still rate Boston Scientific stock a buy or outperform, and the mean price target of $96 implies 61% upside from current levels, a gap driven almost entirely by one question: whether FARAPULSE can maintain clear PFA market leadership as Johnson & Johnson and Medtronic bring competing pulse field ablation catheters to market.

The answer arrived at the American College of Cardiology meeting on March 28, when Boston Scientific presented CHAMPION-AF trial results showing that WATCHMAN FLX, its left atrial appendage closure device used to prevent stroke in atrial fibrillation patients, met both primary endpoints against novel oral anticoagulants: noninferior for stroke prevention and superior for clinically meaningful bleeding reduction over 36 months.

Mike Mahoney, Chairman and CEO, stated on the Q4 2025 earnings call that “our ’26 guidance, along with our ’26 to ’28 goals of sales growing 10% plus, adjusted operating margin expansion of 150 basis points and leveraged double-digit EPS growth continue to be highly differentiated,” tying the long-range plan directly to a pipeline that now includes the CHAMPION label expansion, the $14.9 billion Penumbra acquisition bringing neurovascular and mechanical thrombectomy capabilities to Boston Scientific, and FARAWAVE Ultra, the next-generation PFA platform expected to launch in the first half of 2027.

Wall Street’s Take on BSX Stock

The CHAMPION-AF result changes the duration of the WATCHMAN growth story more than it changes 2026 numbers: management confirmed the data supports their previously stated 20% annual WATCHMAN market growth through the long-range plan.

The longer-term prize, expanding the indicated patient population from 5 million today to 20 million globally, will require an FDA label update, consensus guideline revisions, and a CMS national coverage decision that management acknowledged will take time to work through.

Boston Scientific’s normalized EPS is expected to reach around $3.45 in FY2026, a 13% increase year-over-year driven by continued EP and WATCHMAN growth, Penumbra integration synergies on the commercial side outside the U.S., and 50 to 75 basis points of adjusted operating margin expansion.

That foundation compounds further into FY2027, where consensus sees EPS reaching around $3.90 as the AXIOS stent removal headwind and ACURATE discontinuation roll off and the full pipeline from neuromodulation, interventional oncology, and ICVT begins to contribute.

Twenty-two buy ratings and 10 outperforms against a single hold position — the most concentrated bullish consensus in large-cap medtech — reflect a Street that views the EP share loss as temporary and the CHAMPION catalyst as transformational, with the high target of $112 representing roughly 88% upside and the mean of $96 still implying 61% from current levels.

Trading at roughly 17x forward earnings against 13% normalized EPS growth and a revenue base expanding toward $22 billion in FY2026, Boston Scientific stock appears deeply undervalued, priced as if the EP deceleration is permanent when every clinical data point from CHAMPION to FARAPOINT approval to FARAWAVE Ultra’s pipeline suggests the opposite.

The one risk that could keep the stock range-bound near term is the securities class action lawsuit filed by multiple firms alleging misleading statements about U.S. EP segment sustainability between July 2025 and February 2026, with a lead plaintiff deadline of May 4: even a frivolous case creates a headline overhang that slows institutional re-entry.

The next hard catalyst is today’s Q1 2026 results, scheduled for release April 22 before the open, with the conference call at 8:00 a.m. ET: watch for U.S. EP organic growth to confirm whether the Q4 sequential softness has stabilized, and whether management revises the 10% to 11% full-year organic guide upward or holds it steady given the AXIOS and ACURATE transient headwinds.

What Does the Valuation Model Say?

TIKR’s mid-case model targets around $99 per share by December 2030, anchored to roughly 9% annualized EPS growth and a net income margin expanding toward 25%, but the model was built before CHAMPION-AF trial data confirmed WATCHMAN’s potential first-line label expansion to 20 million eligible patients globally, a catalyst that is not yet reflected in consensus estimates and that management has said will sustain 20% WATCHMAN market growth through 2028.

Priced at 17x forward earnings against a three-year long-range plan guiding to 10%-plus organic revenue growth, 150 basis points of cumulative operating margin expansion, and 13% EPS compounding, Boston Scientific stock is undervalued by a margin that implies the market is treating a temporary EP share loss as a structural impairment of the entire franchise.

Everything in the bull case depends on whether EP holds market leadership through 2026 and whether WATCHMAN can begin to benefit from expanded first-line positioning before competitors close the clinical gap.

Bull Case — The Compounder Trading at a Broken Multiple

- Normalized EPS expected to reach around $3.45 in FY2026 (+13%) and around $3.90 in FY2027 (+13%), compounding at a rate that historically supported 30–35x forward multiples for BSX; re-rating to even 25x FY2026 EPS implies a stock price near $86

- CHAMPION-AF met both primary endpoints, positioning WATCHMAN FLX for a label expansion from 5 million to 20 million indicated patients globally; management confirmed submission to FDA is underway and guideline update process has begun with professional societies

- Penumbra acquisition ($14.9 billion) adds neurovascular and mechanical thrombectomy, two high-growth segments where Boston Scientific had no presence, with closing expected in 2026 and meaningful OUS scale synergies through BSX’s existing EMEA and Asia-Pacific commercial infrastructure

- FARAWAVE Ultra, the third-generation PFA platform, is on track for a first-half 2027 launch with what management described as significant upgrades in capability, delivery, and tracking versus the current FARAWAVE device

- FCF expected to reach around $4.2 billion in FY2026 (80% conversion target), providing capital allocation flexibility for continued tuck-in M&A even as the Penumbra term loan is being drawn

Bear Case — EP Share Loss and Legal Overhead

- U.S. EP organic growth is expected to decelerate toward 10% in 2026 as Johnson & Johnson and Medtronic PFA catheters launch, compressing what was a near-monopoly market position; Leerink Partners cut its price target to $89 and now projects essentially flat U.S. EP growth in FY2027, a scenario not yet embedded in consensus

- WATCHMAN’s CHAMPION label expansion timeline is measured in years, not quarters: FDA review, guideline updates, and a CMS NCD revision each represent independent bottlenecks; the 20-million-patient TAM is a 2030 story, not a 2026 revenue event

- The securities class action with a May 4 lead plaintiff deadline creates ongoing headline risk and could delay institutional re-entry into BSX stock even as fundamentals stabilize

- FY2026 FCF consensus of around $3.64 billion is essentially flat year-over-year, a pause in cash generation that limits near-term buyback capacity just as the stock trades at its widest discount to intrinsic value in years

- The pacemaker battery issue under investigation by Australian regulators and referenced in the NYT report, combined with the AXIOS stent removal and ACURATE discontinuation, signals that product quality management remains a risk the new CFO team will need to address visibly

Should You Invest in Boston Scientific Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up BSX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Boston Scientific Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze BSX stock on TIKR for Free →