Key Stats

- Current price: ~$40

- Q2 FY2026 core revenue: $375M, +17% YoY

- Q2 FY2026 non-GAAP operating margin: 18%

- Spend & Expense revenue (Q2): $166M, +24% YoY

- FY2026 core revenue guidance: $1.490B–$1.510B (+16% YoY)

- FY2026 non-GAAP EPS guidance: $2.33–$2.41

- TIKR model price target: ~$73

- Implied upside: ~85% over ~4 years

Earnings Breakdown: BILL Holdings Accelerates Revenue Growth in Q2

BILL Holdings stock (BILL) posted Q2 FY2026 core revenue of $375 million, up 17% year-over-year, beating the top end of guidance and marking a 370-basis-point sequential acceleration.

Non-GAAP operating margin came in at 18%, expanding both sequentially and year-over-year, as cost discipline compounded alongside volume growth.

Spend & Expense was the strongest segment, generating $166 million in revenue, up 24% year-over-year, driven by accelerating card payment volume of 25% year-over-year and favorable mix toward higher-interchange verticals including advertising and health care services.

AP/AR core revenue grew 11% year-over-year, with transaction revenue of $128 million, up 14% year-over-year, and same-store sales TPV growth of 4%, an acceleration from the prior quarter.

According to CFO Rohini Jain on the Q2 FY2026 earnings call, “These results mark another step forward in growing BILL into a larger, more profitable enterprise.”

BILL Holdings stock saw notable multiproduct momentum: the number of businesses using both AP/AR and Spend & Expense grew 28% year-over-year, a cohort that carries meaningfully higher revenue per customer.

The company repurchased $133 million of stock during the quarter as part of its ongoing capital return program.

For Q3 FY2026, management guided core revenue of $364.5 million to $374.5 million, representing 14% to 17% year-over-year growth, with non-GAAP EPS of $0.53 to $0.57.

Full-year FY2026 core revenue guidance was raised to $1.490 billion to $1.510 billion, approximately 170 basis points above the prior guide, reflecting sustained confidence in second-half execution.

Full-year non-GAAP EPS guidance was set at $2.33 to $2.41, with operating margin expected at approximately 17%, representing more than 320 basis points of year-over-year margin expansion excluding the benefit of float.

BILL Holdings Stock: What the Financials Show

The income statement reflects a business still operating at a GAAP loss but compressing that loss meaningfully as revenue scale has grown, with gross margin holding broadly stable through the expansion.

Total revenues reached $1.46 billion for the fiscal year ended June 30, 2025, up ~13% year-over-year, providing the revenue base from which Q2’s acceleration is launching.

Gross margin was 84.3% for FY2025, modestly below 85.3% in FY2024 and 85.7% in FY2023, reflecting a slight compression as the payment mix has shifted.

GAAP operating loss was $(0.08) billion for FY2025, representing an operating margin of (5.5%), a significant improvement from (11.4%) in FY2024 and (23.0%) in FY2023, pointing to a sustained multi-year operating leverage trajectory.

Valuation Model Take and Scenario Breakdown

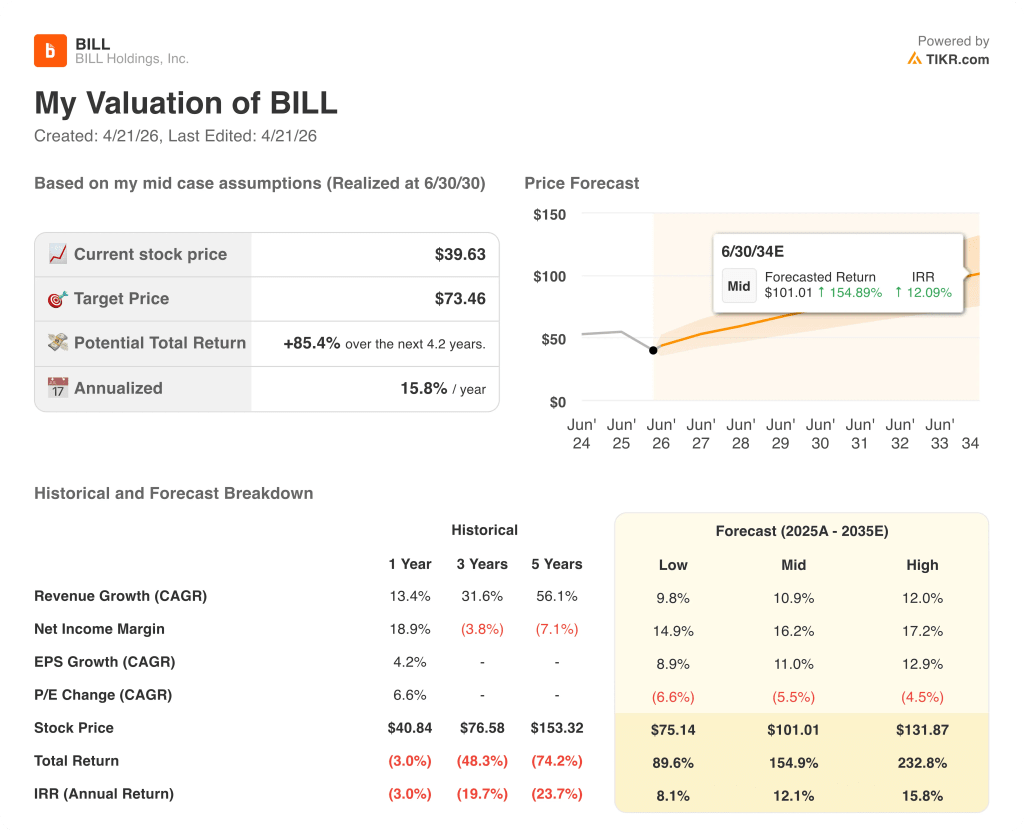

The TIKR model prices BILL Holdings stock at ~$73, implying roughly 85% upside from the current price of ~$40, over a 4.2-year horizon at an annualized rate of about 16%.

The mid-case model assumes revenue CAGR of 10.9% and a net income margin expanding to 16.2% from a currently negative GAAP baseline, which requires the non-GAAP margin momentum visible in Q2 to translate into sustained GAAP profitability.

The Q2 report strengthens the investment case modestly: the 370-basis-point revenue acceleration, the 290-basis-point non-GAAP operating margin expansion year-over-year, and the full-year guidance raise all point in the direction the model requires.

BILL Holdings stock is not cheap on near-term GAAP metrics, but the margin trajectory and raised guidance tighten the gap between current performance and the assumptions embedded in the TIKR target.

The central tension: BILL stock’s bull case requires sustained double-digit revenue growth and a clean path to GAAP profitability, neither of which is fully proven at this scale.

What Has to Go Right

- Core revenue growth sustains at 15%+ through FY2026, supported by the raised guidance range of $1.490B–$1.510B and early Q3 volume trends management cited as encouraging.

- Non-GAAP operating margin expansion continues past 17%, with the GAAP operating loss compressing from (5.5%) in FY2025 toward breakeven as BILL continues adding leverage on its $1.46B+ revenue base.

- Spend & Expense maintains its 24% growth trajectory, led by card payment volume of 25% and take rate above 250 basis points, a combination management guided for the full year.

- Embed 2.0 partnerships with NetSuite, Acumatica, and Paychex begin contributing meaningful TPV and revenue in FY2027, with management explicitly citing FY27 as the expected inflection year.

What Could Still Go Wrong

- AP/AR customer net adds are guided to trend slightly lower near-term as BILL shifts focus to larger businesses, creating a period where ARPU growth must offset volume to maintain the revenue trajectory.

- Spend & Expense revenue was partially driven by vertical mix favorability in advertising and retail, categories management acknowledged had been muted in prior quarters, raising questions about how durable Q2’s volume lift is.

- GAAP profitability remains negative despite significant improvement, with TIKR’s mid-case requiring a net income margin of 16.2% by the end of the forecast horizon, a level that requires years of continued execution without macro or competitive disruption.

- Rewards rate on card spend was 133 basis points in Q2, up 9 basis points year-over-year, and while management noted the rate of increase is moderating, rewards costs remain a drag that limits how fast net margin can expand.

Should You Invest in BILL Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up BILL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track BILL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze BILL Holdings, Inc. stock on TIKR for Free →