Key Stats: Fiserv Stock (FISV)

- Current Price: ~$64

- Full-Year 2025 Adjusted Revenue: $19.8B (+4% YoY)

- Full-Year 2025 Adjusted EPS: $8.64 (above guidance of $8.50–$8.60)

- Q4 2025 Adjusted Revenue: $4.9B (flat YoY)

- Q4 2025 Adjusted EPS: $1.99

- Full-Year 2026 Organic Revenue Guidance: +1% to +3%

- Full-Year 2026 Adjusted EPS Guidance: $8.00–$8.30

- TIKR Model Price Target: ~$99

- Implied Upside: ~55%

Q4 2025 Earnings Breakdown: What Fiserv Reported

Fiserv stock (FISV) closed out 2025 with Q4 adjusted revenue of $4.9 billion, flat year-over-year, and full-year adjusted revenue of $19.8 billion, up 4%.

Full-year adjusted EPS came in at $8.64, above management’s guidance range of $8.50 to $8.60.

Organic revenue grew 3.8% for the full year, finishing in the upper half of the 3.5% to 4% guidance range management had provided on the Q3 call.

Clover was the standout growth driver, finishing the year at $3.3 billion in revenue, up 23%, with Q4 Clover revenue growing 12%, two percentage points above management’s guidance for the quarter, according to Chief Financial Officer Paul Todd on the Q4 earnings call.

A 6-point fee elimination headwind suppressed Q4 Clover revenue growth, meaning underlying volume trends were stronger than the reported figure.

Clover volume growth softened in November due to weakness in the restaurant and retail sectors, but volumes reaccelerated on a combined December-January basis to approximately 11%, excluding the gateway conversion.

Clover Capital grew 30% in North America in 2025, according to CEO Mike Lyons on the Q4 earnings call.

Commerce Hub processed over $200 billion in 2025, a greater than 200% year-over-year increase, according to CEO Mike Lyons on the Q4 earnings call.

Financial Solutions was the primary drag: Q4 organic and adjusted revenue both declined 2%, and banking revenue fell 4% organically, continuing to absorb headwinds from client attrition in the core banking segment.

Full-year free cash flow reached $4.44 billion, above the guided $4.25 billion, representing approximately 93% conversion.

For 2026, management guided to organic revenue growth of 1% to 3% and adjusted EPS of $8.00 to $8.30, with H1 revenue expected to decline in the low single digits as the company laps a higher prior-year mix of nonrecurring revenue.

Fiserv Stock: What the Financials Show

The Q4 income statement reflects a margin compression story: gross margin and operating margin both declined sharply year-over-year despite roughly flat revenue, pointing to cost investment rather than volume weakness as the driver.

Q4 2025 revenue was $5.3B, up 0.6% from $5.3B in Q4 2024.

Q4 2025 gross margin came in at 57%, down from 62% in Q4 2024.

Q4 2025 operating income was $1.3 billion, with an operating margin of 24.4%, compared to 31.8% in Q4 2024.

The compression intensified through the back half of 2025: Q1 operating margin was 26.8%, Q2 was 30.8%, Q3 was 25.4%, and Q4 came in at 24.4%.

Management guided Q1 2026 operating margin to come in just below 30%, before a recovery to 35% to 36% in the second half, blending to approximately 34% for the full year.

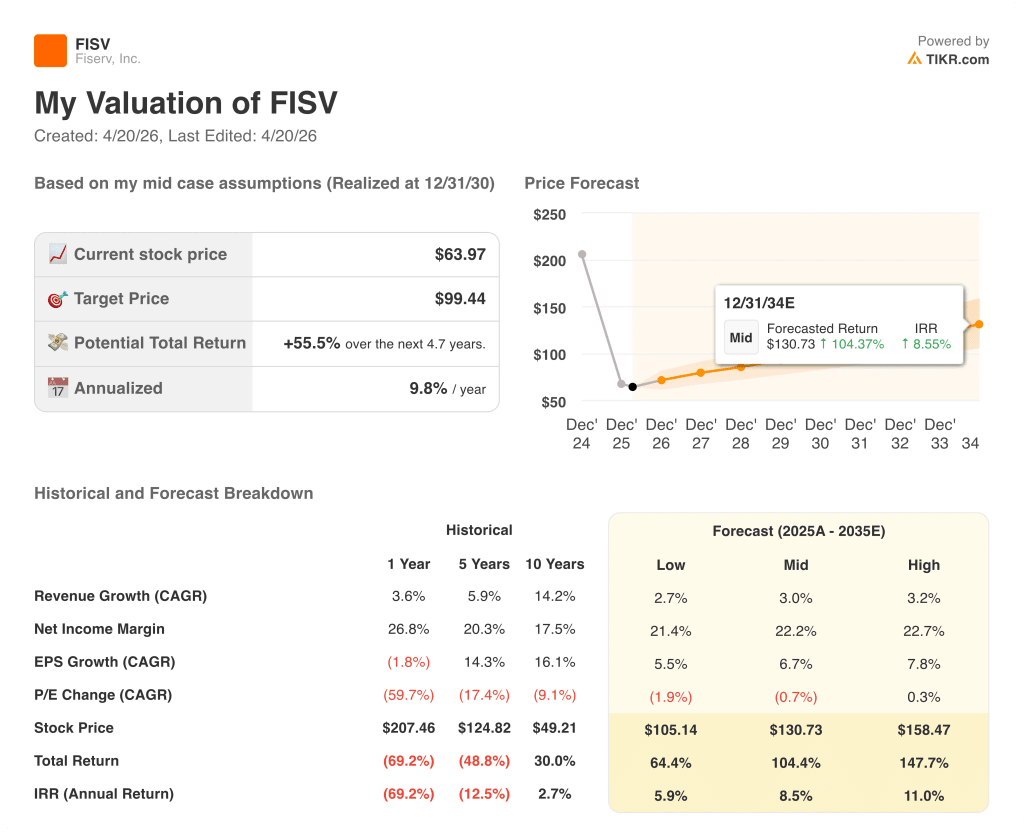

Valuation Model Take and Scenario Breakdown

TIKR’s model prices Fiserv stock at ~$99, implying roughly 55% upside from the current price of ~$64.

The mid-case assumptions are a revenue CAGR of 3% and a net income margin of 22.2%, both consistent with management’s own guidance framework if the second-half 2026 margin recovery materializes as projected.

The Q4 results did not break the long-term thesis for Fiserv stock, but they confirmed that the next two quarters will be noisy: EPS guidance of $8 to $8.30 in 2026 sits below the $8.64 delivered in 2025, meaning near-term earnings contraction is already baked into management’s base case.

At ~$64, Fiserv stock is pricing in a scenario where the turnaround stalls. The 55% upside in the TIKR model reflects the gap between that skepticism and a base case where 3% revenue growth and recovered margins compound over the next several years.

The central tension: Fiserv’s underlying volume drivers remain intact, but investors must decide whether the first-half 2026 margin trough is a temporary reset or the start of a more persistent profitability drag.

What Has to Go Right

- Clover must sustain low double-digit revenue growth in 2026, building on 23% full-year 2025 performance, with Clover Capital’s 30% North America expansion and the ADP and Homebase partnerships adding durable yield

- Operating margin must recover to 35% to 36% in H2 2026 from a Q1 floor just below 30%, a roughly 500 to 600 basis point sequential improvement

- Financial Solutions banking must return to low-single-digit positive organic growth in H2 2026, as guided, after four consecutive quarters of negative organic revenue

- Commerce Hub, having exceeded $200 billion in processing volume in 2025, must convert its pipeline into recurring enterprise revenue that contributes meaningfully to the 1% to 3% organic growth target

What Could Still Go Wrong

- Financial Solutions Q4 adjusted operating margin collapsed to 42.2% from 51.7% a year earlier; if incremental investment persists beyond H1, the company-level H2 margin target of 35% to 36% becomes difficult to hit

- Clover volume growth showed macro sensitivity in November 2025 in restaurant and retail, and a weaker 2026 consumer could push Clover GPV growth toward the low end of the guided 10% to 15% range

- Core banking client attrition remained above management’s desired levels through all of 2025, and the banking segment is still expected to weigh on Financial Solutions through at least the first half of 2026

- 2026 adjusted EPS guidance of $8.00 to $8.30 implies year-over-year earnings contraction from the $8.64 delivered in 2025, even before accounting for execution risk on the margin recovery

Should You Invest in Fiserv, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FISV stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Fiserv, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FISV stock on TIKR for Free →